|

|

Recent Articles

-

Ferrari's Results Speak to Resilience in Ultra-Luxury Markets

Ferrari's Results Speak to Resilience in Ultra-Luxury Markets

Nov 2, 2023

-

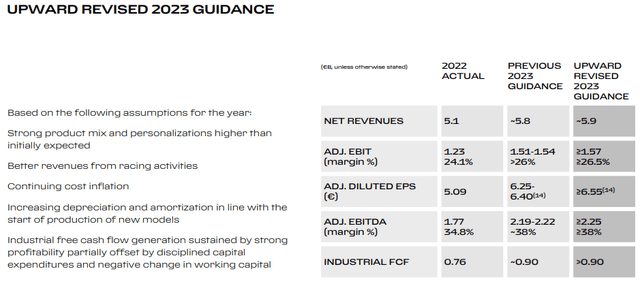

Image: Ferrari raised its guidance for 2023.

Ferrari raised its year-end guidance thanks in part to a strong product mix and improved revenue from racing activities, and the firm noted that its “order book remains at highest levels reflecting strong demand across all geographies, covering the entire 2025.” We couldn’t be happier with the performance at Ferrari, and the momentum speaks to continued strength across the ultra-luxury landscape. We like Ferrari as one of our favorite automakers, a name that we prefer much more than any of the Big 3 in Detroit.

-

AMD Continues to Enhance Artificial Intelligence Capabilities

Nov 2, 2023

-

On October 31, Advanced Micro Devices reported solid third-quarter results with revenue advancing 4% on a year-over-year basis and non-GAAP earnings per share coming in slightly better than expectations, with net income up more than four-fold, to $299 million. Management expressed excitement about demand for its Ryzen 7000 series PC processors and noted that its data center business is progressing well thanks to its 4th Gen EPYC CPU portfolio and Instinct MI300 accelerator shipments across various markets, including artificial intelligence [AI].

-

Caterpillar's Pricing Power Remains Phenomenal

Nov 1, 2023

-

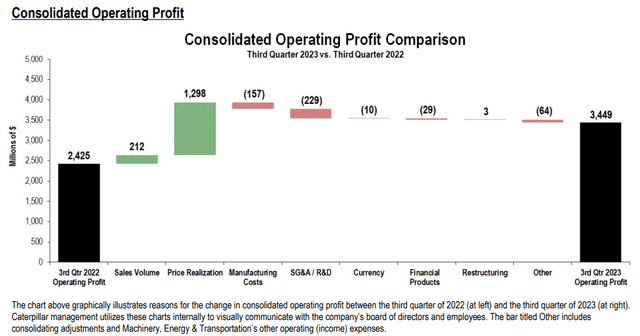

Image: Price realization remains a key driver behind Caterpillar’s strong performance.

On October 31, Caterpillar reported better-than-expected third-quarter results, with revenue advancing 12% and non-GAAP diluted earnings per share handily beating the consensus forecast. Caterpillar continues to benefit from significant pricing power, but the firm is also experiencing volume increases. The firm's adjusted operating profit margin expanded to 20.8% in the third quarter compared to 16.5% for the third quarter of 2022. Caterpillar ended the third quarter with $6.5 billion in cash and cash equivalents, short-term borrowings of ~$4.2 billion, and long-term debt of ~$1 billion and ~$7.6 billion in its ‘Machinery, Energy & Transportation’ and ‘Financial Products’ divisions, respectively. Its balance sheet, while not showcasing a net cash position, remains very healthy, in our view, especially in the context of its free cash flow generation. Through the first nine months of 2023, the maker of mining and construction equipment’s cash flow from operations soared to ~$8.9 billion, as it shelled out just ~$1.06 billion in capital expenditures, a number that excludes equipment leased to others (~$1.2 billion). Free cash flow generation at the firm remains excellent, and we like that it continues to focus on dividend growth. We continue to like the pricing power witnessed within Caterpillar’s operations of late, and we’re sticking with our above-market $262 fair value estimate for now.

-

Public Storage Raises Core FFO Guidance for 2023

Oct 31, 2023

-

Image Source: Public Storage.

Among the REIT sub-sectors, we continue to favor the self-storage space mostly because its traditional free cash flow dynamics are much more attractive. Self-storage REITs are generally recession-resistant, too, offer high operating margins, and generally lower maintenance capital requirements. Public Storage is our favorite self-storage REIT and yields ~5% at the time of this writing. Shares of PSA have soured with the broader equity REIT sell-off this year and have declined nearly 13% year-to-date in 2023. Though we expect a challenging market environment for equity REITs, we view Public Storage as the best long-term play in self-storage.

|