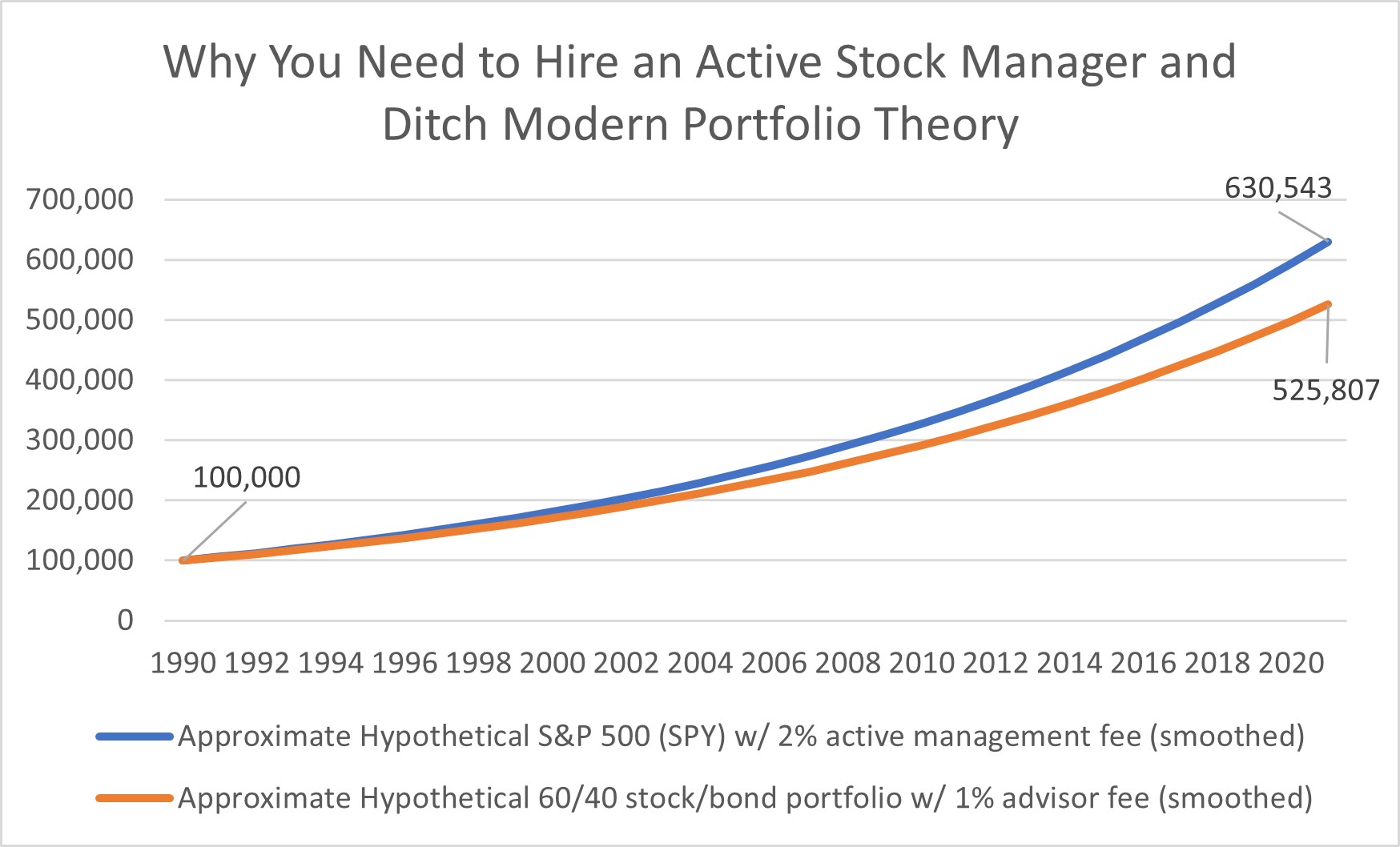

Image: Why You Need to Hire an Active Stock Manager and Ditch Modern Portfolio Theory. An Approximate Hypothetical representation of an active manager that charges a 2% active management fee that mirrors the S&P 500 benchmark versus an advisor that charges a 1% advisor fee that applies a 60/40 stock/bond rebalancing from 1990-2021. Approximate Hypothetical returns are based on the following extrapolation: “Since inception in November 9, 1992, returns after taxes on distributions and sales of fund shares for the [Vanguard Balanced Index Fund Investor Shares] VBINX came in at 6.5% through June 30, 2020, while the same measure since inception in January 22, 1993, for the S&P 500, as measured by the S&P 500 ETF Trust (SPY), came in at 8.12% through June 30, 2020.” The ‘Approximate Hypothetical 60/40 stock/bond portfolio w/ 1% advisor fee (smoothed)’ represents a hypothetical 100,000 compounded at an annual rate of 5.5% [6.5 less 1] over the period 1990-2021. The ‘Approximate Hypothetical S&P 500 (SPY) w/ 2% active management fee (smoothed)’ represents a hypothetical 100,000 compounded at an annual rate of 6.12% [8.12 less 2] over the period 1990-2021. Approximate Hypothetical results are for illustrative purposes only and are based on the data available.

By Brian Nelson, CFA

We’ve been witnessing relative strength in Korn Ferry (KFY) and Dick’s Sporting Goods (DKS), which advanced 1.7% and 2.9%, respectively, during the trading session March 30.

We continue to like these two ideas in the Best Ideas Newsletter portfolio and Dividend Growth Newsletter portfolio, though we note that Korn Ferry has advanced significantly since it registered a 9 on the Valuentum Buying Index.

Please read more about our call on Korn Ferry here >>. Dick’s Sporting Goods raised its payout in a big way as we noted in this article here >>. The sporting goods retailer boasts an amazing Dividend Cushion ratio of 3.2.

We continue to like the areas of large cap growth and big cap tech as we emphasize that “Nothing May Derail the U.S. Economy In the Long Run.” Facebook (FB) is by far our favorite idea as shares remain severely underpriced.

