Morgan Stanley truly shined during this quarter of extreme volatility. While credit provisioning was higher year over year, Morgan Stanley simply does not have many of the credit exposures that are leading to huge multi-billion-dollar credit provisions at some of its money-center banking peers. Though its wealth management business’ net income (applicable to Morgan Stanley) was down 10% year over year, and Investment Management was up only 20%, it was the Institutional Securities stunning 95% advance in net income that made this quarter a (temporary) gem of notable brilliance.

By Matthew Warren

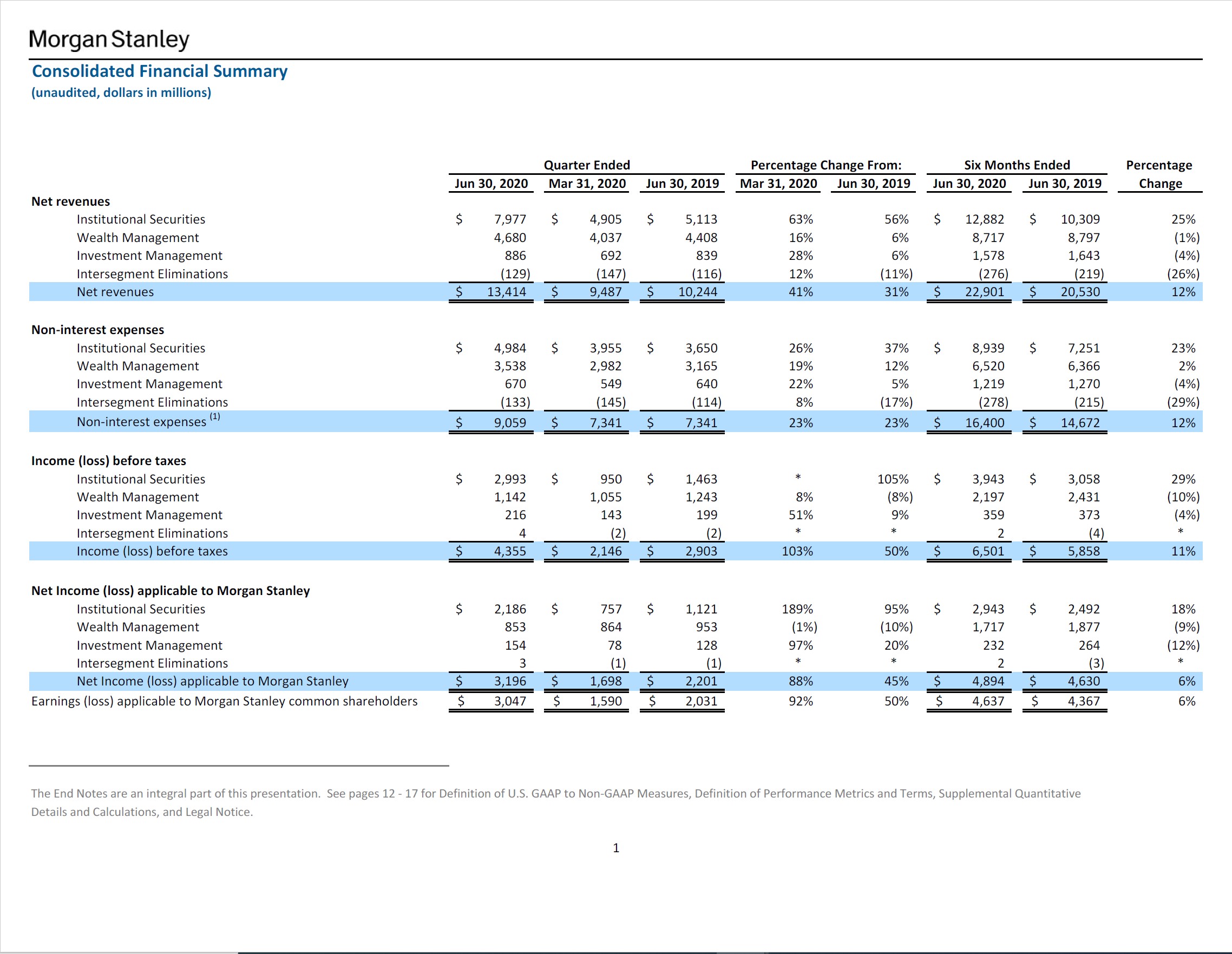

Morgan Stanley (MS) put up a tremendous quarter July 16, blowing away analyst consensus estimates on both the top and bottom lines. As you can see in the upcoming graphic down below, the notoriously volatile Institutional Securities segment had a blowout quarter, driving the income growth as compared to the same quarter last year.

Image Shown: Morgan Stanley’s 2Q2020 Results Broken Down by Segment. Image Source: Morgan Stanley’s 2Q2020 Earnings Supplement.

