Image Source: Realty Income Corporation – July 2020 Institutional Investor Presentation

By Callum Turcan

The real estate investment trust (‘REIT’) Realty Income Corporation (O) recently provided investors with some key financial and operational updates. Realty Income primarily invests in single-tenant commercial properties in the US, Puerto Rico, and the UK, and we include shares of O as a holding with a modest weighting in the Dividend Growth Newsletter portfolio.

Most of Realty Income’s tenants have continued to pay rent during the ongoing coronavirus (‘COVID-19’) pandemic, though tenants in select categories have been unwilling or unable to pay during these challenging times. In particular, Realty Income’s movie theater tenants did not pay rent in June or the second quarter of 2020, according to the REIT.

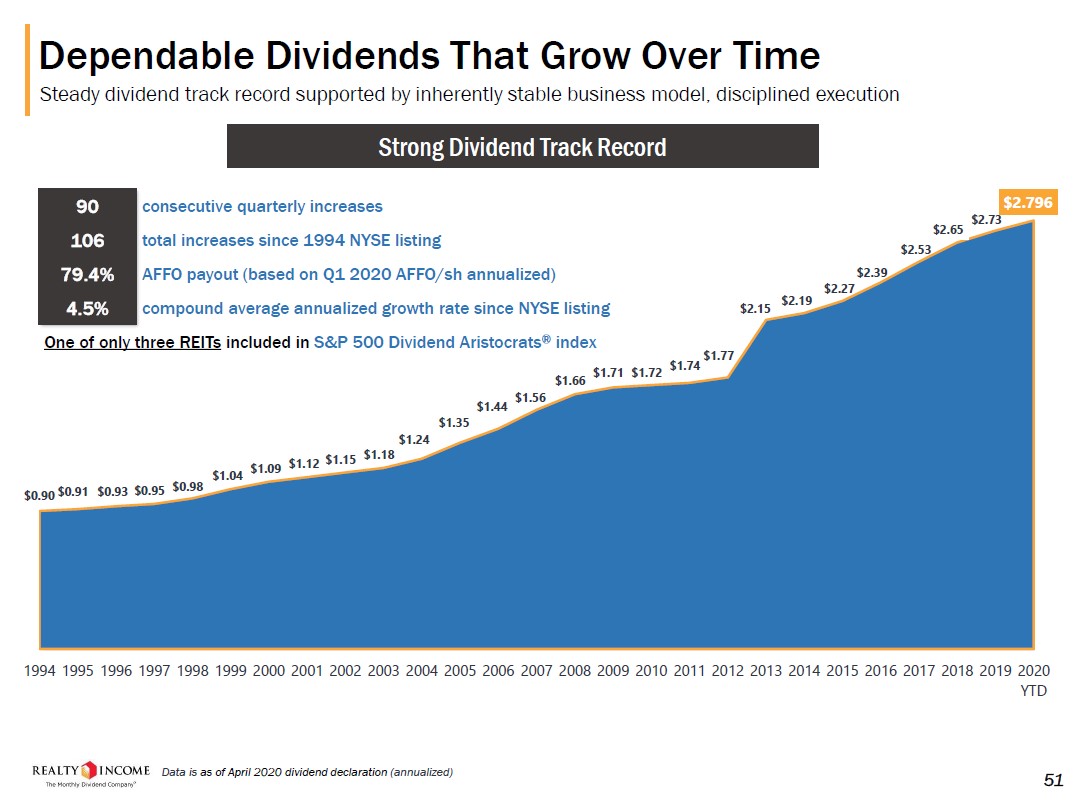

Realty Income’s ongoing access to debt markets combined with its ample borrowing capacity under its revolving credit facility has enabled the company to keep making good on its monthly dividends during the pandemic. Shares of O yield ~4.7% on a forward-looking basis as of this writing (at an annualized payout just south of $2.80 per share) after the firm pushed through its 107th monthly dividend increase in June 2020.

