Member LoginDividend CushionValue Trap

|

Oracle’s Strategic Shift is Starting to Bear Fruit

publication date: Mar 17, 2020

|

author/source: Callum Turcan

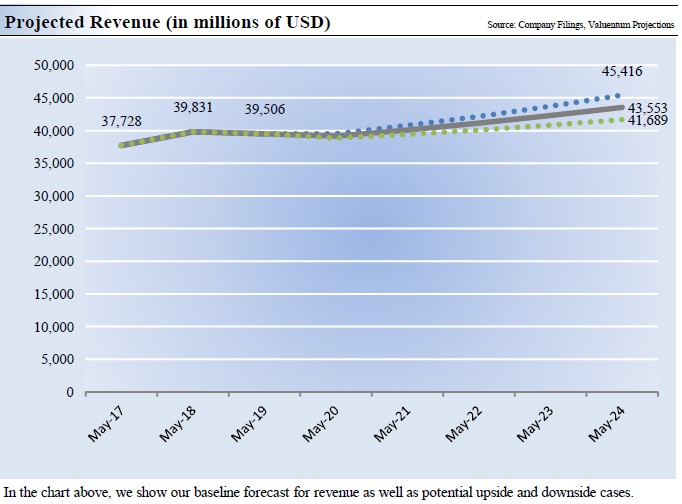

Image Source: Oracle Corporation – Third Quarter Fiscal 2020 Earnings Press Release By Callum Turcan On March 12, Dividend Growth Newsletter portfolio holding Oracle Corporation (ORCL) reported earnings for the third quarter of fiscal 2020 (period ended February 29, 2020) which handily beat consensus expectations on the both the top- and bottom-lines. Growing subscription revenues at its cloud-based businesses were key to generating this outperformance, and most importantly in our view, Oracle showcased that its outlook is improving as it shifts away from old and stale IT infrastructure offerings (i.e. enterprise data application management) and towards the IT infrastructure of the 21st Century (cloud-based services i.e. software-as-a-service and infrastructure-as-a-service). Shares of ORCL yield ~2.1% as of this writing and our fair value estimate stands at $55 per share. Financial Overview In the third quarter of fiscal 2020, Oracle’s GAAP revenues were up 2% year-over-year (3% on a constant-currency basis) due entirely to strength at its ‘cloud services and license support’ segment offsetting weakness elsewhere. The firm’s operating expenses grew by just 1% during this period (2% on a constant-currency basis), allowing for a ~65 basis point expansion in its GAAP operating margin along with 4% year-over-year growth in its GAAP operating income (that growth rate rises to 5% on a constant-currency basis). Operating expenses were contained across the board, with year-over-year reductions realized in G&A, sales and marketing, amortization of intangible assets, and restructuring costs (hardware expense reductions were likely a product of reduced hardware sales). Here’s what management had to say during Oracle’s latest quarterly conference call with investors (emphasis added): “Our Cloud Services and License Support business, basically our subscription business, which includes SaaS, IaaS and software updates, powered our revenue growth. Those subscription revenues for the quarter were $6.9 billion, up 5% and accounted for nearly 71% of total company revenues, up from 69% last year. License revenues were $1.2 billion, the same as last year… As you can see, we've replaced ecosystem revenues with subscription revenues, which will make it easier for you to see the revenue growth rate of the largest part of our business more clearly. You'll still be able to determine the growth rates for our entire software ecosystem by combining subscription and license revenues. Our cloud renewal rates continue to go up. The gross margin for Cloud Services and License Support was 86%, up 1% from last quarter. Both SaaS and IaaS gross margins were up more than 1% from both last quarter and last year. As we continue to get to scale, I expect our cloud gross margins will increase further, driving an acceleration in our gross profit growth.” --- Safra Catz, CEO of Oracle At the end of February 2020, Oracle carried $23.8 billion in cash and cash equivalents and $2.0 billion in marketable securities. That was stacked up against $2.4 billion in short-term debt and $49.3 billion in long-term debt. Please note Oracle’s cash-like balances have been drawn down considerably over the past few quarters to fund enormous share repurchases. During the first three quarters of fiscal 2020, Oracle generated $9.5 billion in net operating cash flows and spent $1.1 billion on capital expenditures, allowing for $8.4 billion in free cash flows. We would like to stress that we view Oracle’s sizable net debt position as quite manageable, as things stand today, given its quality free cash flow profile and still significant cash-like balance. The firm spent $2.3 billion covering its dividend obligations during the first three quarters of fiscal 2020, and another $13.9 billion repurchasing its shares. Oracle’s diluted outstanding common share count fell by over 12% year-over-year in the third quarter of fiscal 2020. Management expects Oracle will spend around $2.0 billion in fiscal 2020 on capital expenditures, up from $1.7 billion in fiscal 2019. Guidance for the Fourth Quarter Oracle’s management noted that due to the ongoing novel coronavirus (‘COVID-19’) pandemic that the firm would have to give a wider range than normal as it relates to its expectations for the fourth quarter of fiscal 2020. Total revenue growth is expected to come in at -2% (negative 2%) to positive 2% on what appears to be a year-over-year basis (based on management commentary before covering guidance). As it relates to Oracle’s subscription revenues, which as mentioned previously, have been a strong point of late, management forecasts those sales will grow by 3%-5% year-over-year in the fourth quarter of fiscal 2020. Non-GAAP adjusted diluted EPS is expected to grow by 3%-9% year-over-year during this period, a product of substantial share buybacks. Looking ahead, management communicated that as Oracle’s subscription-based revenues become an ever-larger part of the business (those sales represented 71% of Oracle’s revenues in the third quarter of fiscal 2020), that will help accelerate company-wide growth. It won’t be until June that Oracle provides a more concrete outlook for fiscal 2021, however, we appreciate that management is indicating the firm’s outlook is improving. That’s likely why shares of ORCL have performed relatively well of late. How This Fits in With Our DCF Valuation Companies are evaluated on the basis of their expected future performance, and by communicating that revenue growth will increase (to some degree) next fiscal year and potentially beyond due to rising recurring subscription-based sales (primarily from its cloud-based businesses), that gives us confidence in our discounted cash flow valuation covering Oracle. As depicted in the upcoming graphic down below, we forecast modest revenue growth for Oracle over the coming fiscal years. This is under our “base case” scenario, and please note there’s room for upside and downside to these forecasts depending on how well Oracle can perform in the cloud-based arena.