In other news, we highlighted Chewy (CHWY) in the Exclusive publication January 2020, and since then, shares have rocketed to as high as $120 per share, now trading at ~$80. The Exclusive publication can be an add-on to your regular membership.

We talked about the secular trend in the humanization of pets in the recent article about General Mills (GIS) that goes into super-premium pet food maker Blue Buffalo here, and we expect peer Chewy to continue to prosper. During fiscal 2020, Chewy’s net sales advanced 47%, while adjusted EBITDA swung into positive territory, to $85.2 million.

But strong results may not be the biggest reason why Chewy has been in the headlines of late.

On March 8, meme-stock favorite GameStop (GME) noted that it had hired Chewy’s co-founder Ryan Cohen to lead the troubled used-game retailer into e-commerce. Since Cohen’s hire, GameStop has brought on board a number of executives with varied previous experience at Amazon, Chewy and Walmart.

Though we like the personnel changes, we can’t forget Warren Buffett’s famous quote: “When a management with a reputation for brilliance tackles a business with a reputation for poor fundamental economics, it is the reputation of the business that remains intact.” We saw a similar type of excitement and hype play out at J.C. Penney in 2012 when they hired Apple veteran Ron Johnson to transform the business model. The department store filed for bankruptcy May 2020.

Of course, management is always an important investment consideration (especially when it comes to negative corporate governance considerations), but it generally is not as important as understanding a company’s industry structure via Porter’s 5 forces and competitive advantage analysis. We’ll cite Buffett again on this: “Go for a business that any idiot can run – because sooner or later, any idiot probably is going to run it.”

In short, we think GameStop should be in your too-hard bucket >>. The company will be issuing equity, which will result in a fair value estimate increase (any equity raised at a price above our fair value estimate will increase the fair value estimate), but we expect the company’s stock to be trading in the double digits soon enough. Shares are trading hands at ~$194 at the moment.

