Image Source: Oracle Corporation – September 2019 IR Presentation

By Callum Turcan

On June 13, Oracle Corporation (ORCL) reported fourth quarter earnings for fiscal 2022 (period ended May 31, 2022) that beat both consensus top- and bottom-line estimates. The tech giant also provided favorable constant currency revenue growth guidance for its cloud businesses for fiscal 2023. Shares of ORCL initially surged higher in the wake of its latest earnings report before drifting modestly lower along the decline in broader equity markets. We include Oracle as an idea in the Dividend Growth Newsletter portfolio and shares of ORCL yield ~1.9% as of this writing.

Quarterly Update

In the fiscal fourth quarter, Oracle’s GAAP revenues grew by 5% year-over-year and were up 10% on a constant currency basis. The firm noted that on a constant currency basis, its cloud revenue grew by 22% year-over-year with infrastructure cloud revenue up 39%, Fusion ERP cloud revenue up 23%, and NetSuite ERP cloud revenue up 30% last fiscal quarter. Please note its sales growth performance on these fronts was modestly lower when not adjusting for foreign currency headwinds. As an aside, Oracle suspended its business in Russia (RSX) shortly after the Russian invasion of Ukraine in February 2022.

Oracle is in the process of scaling up its faster growing cloud-oriented operations and its operating expenses are growing accordingly. Operating expenses advanced 10% year-over-year in the fiscal fourth quarter (up 12% on a constant currency basis) which led to its GAAP operating income declining by 1%, though its non-GAAP operating income was up 6% on a constant currency basis. The firm’s GAAP diluted EPS came in at $1.16 last fiscal quarter, down 21% year-over-year (and down 14% on a constant currency basis) as a decline in its net income was offset somewhat by a 7% drop in its diluted outstanding weighted average share count.

We appreciate Oracle’s relatively strong performance last fiscal quarter as demand for its cloud-oriented services remains quite strong, even in the face of major exogenous shocks. The company entered fiscal 2023 on relatively strong footing.

Acquisition Update and Net Debt Concerns

In December 2021, Oracle announced it was acquiring healthcare technology provider Cerner through an all-cash deal worth approximately $28.3 billion which closed in June 2022, after the end of Oracle’s fiscal fourth quarter. Though the deal gives Oracle a major foothold in the healthcare space and can be used to generate organic growth opportunities in this realm, we caution that the acquisition further stressed Oracle’s balance sheet.

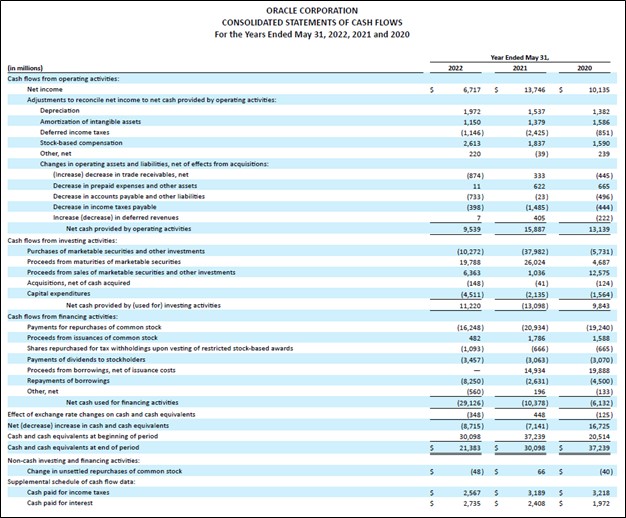

At the end of May 2022, Oracle had $21.9 billion in cash, cash equivalents, and current marketable investments on hand versus $3.7 billion in short-term debt and $72.1 billion in long-term debt, equal to a net debt load of just under $54.0 billion. This net debt load is largely a product of Oracle’s sizable share repurchases, which stood at $16.2 billion in fiscal 2022 and cumulatively totaled $56.4 billion from fiscal 2020-2022. From fiscal 2020-2022, Oracle generated $30.4 billion in cumulative free cash flow (~$10.1 billion on average per fiscal year) which fully covered $9.6 billion in cumulative dividend obligations during this period (~$3.2 billion on average per fiscal year), though large chunks of its share buyback programs were funded by the balance sheet.

In fiscal 2022, Oracle generated $5.0 billion in free cash flow as its capital expenditures increased meaningfully to bring new regional cloud centers online, while its net operating cash flows faced hurdles due to a working capital build, though its free cash flows still handily covered $3.5 billion in dividend obligations during this period. We appreciate Oracle’s strong free cash flow generating abilities in almost any operating environment, though its growing net debt load is concerning.

Going forward, while we do not expect Oracle to negatively impact its stellar dividend track-record as management will likely do all they can to defend the payout (a stated priority of the company), we may proactively remove Oracle from the Dividend Growth Newsletter portfolio.

