Morgan Stanley posted difficult first-quarter 2020 results, released April 16, missing consensus estimates on both the top line and the bottom line. Return on average tangible common equity was 9.7% in the quarter, well above levels of just a few years back (and again better than large bank peers in the quarter), showing the progress that Morgan Stanley has made in improving its return profile.

By Matthew Warren

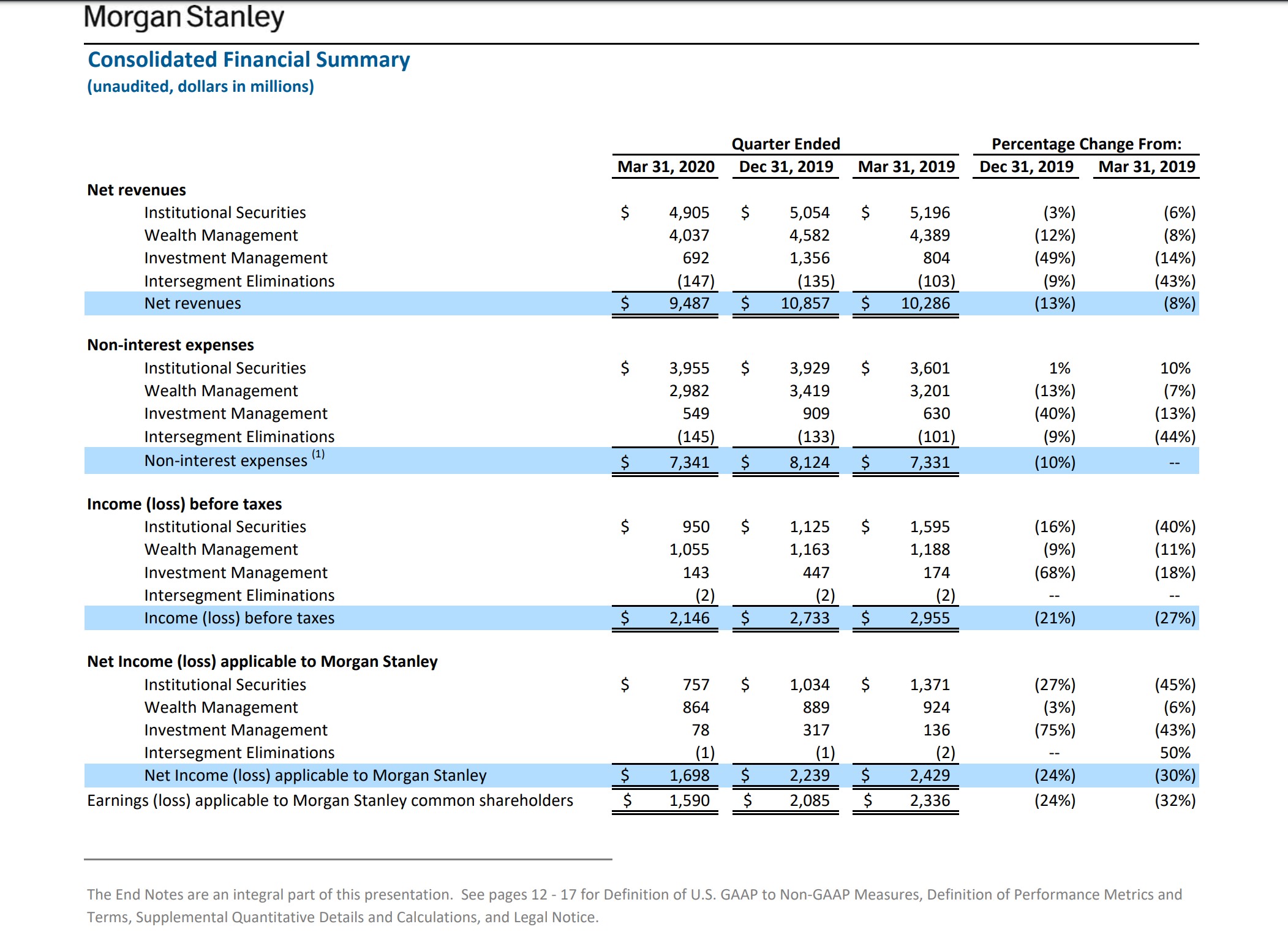

Morgan Stanley (MS) posted difficult first-quarter 2020 results, released April 16, missing consensus estimates on both the top line (revenue of $9.49 missed by $330 million) and the bottom line (EPS of $1.01 missed by $0.14). With that said, the results held up fairly well as one can see in the graphic down below, with net revenues down 8% year over year, and income before taxes down by 27%–better than its large bank peers. Return on average tangible common equity was 9.7% in the quarter, well above levels of just a few years back (and again better than large bank peers in the quarter), showing the progress that Morgan Stanley has made in improving its return profile.

Image Source: Morgan Stanley 1Q2020 Earnings Supplement

As one can see above, the Wealth Management segment held up the best, while Institutional Securities had more cost and bottom-line pressure. Management has committed to no layoffs this year (despite lower investment banking activity, for example) in the face of the COVID-19 pandemic, so the bank will be focusing on cutting back on non-compensation expenses as it moves forward through the year.

Because Morgan Stanley is so reliant on market levels and activity, it is possible that results could come under further pressure as this pandemic-catalyzed recession unfolds. The bounce off the recent market lows, however, shows that the Federal Reserve’s and Congress/Treasury’s actions to reflate the economy and asset markets are very helpful to a firm like this.

It’s also notable that Morgan Stanley hasn’t closely followed closest peer Goldman Sachs (GS) in its drive to become more of a universal bank. While Goldman is pulling back on growth in credit card and unsecured lending, Morgan Stanley is instead sitting on low-risk home loans to very wealthy clients. Morgan Stanley’s bigger concern is that its investment firm clients don’t get caught up in too large of margin calls. While it was an issue in the quarter, it seems the size wasn’t very material despite the wild market gyrations in the quarter. We are maintaining our recently reduced $31.50 fair value estimate.

—

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Matthew Warren does not own any of the securities mentioned. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.