Image Source: GoodRx Holdings Inc – December 2020 IR Presentation

Executive Summary: GoodRx Holdings Inc is a disrupter in the US pharmacy space, and the company went public in September 2020. The firm’s digitally-oriented prescription drug pricing platform generates strong normalized operating income and allows for an impressive cash flow profile. Supported by its pristine balance sheet, GoodRx has the financial firepower to expand into adjacent businesses to further extend its growth runway. While meaningful competitive threats are a concern, such as those posed by Amazon Inc entering the online pharmacy space, GoodRx has significant competitive advantages over its peers and benefits from the network effect. The company’s active monthly user base has grown at an impressive clip during the past several years, and the firm has a number of avenues to generate meaningful upside. The company’s total addressable market is enormous.

By Callum Turcan

In September 2020, GoodRx Holdings Inc (GDRX) went public with the goal of helping Americans reduce their health care expenses. The consumer-facing digital platform GoodRx operates under its namesake brand and offers users the ability to search and compare drug prices in order to faciliate a more competitive prescription drug market. Additionally, the platform also offers coupons when applicable to help users further reduce prescription costs. According to GoodRx, “15 million people visit GoodRx every month to learn about and save on their healthcare” expenses. Since GoodRx was founded in 2011, the company has saved consumers about $25 billion according to commentary provided within its third quarter of 2020 earnings report.

Numerous Large Growth Opportunities

GoodRx sees its total addressable market (‘TAM’) standing at approximately $800 billion ($524 billion opportunity in prescriptions, $30 billion opportunity in pharmaceutical manufacturing solutions, and a $250 billion opportunity in telehealth). The company had roughly 4.9 million active monthly users during the third quarter of 2020, up sharply from roughly 0.7 million active monthly users as of the first quarter of 2016. There is ample room for additional growth on this front, in our view.

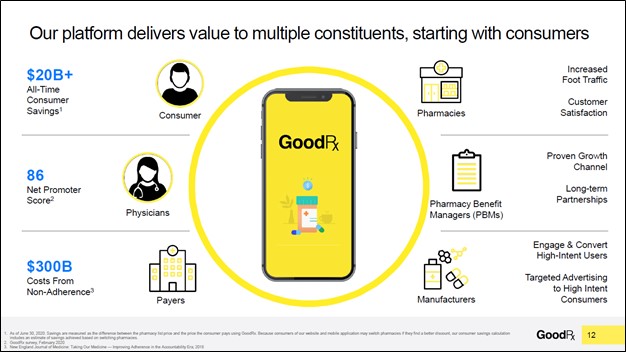

GoodRx benefits from a network effect as a growing active user base encourages large healthcare giants to partner with GoodRx. The increased number of healthcare companies improves the value of GoodRx’s offerings, and then even more users are then drawn to utilize GoodRx’s digital platform. This network effect of more consumers driving more healthcare partners driving more consumers driving more healthcare partners has continued for years, becoming a key advantage locking out new entrants that are unable to build such a virtuous cycle (“feedback loop”).

The upcoming graphic down below provides an overview of this dynamic in action.

How GoodRx benefits from the network effect. Image Source: GoodRx – December 2020 IR Presentation.

Business Overview

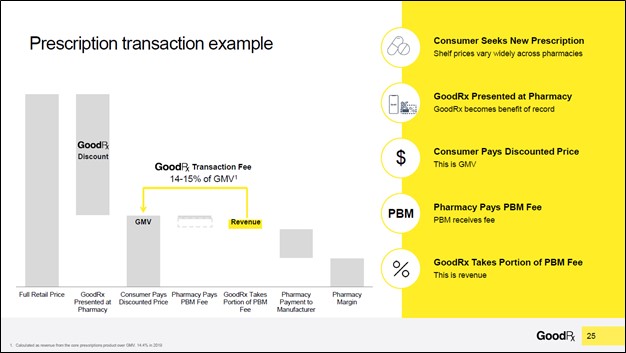

GoodRx primarily generates revenues through its prescription drug offerings. The company’s digital platform aggregates drug pricing data from a variety of healthcare sources, with the result being a GoodRx code that can be used to fill a prescription (a prescription from a physician is also required). When a GoodRx code is used at a US pharmacy, GoodRx receives a fee from the relevant company, namely pharmacy benefit managers (‘PBMs’). Please note that GoodRx codes and coupons can be accessed via its digital app which makes its platform easier to use.