Image Shown: Oracle has historically fully covered its dividend obligations with its free cash flows, as the firm is a stellar cash flow generator in almost any operating environment. We caution that the firm’s capital expenditure expectations have been steadily increasing in recent years as Oracle seeks to build on the growth momentum seen at its cloud-oriented businesses. Image Source: Oracle – Fiscal 2022 10-K SEC Filing

However, on a positive note, Oracle intends to substantially slow down the pace of its share buybacks to free up capital for deleveraging activities. For reference, during the first three quarters of fiscal 2022, Oracle spent $15.7 billion on share repurchases while spending just $0.6 billion during the final quarter of fiscal 2022. Management had this to say regarding Oracle’s capital allocation priorities and the Cerner deal during Oracle’s latest earnings call (emphasis added, lightly edited):

“At quarter end, we had nearly $22 billion in cash and marketable securities, but that’s lower now that Cerner has closed…

With the completion of the Cerner acquisition, which happened after the end of Q4… we’ve added about $15.8 billion of debt. And we anticipate retaining our investment-grade credit rating, meaning that for the time being, we’re going to focus on reducing our debt balance while continuing our share repurchases at current levels. In addition, I don’t believe the dividend will be impacted at all. Once the debt level has declined, we’ll reexamine share repurchase levels.” — Safra Catz, CEO of Oracle

We appreciate Oracle taking its foot off the gas pedal as it concerns share repurchases, and we would like to see the company pursue substantial deleveraging activities before resuming its share buybacks at anything closely resembling its historical pace. Management also had this to say during Oracle’s latest earnings call in response to an analyst’s question regarding share repurchases (emphasis added):

“We bought back $600 million this past quarter. I think we bought back about $600 million the previous quarter. I expect to do about the same this quarter. Usually, I don’t give you the number in advance. But since previous quarter, to those 2, we did $7 billion and a couple of $8 billion. We’re not going to be at that level. We’ll be at the $600 million for a few quarters until I see where our debt levels are. And so $600 million a quarter is probably what I’m targeting. It could be a little bit more potentially but that’s kind of where I’m at.” — CEO of Oracle

Guidance Update

Oracle’s CEO also noted that the firm’s capital expenditures this fiscal year are expected to “be a little bit more than” what Oracle spent last fiscal year, though the company should continue to generate substantial free cash flows in fiscal 2023. In turn, that will enable the Oracle to steadily chip away at its large net debt load.

These investments are being utilized to bring additional data centers online in what the firm refers to as cloud regions, which set the stage for Oracle to further grow its various cloud-oriented businesses in the relevant regions. Management noted that Oracle has 38 cloud regions across 20 countries and intends to add six more in fiscal 2023.

Looking ahead, management is upbeat on Oracle’s growth prospects. During the firm’s latest earnings call, managed noted that Oracle forecasts its cloud revenue will grow more than 30% in fiscal 2023 on an organic and constant currency basis. Additionally, Oracle expects its cloud service and license support business will experience “growth acceleration and could well see double-digit organic growth” which is a welcome sign. Sustained revenue growth will go a long way in supporting Oracle’s cash flow performance over the long haul.

Concluding Thoughts

Oracle’s underlying business is performing well, though we remained concerned about its bloated balance sheet. The firm provided favorable guidance for the current fiscal quarter, aided by the addition of Cerner to its operations, though headwinds from inflationary pressures, geopolitical tensions, and expected increases in its capital expenditures and operating expenses need to be monitored. We are keeping Oracle as an idea in the Dividend Growth Newsletter, for now.

—–

Technology Giants Industry – FB, AAPL, GOOG, AMZN, MSFT, CSCO, V, MA, PYPL, INTC, ORCL, QCOM, TWTR, IBM, ADBE, NVDA, CRM, AMD, AVGO, BABA, BKNG, BIDU, TSM, FFIV, TXN, EBAY, ADP, PAYX, MU, KFY, MAN, KLAC, LRCX, AMAT, ADI, SIMO

Tickerized for ORCL, CERN, XLV, CRM, WDAY, COUP, DOCU, HPE, SNOW, NOW, ADBE, ADSK, WMW, SPLK, TEAM, DDOG, ESTC, SUMO, NET, SMAR, ASAN, PCOR, LAW, UPLD, DBX, CRWD, VRNS, CHKP, S, IRNT, NEWR, SAP, ZM, BOX, FSLY, NABL, NLOK, NTX, QLYS, SWI, TDC, BASE, NTNX

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Callum Turcan owns shares of DIS, META, GOOG, VRTX and XLE and is long call options on META and DIS. Apple Inc (AAPL), Cisco Systems Inc (CSCO), Microsoft Corporation (MSFT), and Health Care Select Sector SPDR Fund ETF (XLV) are all included in both Valuentum’s simulated Best Ideas Newsletter portfolio and simulated Dividend Growth Newsletter portfolio. Alphabet Inc (GOOG) Class C shares, Meta Platforms Inc (META), Korn Ferry (KFY), PayPal Holdings Inc (PYPL) and Visa Inc (V) are all included in Valuentum’s simulated Best Ideas Newsletter portfolio. Oracle Corporation (ORCL) and Qualcomm Inc (QCOM) are both included in Valuentum’s simulated Dividend Growth Newsletter portfolio. Meta Platforms, Oracle Corporation, and Taiwan Semiconductor Manufacturing Company Limited (TSM) are all included in Valuentum’s simulated ESG Newsletter portfolio. Some of the other companies written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.