Rent Collection Update

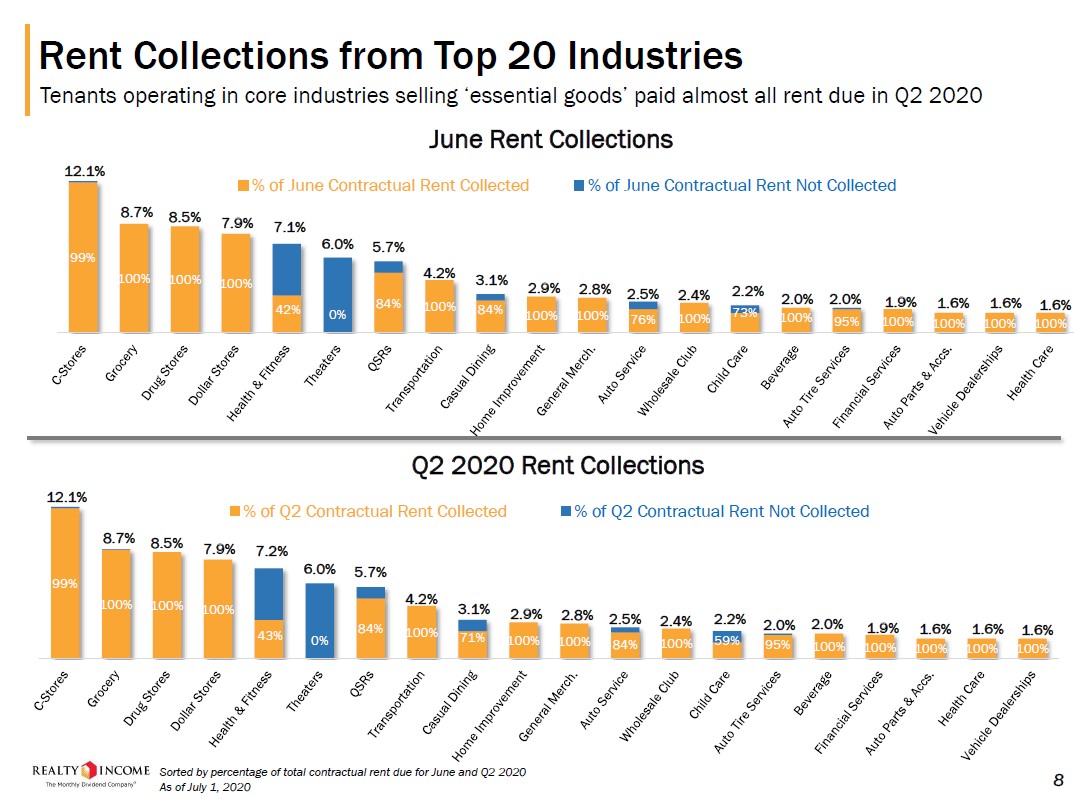

On July 2, Realty Income provided an update on its rent collection performance during the second quarter of 2020. The REIT saw its portfolio-wide rent collection performance weaken from April to May before rebounding in June on a sequential basis. Realty Income collected on just over 85% of its contractual rent across its total portfolio in the second quarter as the pandemic took its toll, though we appreciate the rebound in its rent collection performance during the final month of the second quarter. The REIT’s investment grade tenants, for the most part, continued to make good on their rent obligations during the early stages of the ongoing pandemic.

Image Shown: An overview of Realty Income’s rent collection performance during the second quarter of 2020 on both a quarterly and monthly basis. Image Source: Realty Income – 8-K SEC Filing

In the upcoming graphic down below, Realty Income highlights its rent collection performance by industry during June and the second quarter of 2020. The lack of rent payments from its movie theater tenants weighed heavily on Realty Income’s second quarter financial performance and that will likely continue going forward given that the REIT’s movie theater tenants continued to not pay rent in June. Movie theaters have largely stayed closed during the pandemic and may not reopen for some time as several big movies have been delayed recently including The Walt Disney Company’s (DIS) Mulan and AT&T Inc’s (T) Tenent (via its Warner Bros. subsidiary), neither of which are expected to screen until August at the earliest.