In many ways, “GameStop” has been an unfortunate side-show, but one that reveals the hazards of price-agnostic trading, backward-looking factor investing and the silliness of the efficient markets hypothesis. Investors in the Reddit community were trading on the quant factor “short interest as a percentage of float,” driving prices of troubled companies to nonsensical levels, almost blowing up hedge fund Melvin Capital.

But meme-stocks and their Reddit/Robinhood backers aren’t the only ones that have been infected with the price-agnostic trading bug. Archegos Capital reportedly levered up many times to become overexposed to holdings such as Viacom (VIAC), which shot up to an irrational $100 per share before falling back toward our fair value estimate. Leverage and price-agnostic trading have always been a recipe for disaster. Didn’t we already learn this from LTCM?

As with GameStop that traded in the range of $180 and $350 per share during the same trading day on no news on March 10, many may just be lying to themselves when they take any form of the efficient markets hypothesis seriously. What’s wrong is wrong. Today’s traders in meme stocks such as GameStop and AMC Entertainment (AMC)–and separately with the episode in Viacom– know there’s not much backing the view that stocks are priced “correctly.” It’s a terrible lens by which to view the markets.

You check the receipt for what you pay for groceries at the store, right? Why wouldn’t you pay attention to what you’re paying for businesses (stocks), too?

Unfortunately, the efficient markets hypothesis has been a big reason why index funds have found support within the academic community (and with professionals alike). However, considering the lack of analytical substance within most of quant finance (read Value Trap), it’s hard for me to sleep well at night relying on any quant reasoning given the failures of the CAPM, the quant “value” premium, EMH and beyond. I recently wrote a note on the pitfalls of chasing standard deviation as a measure of risk and “Why You Must Stay Active in Investing.” Evaluate alternate histories (“scenario analysis”) as a way to gauge risk.

To a large extent, even modern portfolio theory has broken down. Here’s what I wrote in the book Value Trap:

A 60%/40% stock/bond portfolio, as measured by the Vanguard Balanced Index Fund Investor Shares (VBINX), for example, fell 17.6% year-to-date through March 18, 2020, and it only “saved” investors from a mere 8 percentage points of underperformance during the worst of the COVID-19 swoon relative to the S&P 500 during that time. However, according to Vanguard’s website, the relative cost to an investor that held the VBINX for its diversification benefits during the 10-year period ending July 30, 2020–arguably to protect against the volatility of the exact adverse market outcome as that driven by the COVID-19 crisis–was over 110 percentage points of cumulative total return underperformance compared to the S&P 500, or roughly $11,324 on an initial $10,000 investment. That was a huge price to pay during the past 10 years through the time of this writing.

Over a longer-run measurement period, the comparison does not get much better. Since inception in November 9, 1992, returns after taxes on distributions and sales of fund shares for the VBINX came in at 6.5% through June 30, 2020, while the same measure since inception in January 22, 1993, for the S&P 500, as measured by the S&P 500 ETF Trust (SPY), came in at 8.12% through June 30, 2020. Though more than 1.5 percentage points of underperformance per year does not sound like much, it compounds quite a bit over a near 30-year period. When it comes to retirement, are investors going to care more about their risk-adjusted returns or more about how big their nest eggs grew after saving for 30 years? I think the latter. For long-term investors and entities with indefinite lives, perhaps they should be concerned that MPT does, in fact, sound a lot like “empty.”

With that humbly said, there was some good news across our coverage this week. Williams Sonoma (WSM) put up a monster fourth quarter, released March 17, and we have raised our fair value estimate as a result (we expect a further fine-tuning of our valuation model in the coming weeks). The company’s fourth-quarter same-store sales advanced 25.7% beating consensus estimates by more than 5 percentage points. We loved its free cash flow generation during fiscal 2020 thanks to a more-than-doubling of operating cash flow and lower capex.

