Member LoginDividend CushionValue Trap

|

How About Teva Pharmaceuticals?

publication date: Nov 3, 2014

|

author/source: Brian Nelson, CFA

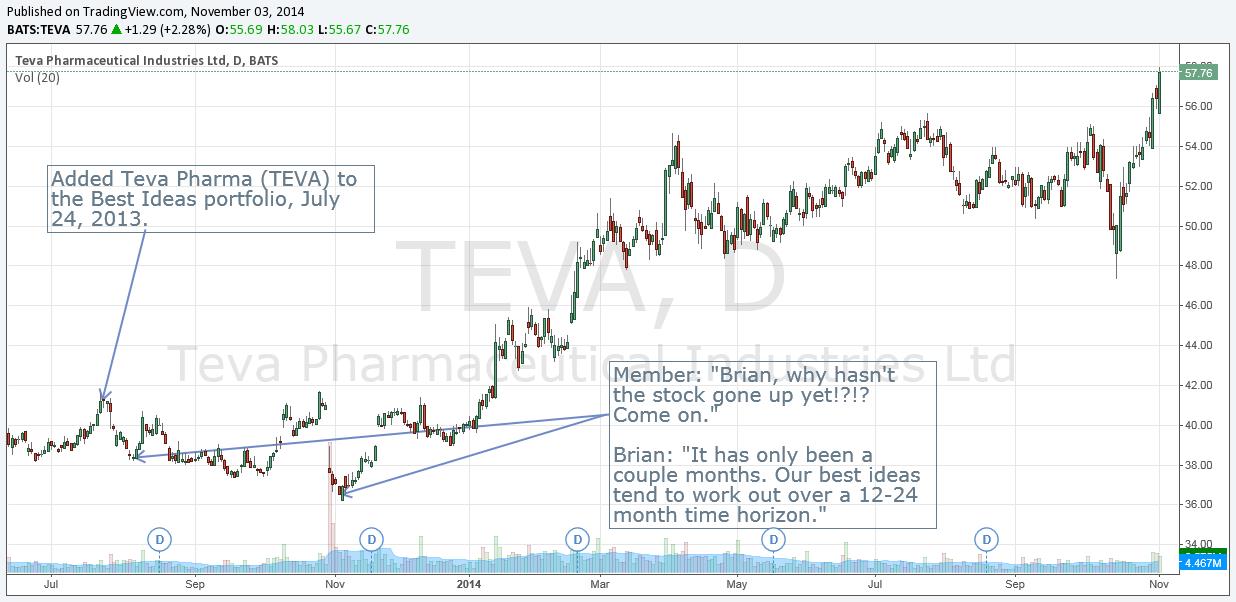

We care very much about our members. We listen to every comment. We read every email. We take everything to heart. We know we’re not supposed to, but we can’t help but be passionate about our work. We strive for your success, and we take failure personally. There are some investors that want our best ideas to work out yesterday. That’s just not going to happen. Aside from yesterday being in the past, our best ideas tend to work out over a 12-24 month time period. This is a reasonable time period to expect price-to-fair-value convergence on stocks with good momentum. From our experience, this is the time period in which the Valuentum process has its greatest efficacy, and no system is perfect. Teva Pharma’s (TEVA) recent stock price performance has put into perspective the up’s and down’s of the equity research business. The firm’s stock price trajectory also highlights one of the many pitfalls that investors fall into: impatience. Even when analysts and ‘stock pickers’ are right, there will be a time when they may look like they were wrong. For one, the odds of timing the price bottom of a stock purchase are slim to none – in fact, investors should set expectations that a ‘best idea’ could fall another 5%-10% or more before that ‘best idea’ eventually recovers and converges to intrinsic value…over time (see end of article for the definition of a ‘best idea’).

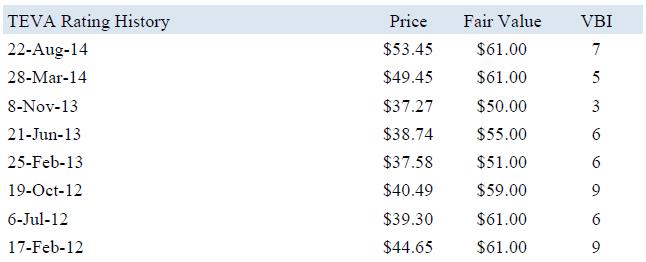

Teva Pharma registered a 9 on the Valuentum Buying Index on two separate occasions, and we think the company has become one of the best examples showcasing the resilience of high-ranking-VBI companies in the face of adversity. Not only has the company overcome recent disappointing news related to its key drug Capaxone, but it has also had to undergo changes in the executive suite, which challenged the continuity of the thesis. But in spite of all this, we were still pounding the table on shares (here, here, and here). We sent an email transaction alert to members, adding the company to the Best Ideas portfolio July 24, 2013. So far in 2014, shares of Teva are up nearly 44% versus the market’s return of 10%. That kind of performance is worth waiting for.

Teva’s third-quarter results, released October 30, have helped to propel equity price performance. During the period, cash flow from operations surged, while generic medicine profitability jumped 40% on a year-over-year basis. GAAP diluted earnings per share increased more than 20%, and the firm raised the low end of its earnings per share guidance for the year to $5-$5.10 from $4.90-$5.10 previously. Management also indicated that it will increase its share repurchase program to $3 billion, an increase of $1.7 billion to the existing program. With the company still trading below our $60+ per share fair value estimate, we’re big fans of the increased buyback. The company will remain a holding in the Best Ideas portfolio for the time being. Job well done. What is considered a ‘Best Idea’ at Valuentum? A best idea in Valuentum parlance is a holding in the Best Ideas portfolio and/or the Dividend Growth portfolio. We typically add shares to the Best Ideas portfolio when they register a high rating (a 9 or 10 = a “we’d consider buying” rating) on the Valuentum Buying Index and hold them until they register a low rating (a 1 or 2 = a “we’d consider selling” rating) on the Valuentum Buying Index. We don’t add all firms that register a high score on the Valuentum Buying Index to the actively-managed portfolios due to sector weighting or overall market valuation considerations, among others. The Valuentum Dividend Cushion is a key factor behind adding companies to the Dividend Growth portfolio and is used in conjunction with a company’s annual dividend yield, its price-to-fair value ratio and Valuentum Buying Index rating. |