There may have been little surprise across the market when GE halved its dividend in its investor update November 13, but shares are selling off after management issued weaker-than-expected EPS guidance for 2018.

By Kris Rosemann

We can’t say we didn’t see this coming for General Electric (GE), a newsletter idea we parted ways with in May of this year as concerns rose over the sustainability of its dividend. It registered a Dividend Cushion ratio of 0.3 and dividend growth and dividend safety ratings of VERY POOOR at the time of the cut. The halving of GE’s dividend did not come as a surprise to most, “GE Cuts Guidance, All Eyes Turn to November 13,” but shares are still facing noteworthy selling pressure in the trading session November 13, immediately following the announcement.

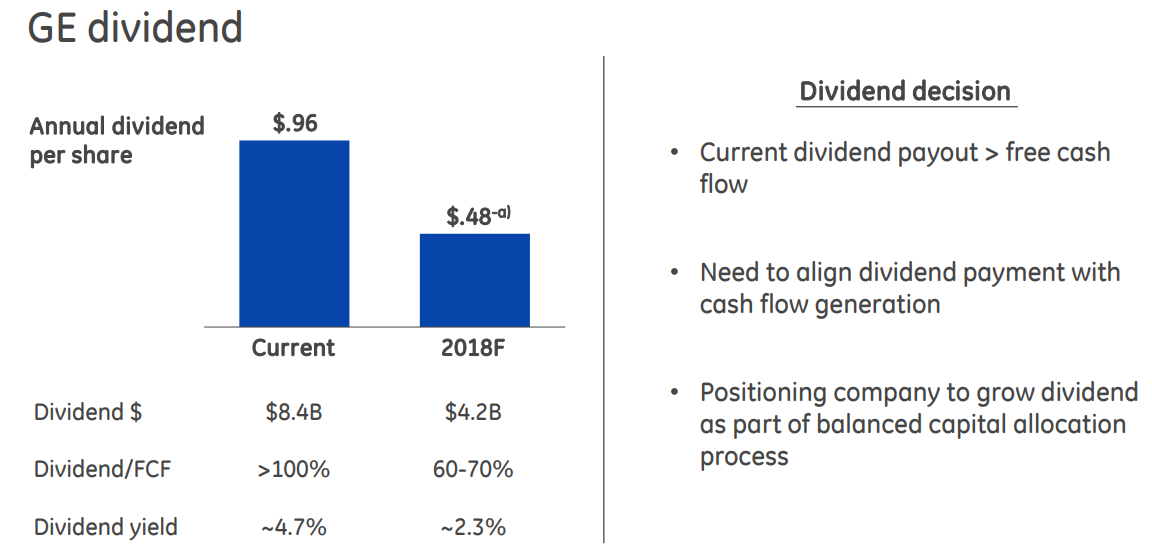

However, the pressure may be more a result of weaker than expected earnings per share guidance for 2018, a year that new CEO John Flannery has requested investors view as a “reset year.” 2018 adjusted EPS is expected to be in a range of $1.00-$1.07, compared to guidance of $1.04-$1.12 for 2017, while free cash flow for 2018 is being targeted at $6-$7 billion–2017 free cash flow is projected to be ~$3 billion. Prior to the dividend cut, such a level of free cash flow in 2018 would imply a material shortfall in free cash flow covering cash dividend obligations. The image below, taken from GE’s investor update presentation, says it all.

Image Source: General Electric

Moving forward, GE will focus on its three core units–aviation, power, and healthcare–which accounted for roughly 58% of total revenue in 2016. Generally speaking, we like the idea that the industrial giant is getting back to the basics in its attempt to turn the business around, but it is not out of the woods yet. We’ll be monitoring progress in its plans to exit $20+ billion in non-core assets, not an immaterial amount of divestitures that come on the heels of its massive portfolio transformation.

We’re still not interested in shares of GE, and though we like the new, or rather refocused, direction the company is heading, there is a meaningful amount of uncertainty and execution risk surrounding its turnaround plans. Its balance sheet remains tremendously bloated, and the new look GE has yet to prove itself as a free cash flow generating machine able to handle such a debt load.

Related: BHGE