Image Source: Valuentum

The embattled department store Macy’s suspended its dividend and drew down its revolving credit line on March 20 in order to shore up its financial position in the face of the ongoing coronavirus (‘COVID-19’) pandemic. All of Macy’s physical stores were temporarily closed on March 18, though some might shut down for good given the company’s financial woes. The fair value estimate of Macy’s is heavily dependent on factors well outside the control of management, and considering the US economy and global economy at-large are sliding toward a pandemic/leverage induced recession/depression, we aren’t optimistic on Macy’s ability to unlock the (fair) value of its real estate. Any real estate sales done in the foreseeable future will likely be at a discount to their fair value. As the firm continues to burn through cash–there’s a very high probability Macy’s will continue to generate negative free cash flows until the “cocooning” of households ends–the clock is working against Macy’s. We are staying away from the name.

By Callum Turcan

The embattled department store Macy’s Inc (M) suspended its dividend and drew down its revolving credit line on March 20 in order to shore up its financial position in the face of the ongoing coronavirus (‘COVID-19’) pandemic. All of Macy’s physical stores were temporarily closed on March 18, though some might shut down for good given the company’s financial woes. Macy’s problems aren’t unique, with JCPenney Company Inc (JCP) reportedly considering a Chapter 11 filing given its hefty net debt load and untenable financial situation. JCPenney exited its fiscal 2019 (period ended February 1, 2020) with over $3.7 billion in total debt, inclusive of short-term debt, versus less than $0.4 billion in cash and cash equivalents on hand.

Since March 20, Macy’s has cut executive pay (announced March 25), furloughed most of its workforce save for a small portion handling e-commerce sales and other operations (announced March 30), and aggressively scaled back capital expenditures. Additionally, the firm pulled its guidance for fiscal 2020 given the high level of uncertainty going forward. At the end of the company’s fiscal 2019 (period ended February 1, 2020), Macy’s had 123,000 full- and part-time employees and ~8% of those employees were represented by unions. As part of the furlough process, Macy’s will continue to provide healthcare benefits to its employees enrolled in its healthcare program through at least May.

Financial Overview

Macy’s operates the Macy’s, Bloomingdales, and Bluemercury brands, and its net merchandise sales have slipped modestly over the past couple years, falling from over $24.9 billion in fiscal 2017 to under $24.6 billion in fiscal 2019, with a ~$0.1 billion increase in credit card revenues (which came in just below $0.8 billion in fiscal 2019) offsetting some of that decline. However, please note Macy’s generated $28.1 billion in GAAP net sales in fiscal 2014 (versus $25.3 billion in fiscal 2019), indicating that its falling sales are part of a long-term trend.

While Macy’s has (arguably) held up significantly better than some of its worst performing peers (JCPenney and Sears Holding Corporation [SHLDQ] to name two) that hasn’t meant much in an industry in secular decline. The macroeconomic backdrop in the US was benign from 2014 to early-2020 before the pandemic hit; however, rising nominal GDP and the rise in total consumer spending didn’t filter into improving financial results at Macy’s. As it relates to GAAP operating income, Macy’s performance in that arena dropped from $2.6 billion in fiscal 2014 to $1.0 billion in fiscal 2019. During this period, Macy’s witnessed its free cash flows drop from $1.9 billion to $0.7 billion.

With its physical stores closed and keeping high fixed costs in mind, the company’s financial outlook is dour but not quite dire given its extensive real estate holdings. At the end of fiscal 2019, Macy’s had $0.7 billion in cash and cash equivalents on hand versus $0.5 billion in short-term debt and $3.6 billion in long-term debt. Fully drawing down its $1.5 billion credit line in March 2020 should help enhance its liquidity position given that revolver doesn’t mature until May 2024.

Real Estate Consideration

Macy’s real estate assets offers some security on this front with its net property and equipment balance totaling $6.6 billion at the end of fiscal 2019. Please note that this is the book value of Macy’s real estate assets, which isn’t necessarily the fair value of those properties. Research firm Cowen estimates that the fair value of Macy’s real estate assets stood at ~$16 billion in late-2017 (near a time when Macy’s ‘property and equipment – net’ carried a book value of ~$6.7 billion as of February 3, 2018), keeping in mind Macy’s has divested various properties since then while making upgrades to others. The value of Macy’s remaining real estate assets is immensely important, and not easy to quantify given the ongoing pandemic and lack of obvious buyers in the current environment.

