Member LoginDividend CushionValue Trap

|

What Baseball Taught Investors About Stock Valuation

publication date: Oct 10, 2013

|

author/source: Brian Nelson, CFA

By Brian Nelson, CFA It was October 1, 1961 – 34 years after Babe Ruth hit 60 homeruns in one season. Yankee Stadium was half-empty on the last game of the regular season. It was the fourth inning against the Red Sox, and Boston right-handed rookie pitcher, 24-year old Tracy Stallard, thus far had held the Bombers to a goose egg. Nineteen-year-old truck driver Sal Durante watched anxiously from the right field stands.

[Roger Maris stepped to the plate. Stallard threw two pitches, hoping that the reigning American League Most Valuable Player would chase them. The bomber didn’t bite. The crowd booed, as only a long-ball would satisfy. And then it came – a waist high fastball – and Maris belted it into the hands of Durante ten rows into the right field stands. Durante would get a $5,000 award for his part in this historic event.] It must have been a beautiful thing to see live for the 23,154 souls in attendance for the final game of the Bombers' 1961 season. Billy Crystal’s 61* was a valiant effort to give to future generations the mystical story of Mantle and Maris that summer, but for those that lived it, there may never be another quite like it. McGwire's and Sosa’s homerun race in 1998 – and perhaps the best ballplayer that ever lived Barry Bonds (who not only holds the single-season homerun record but also the lifetime homerun record) – will always be plagued by allegations regarding performance-enhancing drugs (steroids). The summer of 1961 was baseball at its finest.

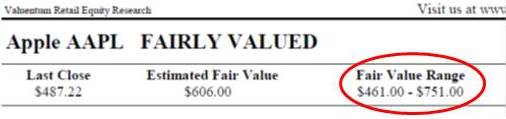

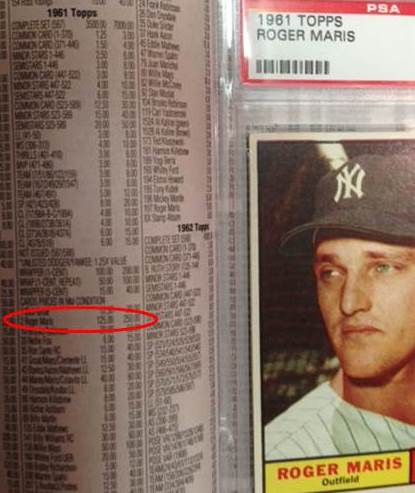

Almost everyone – boys and girls alike – has owned a card of their favorite sports hero. Some may remember attaching them with clothes pins to the frames of their bicycles (so that every turn of the wheel made a “motor” sound). It was “all-the-rage” in the 1950s and 1960s. Others stored them for safekeeping as a nostalgic token of their childhood – a time when everything seemed so innocent. Today, collectors around the world use a price guide – “a Beckett” – to discover the value of these now-coveted cards. For a graded 1961 Topps Roger Maris, the value range is $125 to $250 (as encircled in red in the picture to the right), depending on the condition of the card. You’ll notice that, in the guide, there’s no precise figure for value (it doesn’t say the card is worth exactly $200, for example), but instead the guide offers a range of probable fair values for the card’s intrinsic worth, depending on certain variables. To a large extent, the framework that youngsters use to assess the value of their baseball cards is the same framework that some of the most savvy investors use to evaluate stocks. As we outline in the ’13 Most Important Steps to Understand the Stock Market’: Value is not a precise point estimate, but a range of probable outcomes. Why? Because all of the value of a company is generated in the future (future earnings and free cash flow), and the future is inherently unpredictable (unknowable). If you or I could predict the future with absolute certainty, then we can say a company's shares are worth precisely this, or that a firm's stock is worth precisely that. But the truth is that nobody knows the future, and we can only estimate what a company's future free cash flow stream will look like. Certain factors will hurt that free cash flow stream relative to forecasts, while other factors will boost performance. That's how a downside fair value estimate and an upside fair value estimate is generated, or in the words of Warren Buffett and Benjamin Graham a "margin of safety." Within our 16-page equity research reports, we not only provide a fair value estimate for each company but also a fair value estimate range. Just like you may be interested in buying a 1961 Topps Roger Maris card at a price far below the low end of its fair value range ($125) -- or not at all if it doesn't meet other criteria -- we think stocks that are trading below the low end of their respective fair value ranges are also attractive (we consider these firms to be ‘undervalued’). Typically, firms that are undervalued and are just starting to exhibit strong technical and momentum indicators (buying interest by investors) score highly on our Valuentum Buying Index, our stock-selection methodology. Key Takeaway: Investors of all types are going to try to sell you overpriced stock everyday. It's good practice to use the fair value ranges found at the top of our 16-page equity reports as a way to separate bargains from overpriced hypes that are due for a fall. Example fair value range shown below:

Source: Valuentum's 16-page Report P.S. The Roger Maris card is not for sale. I'm saving it for my little boy. Related Companies: CLCT |

What Baseball Taught Investors About Stock Valuation

What Baseball Taught Investors About Stock Valuation