Image Shown: An overview of Realty Income’s rent collection performance by industry for June and the second quarter of 2020. Image Source: Realty Income – July 2020 Institutional Investor Presentation

AMC Theaters and Regal Theaters, owned by AMC Entertainment Holdings Inc (AMC) and Cineworld Group plc (CNNWF) respectively, each represented about 2.9% of Realty Income’s annualized rent (as of the end of the first quarter of 2020). While Realty Income expects that movies will continue to represent an attractive low cost entertainment option for US households in the long term, there is no getting around the fact that the industry remains financially stressed as virtually all its cash flows have dried up. Even if movie theaters do reopen in the US, it is not for sure that occupancy rates would allow for those facilities to generate meaningful cash flows keeping in mind that occupancy rates are going to be severely curtailed according to various company’s announced policies.

Beyond problems at its ‘theater’ tenants, many of Realty Income’s ‘health & fitness,’ ‘casual dining,’ and ‘child care’ tenants have not been paying rent over the past few months, likely due to pandemic containment efforts forcing those locations to close down (hurting the tenant’s ability to pay). Realty Income’s ‘QSR’ [or quick-service restaurant] tenants have for the most part continued to pay rent, supported by the QSR industry’s ability to shift towards a drive-through/delivery model. Additionally, many of Realty Income’s tenants in different industries (‘home improvement’, ’financial services,’ and ‘health care’ among others) have continued to pay rent, highlighting the strength of its diverse customer base.