Image Shown: How GoodRx’s digital prescription drug platform generates revenues for the company. Image Source: GoodRx – December 2020 IR Presentation

The difference between the list price of the drug at the pharmacy and negotiated price by the relevant PBMs or other entity that is accessible via GoodRx’s digital platform is the opportunity GoodRx is tapping into, as some of those “savings” are passed back to the firm in the form of fees (as GoodRx effectively helps save both consumers and PBMs some money by reducing prescription drug costs). In 2019, about 94% of GoodRx’s revenues were generated via these prescription transactions.

Since 2016, over 80% of the transactions conducted via its prescription offering have been from repeat users, highlighting the potential to build sizable recurring sales from this business model. Recurring revenue streams provide for stronger and more resilient cash flow profiles given the greater visibility of the company’s future financial performance. The upcoming graphic down below highlights the impressive user growth and rising gross merchandise value (‘GMV’) seen at GoodRx’s digital prescription drug pricing platform.

Image Shown: GoodRx’s core business has posted stellar growth over the past few years and we see room for significant upside here going forward. Image Source: GoodRx – December 2020 IR Presentation

Growing Its Subscription Business

Over the long term, the company’s goal is to expand into adjacent businesses to extend its growth runway. GoodRx offers subscription services including Gold (launched in 2017) and Kroger Savings (launched in 2018), with some of the fees generated by the latter split with grocery/pharmacy giant Kroger Company (KR). By growing the recurring revenues generated from subscription sales, GoodRx is further enhancing its cash flow profile. GoodRx notes that subscribers to these services, which aim to generate additional savings for its user base, tend to spend significantly more on prescriptions at its digital platform than non-subscribers. Subscriber growth has been strong of late, aided by GoodRx stepping up its sales and marketing budget.

GoodRx’s Gold offering costs $5.99 per month for individuals and $9.99 per month for a family of up to five. Subscribers to this service gain access to over 1,000 prescription medications that are available for under $10. The company recently added a mail order service to its Gold subscription, providing additional convenience and value at a time when home delivery services are in high demand.

Pivoting to the Kroger Savings subscription program, this costs $36 per year for individuals and $72 per year for families of up to six, which allows subscribers to gain access to cheaper prescription medicine prices at Kroger pharmacies. Recently, GoldRx expanded its partnership with Kroger through a multi-year long deal. Here, we would like to highlight the favorable impact the network effect has had on GoodRx’s operations so far.

Partnering Up with Pharmaceutical Manufacturers

Another realm that has been experiencing strong growth of late is GoodRx’s pharmaceutical manufacturer solutions offerings. These services involve GoodRx partnering up with pharmaceutical manufacturers to advertise and integrate affordability offerings for brand name medications, which tend to be quite expensive, across GoodRx’s digital platform. GoodRx generates revenues from the pharmaceutical manufacturers, generally under fixed fee structures with services provided for a fixed period. The company notes growth in this area has been exceptional recently, aided by GoodRx’s expanding user base and new partnerships with pharmaceutical manufacturers.

Roughly 20% of the searches on GoodRx’s digital platform are focused on brand name medications, and some of the affordability solutions include co-pay cards and patient assistance programs. GoodRx has over 30 partnerships with pharmaceutical manufacturers through this offering. The firm recently launched care portals for certain brands that seek to provide its users with better access to information regarding treating their medical conditions and cost savings programs for the relevant medications.

Telehealth Upside

The third big opportunity GoodRx aims to capitalize on is telehealth. These types of services have become a lot more prevalent during the coronavirus (‘COVID-19’) pandemic due in part to the desire for households to socially distance and in part due to the stress the pandemic has placed on health care infrastructure (creating demand for more convenient and effective health care delivery solutions). GoodRx offers its own telehealth service through HeyDoctor and runs the GoodRx Telehealth Marketplace which provides users access to third-party providers.

