Member LoginDividend CushionValue Trap

|

Dividend Growth Idea Oracle Stepping Up Cloud Investments to Build on Recent Momentum

publication date: Jun 16, 2021

|

author/source: Callum Turcan

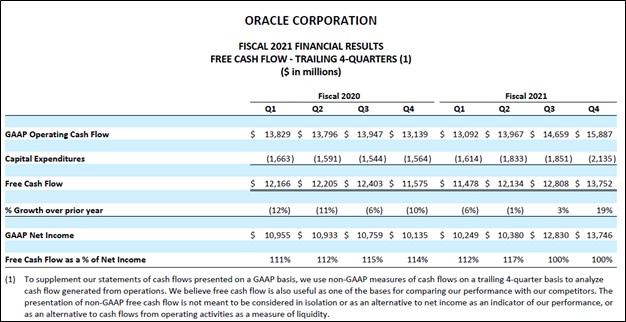

Image Shown: Oracle Corporation’s pivot towards cloud computing offerings continues. We include Oracle as an idea in our Dividend Growth Newsletter portfolio and continue to view its payout growth trajectory quite favorably. Image Source: Oracle Corporation – September 2019 IR Presentation By Callum Turcan On June 15, Oracle Corporation (ORCL) reported fourth quarter fiscal 2021 earnings (period ended May 31, 2021) that beat both consensus top- and bottom-line estimates. The company’s GAAP revenues climbed higher 8% year-over-year and its GAAP operating income grew 5% year-over-year in the fiscal fourth quarter. Oracle cited growth at its Fusion and NetSuite cloud applications businesses along with growth at its Gen2 Cloud Infrastructure business as driving its financial performance in the fiscal fourth quarter. We continue to like Oracle as an idea in the Dividend Growth Newsletter portfolio; shares of ORCL yield ~1.6% as of this writing. Earnings Update Shares of Oracle fell initially after its latest earnings report was published as its earnings guidance for the first quarter of fiscal 2022 came in short of expectations. Oracle plans to further ramp up its cloud computing investments going forward, a strategy that involves doubling its cloud-related capital expenditures this fiscal year. We are supportive of Oracle’s efforts to maintain its momentum in this space, especially as management’s revenue guidance calls for decent single digit-growth during the current fiscal quarter. Here is what management had to say regarding the firm’s fiscal 2022 guidance during Oracle’s latest earnings call (emphasis added): “Now to the guidance. Let me first start with my confidence in the continuation of our revenue growth acceleration for fiscal year 2022. As I’ve said many times over the last two years, our overall revenue growth is continuing to accelerate as our fast-growing cloud business becomes a larger portion of our total revenue. I see total revenue for fiscal 2022 growing faster than fiscal ‘21 with constant currency revenue growth somewhere in mid-single digits. Given our increasing confidence in revenue growth and our unique and differentiated position in the market, we are going to invest back in the business at a greater rate, so we can further accelerate the top line. We also see cloud as being fundamentally a more profitable business compared to on-premise.And as everyone knows, our annual non-GAAP margins of 47%, and that’s what we run the business at, are, in fact, the highest non-GAAP margins of all of our competitors. And we believe that now is the right time to increase our investment to capture market share. As such, we expect to roughly double our cloud CapEx spend in FY 2022 to nearly $4 billion. We are confident that the increased return in the cloud business more than justify this increased investment and our margins will expand over time.” --- Safra Catz, CEO of Oracle For the current fiscal quarter, Oracle is guiding its revenues to grow 3%-5% and for its non-GAAP adjusted EPS to grow 2%-6% in US dollar terms, aided by expected favorable foreign currency movements. In constant currency terms, Oracle expects its revenues to grow 1%-3% and that its non-GAAP EPS will be broadly flat this fiscal quarter. As an aside, the firm’s financial performance in the fiscal fourth quarter benefited from favorable foreign currency movements as well. Oracle reported annual revenue growth at all three of its geographical regions in fiscal 2021, represented by the Americas, Europe/Middle East/Africa, and Asia Pacific. The company’s GAAP revenues increased 4% year-over-year in fiscal 2021 in part due to the strength of its cloud-oriented enterprise resource planning (‘ERP’) offerings such as Fusion ERP and NetSuite ERP. Additionally, its Oracle Cloud Infrastructure (‘OCI’) business was supported by surging demand for its Autonomous Database offering last fiscal year. Building on these successes and making the necessary investments to maintain its momentum may weigh on Oracle’s near-term profitability, though its longer term outlook is bright and getting brighter. Oracle’s GAAP operating income climbed higher 9% year-over-year in fiscal 2021, outpacing its GAAP revenue growth as it kept its operating expenses broadly flat during this period. Financial Strength Maintained Oracle has the financial capacity to make these investments while maintaining its dividend growth trajectory. In fiscal 2021, Oracle generated $13.8 billion in free cash flow and spent $3.1 billion covering its dividend obligations along with $20.9 billion buying back its common stock. At the end of fiscal 2021, Oracle had $46.6 billion in cash, cash equivalents, and marketable securities on hand versus $84.2 billion in short- and long-term debt combined on the books. While Oracle has a sizable net debt position, we view this burden as manageable given its ability to generate sizable “excess” free cash flows after covering its payout obligations and its ample liquidity levels on hand. Historically, Oracle has posted a stellar free cash flow conversion ratio (free cash flows divided by its GAAP net income during a given period) as one can see in the upcoming graphic down below. A free cash flow conversion ratio at or above 100% is quite the feat and highlights the strengths of Oracle’s asset-light business model. Its business requires relatively modest capital expenditures to maintain a certain level of revenues, even when considering the planned ramp up in Oracle’s capital expenditure expectations going forward.

