|

|

Recent Articles

-

In the News: MSFT, AAPL, SAVE, ALB

In the News: MSFT, AAPL, SAVE, ALB

Jan 17, 2024

-

Image: Microsoft and Apple have been strong performers the past several years, with Microsoft recently surpassing Apple’s market capitalization to become the largest entity in the S&P 500.

The start of trading in 2024 hasn’t been tracking the way that we like, but it’s way too early to sound the alarm on any sort of correction. The employment markets remain very healthy, both as it relates to unemployment and wage gains, while inflation looks to be largely under control, with the market expecting a number of rate cuts during 2024. We continue to like the areas of big cap tech and large cap growth in the current market environment.

-

Your Role as a Choice Architect

Your Role as a Choice Architect

Jan 15, 2024

-

Image: Impact Hub Global Network.

Richard Thaler in his groundbreaking book Nudge, co-written with Cass Sunstein, talked about the role of the choice architect. A choice architect is basically someone or some organization that has the responsibility for organizing the context and content in which people make decisions. At Valuentum, we can never provide personalized buy/sell advice, but in providing publishing services, we've opted for the healthy option for members, and that sometimes means you won't find a large selection of dessert options. This isn't a shortcoming of our service (i.e. we know desserts are tempting), but rather a key positive attribute. As we've shown time and time again, you don't need to look far to beat the market return (or, by comparison, to have a healthy diet). If something is not on the menu at Valuentum, it means the chef has something better cooking in the kitchen. Here's to your long-term financial health!

-

FedEx’s ESG Initiatives Are Refreshing Reminder of Great Companies Doing Things Right

Jan 13, 2024

-

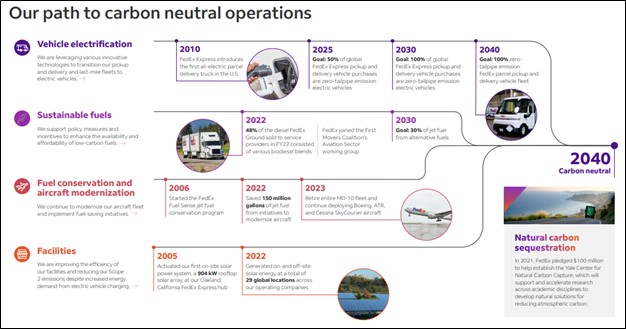

Image Source: FedEx 2023 ESG Report.

FedEx’s revenue outlook for the remainder of fiscal 2024 wasn’t great, and while the company is a key input to assessing the health of the U.S. economy, we’re not reading too much into the weakness. We find that FedEx is doing a great job with respect to its ESG initiatives across the board, and while we won’t be adding it to any newsletter portfolio at this time, the company’s efforts with respect to ESG are a refreshing reminder of the companies in our coverage universe that are doing things right.

-

UnitedHealth Group Still a Free-Cash-Flow Generating Machine

Jan 12, 2024

-

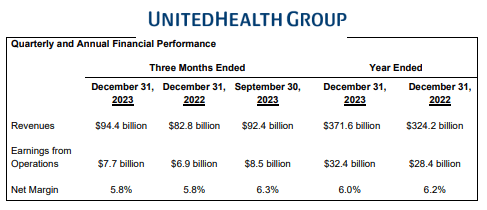

Image: UnitedHealth Group continues to drive strong revenue and operating earnings performance. Image Source: UnitedHealth Group.

On January 12, healthcare benefits provider UnitedHealth Group reported strong fourth-quarter 2023 results that showed revenue advancing 14% on a year-over-year basis thanks to strength at its UnitedHealthcare and Optum divisions, while earnings from operations advanced 11.6%. UnitedHealth is facing some temporary cost pressures in its business due to pent-up demand for discretionary procedures following the worst of the COVID-19 pandemic, but its net margin held up fine in the period, coming in at 5.8%, the same level a year ago. Management reaffirmed its previously-issued 2024 guidance, and we continue to like UnitedHealth Group as a key weighting in the Best Ideas Newsletter portfolio. Shares yield ~1.4% at the time of this writing.

|