For reference, telehealth giant Teledoc Health Inc (TDOC) reported that its ‘Total Visits from U.S. Paid Membership’ rose by over 240% year-over-year in the third quarter of 2020. There is room for numerous “winners” in the telehealth space as adoption of telehealth services by US households continues to move in the right direction. As an aside, Teledoc merged with Livongo through a deal worth about $18.5 billion that was completed in October 2020, combining its telehealth offering with Livongo’s data-based health assistance and management programs.

Looking ahead, telehealth offerings are likely to become increasingly popular as US households seek cheaper access to healthcare services and greater convenience, while healthcare insurance companies seek to reduce costs. Overall, health care spending in the US is supported by the “greying of America” demographic trend, with an eye towards the growing cohort of Americans over the age of 65 and over the age of 80. Here is what management had to say about GoodRx’s telehealth operations during the firm’s third quarter of 2020 earnings call (emphasis added):

“We also added mail order services to HeyDoctor, our low cost online telehealth service. In addition, HeyDoctor expanded to provide care for Americans in all 50 states and grew the number of conditions we treat. The combination of convenient online provider visits and our new mail order service gives Americans access to medical professionals and medication all through an integrated online experience at a time when they need it most.” — Trevor Bezdek, Co-Founder and Co-CEO of GoodRx

GoodRx’s management team also noted that HeyDoctor continues to expand the number of conditions that the service can treat and has been focusing on cross-selling its prescription-offerings to users of its telehealth services. The company intends to continue making significant investments in bulking up its telehealth operations as demand for the offering has been strong of late according to management. Operational synergies that arise from GoodRx launching new health care services further enhances its long-term growth outlook, which we appreciate.

Financial Overview

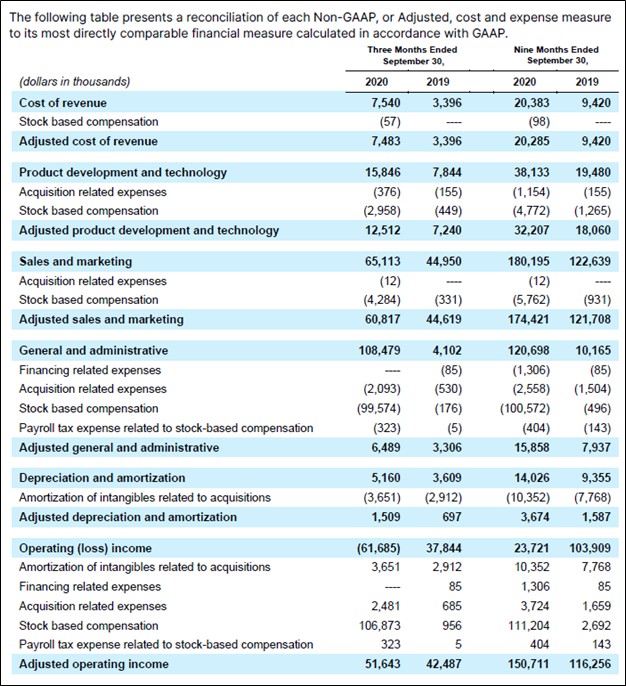

GoodRx reported that its GAAP revenues were up 44% year-over-year during the first three quarters of 2020 (revenue increased 38% in the third quarter), largely due to impressive growth at its prescription-related businesses. While its other offerings grew meaningful, those businesses represented only a small portion of GoodRx’s company-wide revenues. Its GAAP operating income fell during this period due to a sharp increase in its operating expenses, though we still stress that this was largely a product of IPO-related expenses. On a normalized basis, GoodRx generates meaningful positive operating income and its non-GAAP adjusted operating income continued to grow during the first nine months of 2020 on a year-over-year basis, as one can see in the upcoming graphic down below.