Image Shown: Oracle’s free cash flow conversion ratio is impressive and underpins why we are big fans of the company. Image Source: Oracle – 8-K SEC filing cover the fourth quarter of fiscal 2021 Concluding Thoughts Looking ahead, Oracle should benefit from the eventual reopening of the global economy as ongoing vaccine distribution efforts help put an end to the coronavirus (‘COVID-19’) pandemic. Many enterprises and governments suspended major IT projects in the wake of the pandemic for myriad reasons. When those activities resume in earnest, Oracle will be well-positioned to meet customer demand. Oracle’s pivot towards cloud computing operations continues and its outlook is getting brighter, aided by the company stepping up its investments towards its most promising growth opportunities. We are big fans of Oracle and continue to like shares of ORCL as an idea in our Dividend Growth Newsletter portfolio. ----- Technology Giants Industry - FB, AAPL, GOOG, AMZN, MSFT, CSCO, V, MA, PYPL, INTC, ORCL, QCOM, TWTR, IBM, ADBE, NVDA, CRM, AMD, AVGO, BABA, BKNG, BIDU, TSM, FFIV, TXN, EBAY, ADP, PAYX, MU, KFY, MAN, KLAC, LRCX, AMAT, ADI Related: NOW, CRM, HUBS, WDAY, WORK, DDOG Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free. Callum Turcan does not own shares in any of the securities mentioned above. Apple Inc (AAPL), Cisco Systems Inc (CSCO) and Microsoft Corporation (MSFT) are all included in both Valuentum’s simulated Best Ideas Newsletter portfolio and simulated Dividend Growth Newsletter portfolio. Alphabet Inc (GOOG) Class C shares, Facebook Inc (FB), Korn Ferry (KFY), PayPal Holdings Inc (PYPL) and Visa Inc (V) are all included in Valuentum’s simulated Best Ideas Newsletter portfolio. Oracle Corporation (ORCL) and Qualcomm Inc (QCOM) are both included in Valuentum’s simulated Dividend Growth Newsletter portfolio. Some of the other companies written about in this article may be included in Valuentum's simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

|

0 Comments Posted Leave a comment