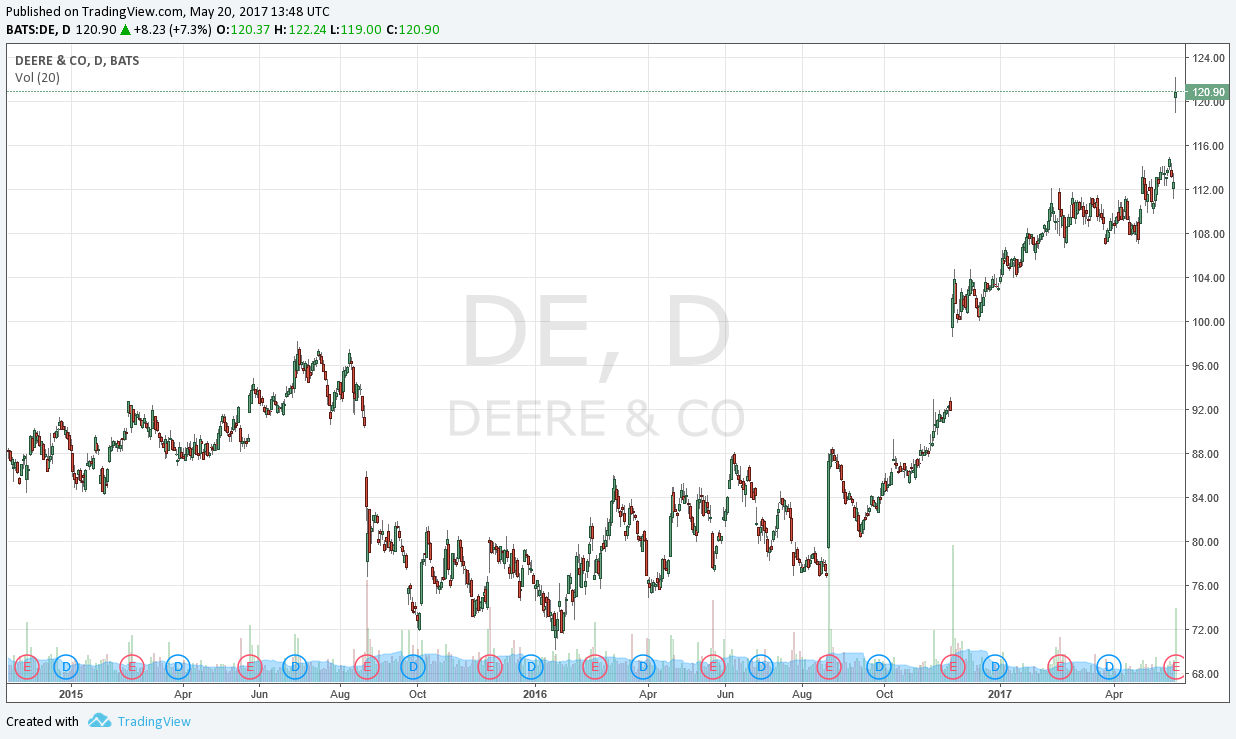

Deere’s equity is charging higher. Let’s look at the reasons why. Will Caterpillar follow?

By Brian Nelson, CFA

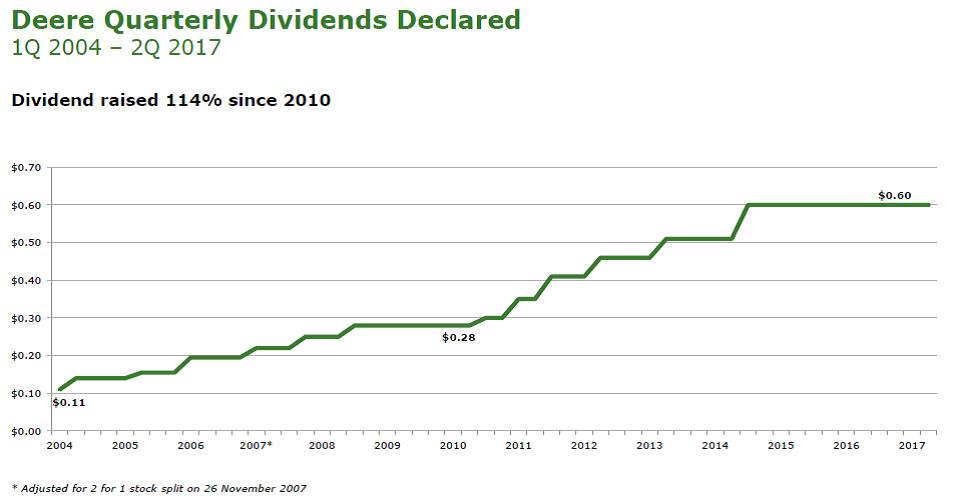

On May 19, agricultural equipment maker Deere (DE) reported solid quarterly results for the period ending April 30 that showed strong improvement in farm and construction equipment demand. Management noted that in its recently-completed second quarter “market conditions showed signs of further stabilization…(and) farm machinery sales in South America experience(ed) a strong recovery,” too. Deere increased its full-year earnings forecast to $2 billion, which it expects to be driven by 9% sales growth. Shares of Deere yield just north of 2% at the moment.