|

|

Recent Articles

-

3 Mid Caps With Net Cash And Strong Free Cash Flow

3 Mid Caps With Net Cash And Strong Free Cash Flow

Oct 31, 2023

-

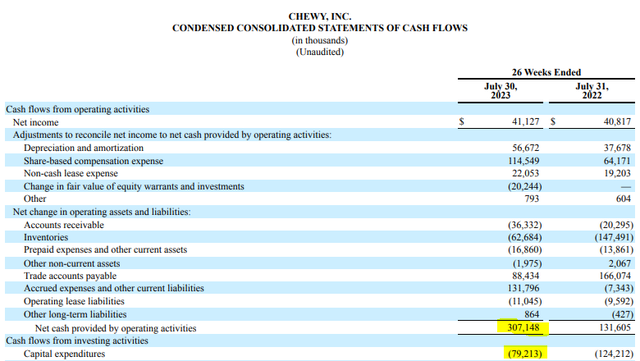

Image: Chewy's best-in-class customer service is paying off in strong free cash flow generation.

We're huge fans of companies with net cash on their balance sheet and strong free cash flow generating potential. This view has led us to favor the areas of big cap tech and the stylistic area of large cap growth in the newsletter portfolios, but there are other companies emerging with similar economics on a smaller scale. Chewy, Inc. E.L.F Beauty and DocuSign are three that come to mind, and all three of these names boast a strong balance sheet and favorable free cash flow dynamics. Each of these companies is also benefiting from secular growth trends as they seek to gain market share against rivals. Though certainly not without valuation risk as the trajectory of free cash flow expectations will certainly cause volatility in their respective stocks, we think all three may be worthy of consideration for the aggressive, risk-seeking investor targeting long-term capital appreciation.

-

The Dividend Growth Newsletter Portfolio’s Outperformance

Oct 30, 2023

-

Image: The Dividend Cushion ratio is one of the most powerful financial tools an income or dividend growth investor can use in conjunction with qualitative dividend analysis. The ratio is one-of-a-kind in that it is both free-cash-flow based and forward looking. Since its creation in 2012, the Dividend Cushion ratio has forewarned readers of approximately 50 dividend cuts. We estimate its efficacy at ~90%.

Large cap growth names in the likes of Apple, Microsoft, Oracle, and Cisco form a solid foundation for continued dividend growth across the portfolio thanks in part to their fantastic Dividend Cushion ratios. Not only this, but we like the defensive characteristics of garbage hauler Republic Services and McDonald’s, and the tried-and-true dynamics of Home Depot, Honeywell and UnitedHealth, which can handle just about any economic environment that is thrown at them. Today, the 10-year Treasury rate stands at close to 5%, so while many dividend growth stocks don’t yield as much, we still like their cash-based sources of intrinsic value, as such dynamics offer substantial support to their equity prices, despite competing sources of income.

-

Staying Far Away from Intel; McDonald’s a Better Play

Oct 30, 2023

-

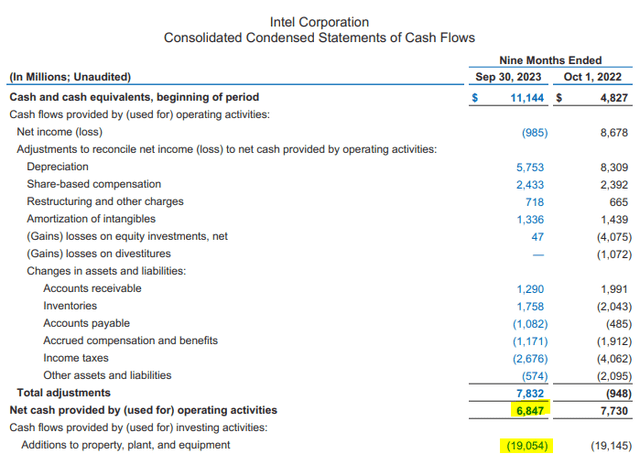

Image: Intel’s cash flow from operations is under pressure, as it continues to shell out capital expenditures, resulting in materially negative free cash flow generation.

Intel's cash-based sources of intrinsic value are in a world of hurt, meaning that we won't be adding the company to any newsletter portfolio anytime soon. Instead, we prefer McDonald's, which is well-positioned for inflationary pressures as it continues to raise its payout.

-

3 Net-Cash-Rich, Free-Cash-Flow Generating, Secular Growth Powerhouses

Oct 30, 2023

-

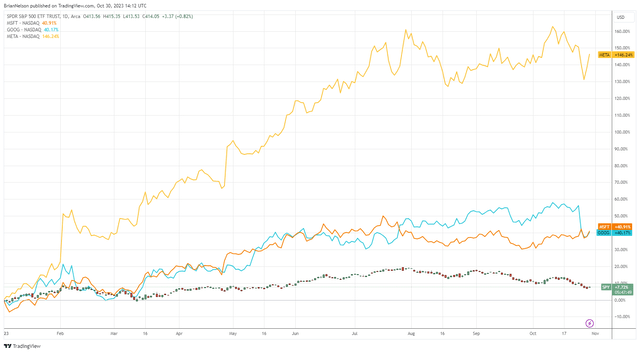

Image: Shares of Microsoft, Alphabet, and Meta Platforms have trounced the market return so far in 2023.

We think a holistic view to a company's fundamentals provides an upper hand when it comes to outperforming the market, but we also feel that the discounted cash-flow model is an indispensable tool to help investors collect all of their thoughts and quantitatively put them together within valuation to arrive at what a company is worth. After all, the stock market is an expectations game, where expectations of free cash flow form the baseline for value, and changes in them heavily influence the direction of share prices. We like stocks that have strong net cash positions on the books and have a high probability of achieving better-than-expected free-cash-flow generation in coming years. In this article, we'll talk about the cash-based sources of intrinsic value at three large cap growth names.

|