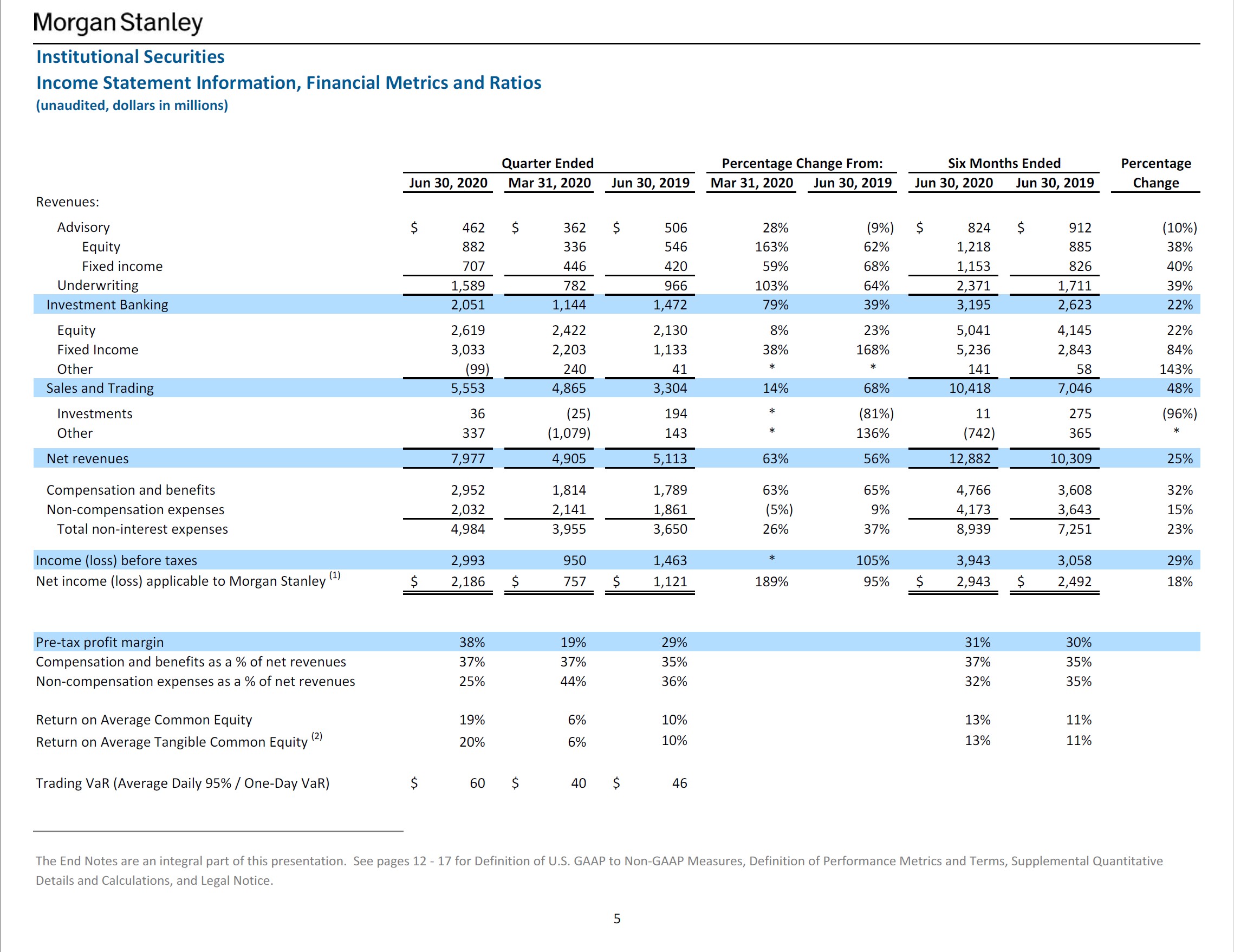

So, let us take a closer look at the subsegments within the Institutional Securities segment. As you can see in the upcoming graphic down below, equity and fixed income underwriting and especially Fixed Income Sales and Trading were outrageously strong in the quarter.

Image Shown: A Closer Look at Morgan Stanley’s Institutional Securities Sub Segments. Image Source: Morgan Stanley 2Q2020 Earnings Supplement

Underwriting was strong across the industry as clients raised massive amounts of liquidity to shore up their balance sheets to withstand potential downside scenarios associated with the COVID-19 induced economic downturn. While many firms initially pulled down their revolving credit lines, much of that liquidity was actually paid back by quarter end as equity, converts, and new debt offerings put in place longer dated and more stable capital.

As to the 168% year over year gain in fixed income sales and trading, this is what happens when investor clients seek out a strong counter party to navigate incredibly volatile markets. Based on industry revenue figures, it’s clear that there was massive turnover of client portfolios as asset prices tanked starting back in March and then recovered so rapidly thereafter. The investment banking industry should send the Treasury and Federal Reserve a huge thank you letter for putting a bottom into these volatile markets and creating such a flurry of trading as asset markets recovered in such rapid fashion. As to whether this activity can continue apace, Morgan Stanley CEO tamped down expectations as did several other industry executives on this round of earnings calls:

So what does the future hold? Clearly, it will be challenging for the back half of 2020 to meet the record first half results and we expect advisory and macro trading to be significantly lower. That said, many parts of our business should continue to perform well.

Morgan Stanley truly shined during this quarter of extreme volatility. While credit provisioning was higher year over year, Morgan Stanley simply does not have many of the credit exposures that are leading to huge multi-billion-dollar credit provisions at some of its money-center banking peers. Though its wealth management business’ net income (applicable to Morgan Stanley) was down 10% year over year, and Investment Management was up only 20%, it was the Institutional Securities stunning 95% advance in net income that made this quarter a (temporary) gem of notable brilliance.

—

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Matthew Warren does not own any of the securities mentioned. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.