Image Shown: On a normalized basis, GoodRx generates meaningful operating income that continued to grow on a year-over-year basis in 2020. Image Source: GoodRx – Third Quarter of 2020 Letter to Shareholders

The company was modestly GAAP profitable on a net income basis during the first three quarters of 2020 and generated about $101 million in free cash flow during this period. We appreciate GoodRx is already on a sustainable financial trajectory.

In our view, the company’s financial performance should improve materially going forward aided by 1) economies of scale (earnings leverage), 2) the aforementioned network effect, 3) the roll off of IPO-related expenses, 4) the launch of new health care-related services, 5) a growing user base, 6) a growing subscription base, 7) the chance for new major partnerships with key health care firms, and 8) secular growth tailwinds. Additionally, there are meaningful barriers to entry in the extraordinarily complex US health care sector, providing GoodRx with competitive advantages over its current and future peers. However, we caution that tech giants like Amazon Inc (AMZN) will pose a growing competitive threat to GoodRx considering Amazon recently launched its own online pharmacy offering and given that Amazon has deep pockets.

At the end of September 2020, GoodRx had $1.1 billion in cash and cash equivalents on hand versus a negligible amount of short-term debt and $0.7 billion in long-term debt. The company’s net cash position provides the firm with a pristine balance sheet, as its total operating lease liabilities (short- and long-term) sat at less than $0.05 billion at the end of this period. We are big fans of GoodRx’s strong financial position, normalized operating income and impressive free cash flow generating abilities.

Guidance and Other Management Commentary

Regarding GoodRx’s near-term outlook, here is what management had to say during the firm’s third quarter of 2020 earnings call (moderately edited, emphasis added):

“I’ll now turn to guidance… For the fourth quarter, we expect revenue of approximately $148 million reflecting 31% year-over-year growth. This would translate to full-year total revenue of approximately $545 million representing a year-over-year growth of 40%.

While we won’t be providing guidance for monthly active consumers regularly, we did want to provide our short-term expectations on this call since our business is still impacted by COVID-19 and because this is such an important driver of our prescription offering. For that reason, we expect our quarter-over-quarter growth of monthly active consumers to be approximately between 4% and 5% for the fourth quarter. Remember that consumers of our other non-prescription transactions offerings, like for example, our high growth subscriptions offering, which delivers two times the contribution do not contribute to our monthly active consumer figure.

Final note on revenue, we won’t be providing guidance for each revenue line item, but just for total revenue, we expect the other revenue line to continue to gradually make up a higher percentage of our revenue.” — Karsten Voermann, CFO of GoodRx

GoodRx expects its active user base and revenues to continue to move in the right direction in the final quarter of 2020, putting the firm in a prime position as we head into 2021. We will stress, however, that growth at its adjacent businesses should be closely monitored going forward, given that management expects these operations to represent a larger percentage of GoodRx’s company-wide financial performance over the coming years.

Concluding Thoughts

Shares of GDRX have largely treaded water since going public as of this writing. The company’s business model is intriguing, and on a normalized basis, its financial performance continues to impress. GoodRx’s growth runway could potentially be enormous, assuming GoodRx is successful in growing its adjacent business segments alongside its prescription drug-oriented business, and there are numerous operational synergies to be had, particularly through deal-making and other efficiency endeavors. Investors seeking speculative capital appreciation upside should keep GoodRx on their radar, though for long-term investors, we caution that competitive threats from tech giants like Amazon always need to be kept in mind.

—–

Disruptive Innovation Industry – W, ZM, SPCE, ROKU, WORK, MNST, SAM, SPLK, PENN, VRSK, ICE, LULU, ESTY, DOCU, UBER, BYND

Health Care Bellwethers Industry – JNJ, WBA, CVS, ISRG, MDT, ZBH, BAX, BDX, BSX, MTD, SYK, BIIB, GILD, ABT, ABBV, LLY, AMGN, BMY, MRK, PFE, VRTX, ZTS, REGN, UNH

Tickerized for GDRX, KR, WBA, CVS, TDOC, AMZN, TGT, WMT, RAD, CAH, MCK, ABC

—–

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ra