To shore up its financial position, Macy’s has been selling off some of its real estate holdings and that includes its Downtown Seattle location (a gain of $52 million was recorded from that sale in fiscal 2019) and its I. Magnin building in Union Square San Francisco (a gain of $178 million was recorded from the sale in fiscal 2018). Property and equipment sales (namely real estate) generated cash proceeds of $185 million in fiscal 2019 and $885 million in the previous two fiscal years combined.

At the end of fiscal 2019, Macy’s operated 775 stores across 43 US states, D.C., Guam, and Puerto Rico (most of those are branded as Macy’s locations). As an aside, please note that Macy’s has licensing agreements in a couple of Middle Eastern countries (Dubai within the UAE and Kuwait). Here’s a key excerpt from its Fiscal 2019 Annual Report (emphasis added):

As of February 1, 2020, the operations of the Company included 775 store locations in 43 states, the District of Columbia, Puerto Rico and Guam, comprising a total of approximately 120 million square feet. At these locations, store boxes consisted of 342 owned boxes, 384 leased boxes, 108 boxes operated under arrangements where the Company owned the building and leased the land and five boxes of partly owned and partly leased buildings. All owned properties are held free and clear of mortgages. Pursuant to various shopping center agreements, the Company is obligated to operate certain stores for periods of up to 15 years. Some of these agreements require that the stores be operated under a particular name.

Most leases require the Company to pay real estate taxes, maintenance and other costs; some also require additional payments based on percentages of sales and some contain purchase options. Certain of the Company’s real estate leases have terms that extend for a significant number of years and provide for rental rates that increase or decrease over time.

We caution that should Macy’s attempt to sell off a lot of real estate all at once, especially at a time of distress in the retail industry and economy at-large (i.e. when many other companies, particularly retail firms, are also attempting to sell off real estate and there aren’t many buyers out there), it will become hard to get fair value for those assets (meaning those properties would need to be sold off at a discount). Additionally, Macy’s has had success selling off properties in top tier locales but selling off properties in less attractive locations is a much tougher proposition regardless of the macroeconomic backdrop.

As it relates to the estimated fair value of the common stock of Macy’s, our fair value estimate range is quite wide ($1 per share in the bear case, $9 per share in the bull case) to reflect the high degree of uncertainty in the firm’s outlook. Should Macy’s be able to sell off some of its real estate holdings at prices estimated by Cowen, then the firm’s shares would look downright cheap at current levels. However, should Macy’s find it hard to locate buyers for its properties given the ongoing structural headwinds facing physical retailers and the dour/dire macroeconomic backdrop, then it’s clear why shares of M have moved aggressively lower over the past year. Meaningfully negative free cash flows will further stress its financials and will likely ding its fair value estimate over time as its balance sheet strength erodes. We aren’t optimistic that the US economy will witness a “V-shaped” rebound.

Reportedly, Macy’s is seeking to borrow against its real estate holdings to raise additional funds during these harrowing times. Nordstrom Inc (JWN) recently pursued a similar move; however, please note that the coupon Nordstrom is paying on those secured bonds is quite high at 8.75% on a $600 million offering. As Nordstrom exited its fiscal 2019 (period ended February 1, 2020) with less than $0.9 billion in cash on hand versus almost $2.7 billion in long-term debt (and no short-term debt), its financial position wasn’t horrible (though we at Valuentum strongly prefer net cash balances as we’ve often stated in the past) highlighting the “premium” creditors are demanding from retailers in terms of interest payments (due to the risk the creditors are taking on by lending to the space). Macy’s spent over $0.2 billion on its cash interest expenses in fiscal 2019.