Here’s what WSM’s management had to say in its fourth-quarter earnings press release:

Looking ahead, we are very optimistic about our runway for growth and profitability. All of our brands are starting the year strong, and we expect this strength to continue through 2021 and beyond based on a number of factors. First, it is the ongoing momentum of our growth initiatives and the increasing relevance of our three key differentiators. Second, it is the recovery in our retail traffic and our inventory levels as we move throughout the year. And third, it is the favorable macro trends that are expected to continue to benefit our business for the long-term, including high consumer confidence, a strong housing market, an accelerating shift to e-commerce, the expected continuation of working from home in some capacity post pandemic, and the importance of sustainability and values to the consumer. Against this backdrop, we are confident that we will deliver mid-to-high single digit revenue growth and operating margin expansion in 2021. Longer-term, we have accelerated our path to $10 billion in net revenues and see us hitting this milestone in the next five years, with operating margins at 15%.

Flavor and spice giant McCormick & Company (MKC) also put up very nice fiscal first quarter performance for the period ending February 28, 2021, results released March 30. Sales leapt an impressive 22% driving adjusted operating income 35% higher in its fiscal first quarter from the year-ago period. The company has been benefiting from a “sustained shift to cooking more at home, increased digital engagement, clean and flavorful eating, and trusted brands.” McCormick’s management was confident enough to raise its outlook for fiscal 2021, too, suggesting the accelerated shift to eating more at home has legs:

In 2021, the Company expects to grow sales by 8% to 10% compared to 2020, which in constant currency is 6% to 8%…This is an increase from the Company’s previous projection of 7% to 9%, or 5% to 7% in constant currency. Operating income in 2021 is expected to grow by 5% to 7% from $1.00 billion in 2020…adjusted operating income is expected to grow by 9% to 11%, which in constant currency is 7% to 9%. This is an increase from the Company’s previous projection of 8% to 10%, or 6% to 8% in constant currency…McCormick increased its projected 2021 earnings per share to be in the range of $2.77 to $2.82, compared to $2.78 of earnings per share in 2020… the Company projects 2021 adjusted earnings per share to be in the range of $2.97 to $3.02. This is an increase from previously reported guidance of $2.91 to $2.96 and, as compared to $2.83 of adjusted earnings per share in 2020, represents an expected increase of 5% to 7%, which includes a favorable impact from currency.

We’re monitoring the trading activity of CRISPR Therapeutics (CRSP) closely, and while shares of the company have faced pressure during the past few months, we’re going to maintain our $200 per share fair value estimate for now, with the emphasis on our last bullet point in its 16-page report: “Shares of CRISPR Therapeutics are nearly impossible to value with any sort of precision, and our valuation assumptions are highly subjective and certain to change in coming updates. Though its technology is revolutionary, CRSP’s shares are ultra-speculative.” CRISPR Therapeutics gene-editing breakthroughs are exciting nonetheless, and while we like the prospects, we prefer Vertex (VRTX) as our biotech play in the Best Ideas Newsletter portfolio.

Read more about our thesis on Vertex here >>

As I wrap up, I wanted to address member questions about the hypothetical performance of Valuentum’s simulated newsletter portfolios. Valuentum hasn’t emphasized this area in part because Valuentum is not a money manager or financial advisor. However, the latest update showed that our process can handle major market disruptions. For example: “From February 15 through June 11, or through the course of the worst of the COVID-19 meltdown and its abrupt recovery, we estimate that the Best Ideas Newsletter portfolio exceeded the market return by about 7.8 percentage points.”

Please be sure to read, “Outperformance of Valuentum’s COVID-19 Ideas.” We expect to do more extensive studies on our hypothetical simulated newsletter performance in the coming months. But that’s it for now. The April edition of the High Yield Dividend Newsletter and the April edition of the Dividend Growth Newsletter will be released April 1. The April edition of the Exclusive publication will be released Saturday, April 10. Note that this is the second Saturday of April due to the upcoming holiday weekend. More to come. Stay tuned.

Related: The Skill Paradox Is a Myth in Investing

Stock Pages

—–

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Brian Nelson owns shares in SPY, SCHG, QQQ, DIA, and IWM. Brian Nelson’s household owns shares in HON. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.