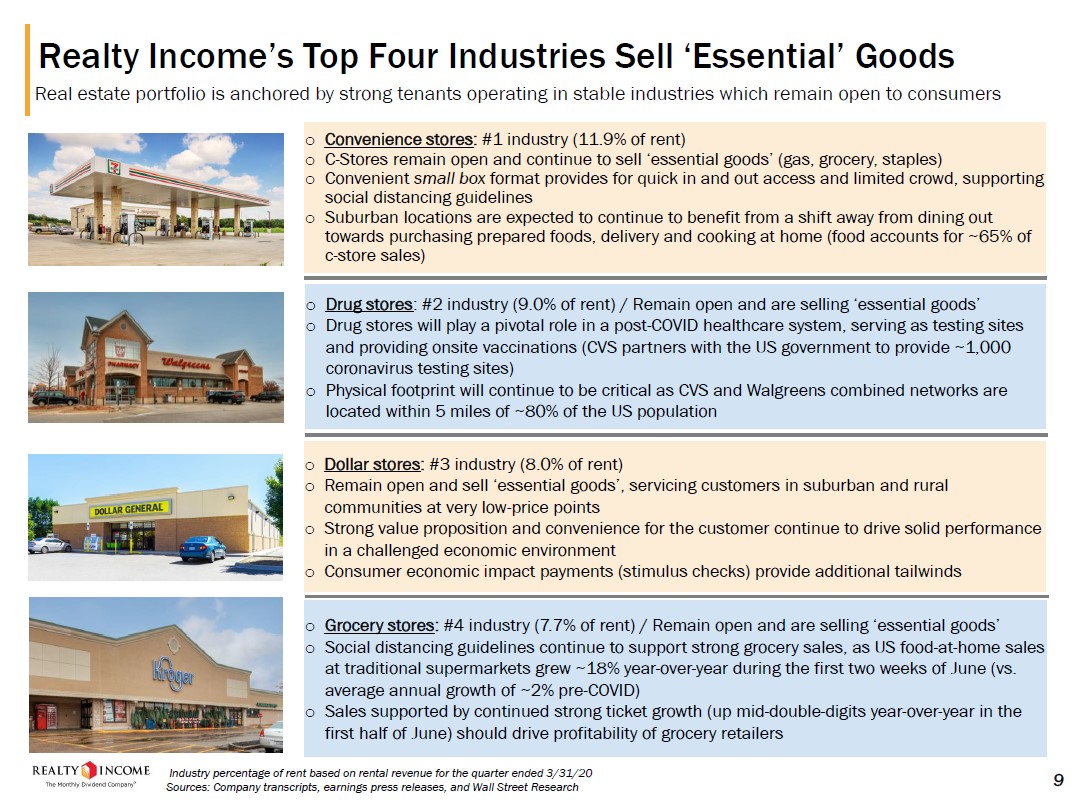

Realty Income’s “top four industries” continue to hold up well (convenience stores, drug stores, dollar stores, and grocery stores) as surging demand for consumer staples products supported the financial performance of firms within those industries. That will likely continue being the case in the US going forward, in our view. Combined, tenants in those four industries represented over 37% of Realty Income’s annualized rent revenues in the second quarter of this year.

In the upcoming graphic down below, Realty Income highlights why the REIT is optimistic its tenants in these four industries will continue to meet virtually all of their contracted rent obligations as was the case in the second quarter (out of the four top industries, only one did not report 100% rent collection last quarter and that was convenience stores at ~99%).

Image Shown: Realty Income’s convenience store, drug store, dollar storage, and grocery store tenants continued to make good on virtually all of their rent obligations in the second quarter of 2020 (at least the rents owed to Realty Income). Image Source: Realty Income – July 2020 Institutional Investor Presentation

Financial Update

Realty Income announced it would raise ~$0.35 billion by issuing 3.250% Notes due 2031 at a premium (108.241% of the principal amount for an effective yield to maturity of 2.341%) in early-July. The REIT intends on using the proceeds to pay down its $3.0 billion revolving credit line which was drawn by ~$0.6 billion as of July 1, 2020, according to its prospectus. That prospectus also noted that Realty Income had ~$0.1 billion in cash on hand as of July 1 and a ~$0.3 billion term deposit (a cash-like asset) coming due on July 24. The bond issuance is expected to close on July 16.

As of July 1, Realty Income had roughly $2.4 billion in borrowing capacity remaining on its revolving credit line, which matures March 2023. That revolver provides the REIT with ample access to liquidity to ride out the storm caused by COVID-19. Given Realty Income’s high quality investment grade credit ratings (A-/A3/BBB+) supported by stable outlooks, the REIT should retain access to capital markets at attractive rates going forward, particularly debt markets.

Concluding Thoughts

Though these are challenging times, Realty Income remains committed to meeting its dividend obligations. Given Realty Income’s apparent access to debt markets at attractive rates, its ample access to liquidity provided by its revolving credit line, and its ability to continue collecting rent from the vast majority of its tenants (meaning its cash flows are holding up relatively well given the circumstances), the REIT appears well-positioned to continue meeting its dividend obligations. The modest payout increase pushed forward in June 2020 was a sign of that commitment. When movie theaters begin to reopen (and better yet, if a COVID-19 vaccine materializes), Realty Income’s rent collection performance should improve materially which in turn will support its cash flow outlook. After the market closes on August 3, Realty Income will publish its second quarter earnings report.

—–

Retail REIT Industry – CONE DLR FRT O REG SPG WPC

Related: AMC, CNNWF, DG, VNQ, SCHH, SRVR, SPY, RTL, NETL, T

—–

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Callum Turcan does not own shares in any of the securities mentioned above. Realty Income Corporation (O) and Digital Realty Trust Inc (DLR) are both included in Valuentum’s simulated Dividend Growth Newsletter portfolio. Dollar General Corporation (DG) and The Walt Disney Corporation (DIS) are both included in Valuentum’s simulated Best Ideas Newsletter portfolio. Digital Realty Trust, Vanguard Real Estate ETF (VNQ), and AT&T Inc (T) are all included in Valuentum’s simulated High Yield Dividend Newsletter portfolio. Both the Best Ideas Newsletter and Dividend Growth Newsletter portfolios include a SPDR S&P 500 ETF Trust (SPY) put option holding with a $295 per share strike price that expire on August 21, 2020. Some of the other companies written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.