Pension Plan Considerations

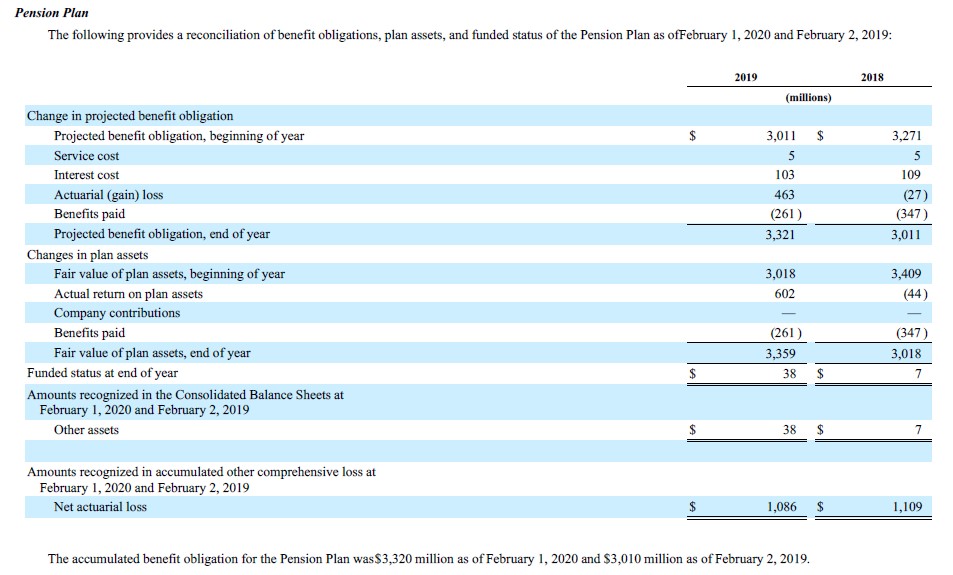

Macy’s transitioned from a defined benefit plan to a defined contribution plan in calendar year 2012-2013; however, it continues to have legacy liabilities that are important to keep aware of. A saving grace for Macy’s is that its pension plan was fully funded at the end of fiscal 2019. In the upcoming graphic down below, note that the ‘fair value of plan assets, end of year’ exceeded the ‘projected benefit obligation, end of year’ line-item to the tune of $38 million at the end of fiscal 2019, up from a surplus of $7 million at the end of fiscal 2018.

Image Shown: Macy’s pension plan was considered fully funded at the end of its latest fiscal year. Image Source: Macy’s – Fiscal 2019 Annual Report

Lower interest rates due to zero interest rate policies (‘ZIRP’) will likely make it harder to earn a nice return on the ‘plan assets’ over the medium- and long-term, and that could create a scenario where Macy’s would need to occasionally make meaningful cash contributions to the plan (which the firm didn’t need to do in fiscal 2018 or fiscal 2019, given its large ‘actual return on plan assets’ in fiscal 2019). These pension liabilities are significant and should the pension portfolio’s return come in below expectations going forward, that could place stress on the firm’s financials. Here’s a key excerpt from Macy’s Fiscal 2019 Annual Report:

The Company’s assumed annual long-term rate of return for the Pension Plan’s assets was 6.50% for 2019, 6.75% for 2018 and 7.00% for 2017 based on expected future returns on the portfolio of assets. For 2020, the Company is lowering the assumed annual long-term rate of return to 6.25% based on expected future returns of the portfolio of assets. The Company develops its expected long-term rate of return assumption by evaluating input from several professional advisors taking into account the asset allocation of the portfolio and long-term asset class return expectations, as well as long-term inflation assumptions. Pension expense increases or decreases as the expected rate of return on the assets of the Pension Plan decreases or increases, respectively. Lowering or raising the expected long-term rate of return assumption on the Pension Plan’s assets by 0.25% would increase or decrease the estimated 2020 pension expense by approximately $7 million.

Over the past several fiscal years, Macy’s has been forced to lower its assumed annual long-term rate of return for the Pension Plan’s assets and Macy’s continued to do so in fiscal 2020. With that in mind, a 6.25% assumed rate of return over the long-term isn’t terribly optimistic but given that US Treasuries and investment grade rated bonds are yielding way below that, it’s possible even subdued portfolio return expectations will prove hard to meet.

Concluding Thoughts

The fair value estimate of Macy’s is heavily dependent on factors well outside the control of management, and considering the US economy and global economy at-large are sliding toward a pandemic/leverage induced recession/depression, we aren’t optimistic on Macy’s ability to unlock the (fair) value of its real estate. Any real estate sales done in the foreseeable future will likely be at a discount to their fair value. As the firm continues to burn through cash–there’s a very high probability Macy’s will continue to generate negative free cash flows until the “cocooning” of households ends–the clock is working against Macy’s. We are staying away from the name. Investors interested in retail should take a look at Best Ideas Newsletter portfolio holding Dollar General Corporation (DG) which we recently covered in this article here.

———-

Dollar Store and Department Store Industries – KSS M JWN BIG DG DLTR PSMT

Specialty Retailers Industry – AAN BBBY BBY GME HD LOW LL ODP SHW TSCO WSM

Food Retailing Industry – CASY COST CVS KR SYY TGT WBA WMT

Related: AMZN, FDS, SPY

———-

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Callum Turcan does not own shares in any of the securities mentioned above. Cracker Barrel Old Country Store Inc (CBRL) is included in Valuentum’s simulated Dividend Growth Newsletter portfolio. Dollar General Corporation (DG) is included in Valuentum’s simulated Best Ideas Newsletter portfolio. Some of the other companies written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.