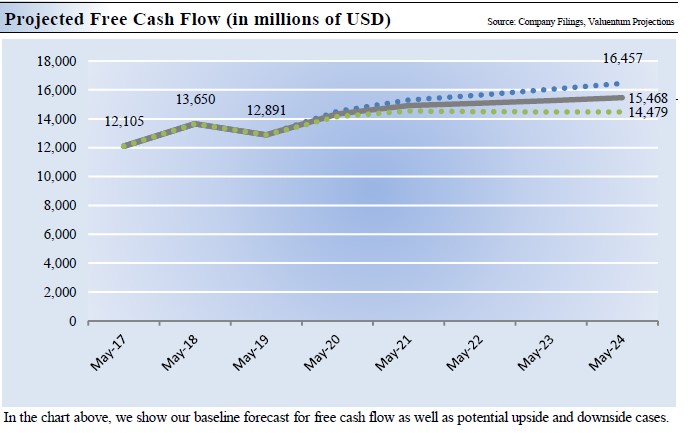

Image Shown: Our base case scenario forecasts modest revenue growth at Oracle over the coming fiscal years. Top-line growth combined with controlled operating expenses, relatively low capital expenditure requirements, and the potential for gross margin expansion at its cloud-based businesses (as management alluded to during Oracle’s quarterly conference call) allows for Oracle to carry a quality cash flow profile. We model modest free cash flow growth over the coming years, which would be made more obtainable if management’s guidance for Oracle to see an acceleration in its sales growth next fiscal year materializes.

Image Shown: Our base case scenario forecasts that Oracle will generate modest free cash flow growth over the coming fiscal years, aided by rising revenues. Concluding Thoughts We continue to like Oracle in our Dividend Growth Newsletter portfolio and view the firm as well-positioned to ride out the ongoing storm. When Oracle provides an update on its expectations for fiscal 2021, we will provide our members with any relevant updates. COVID-19 is putting a tremendous amount of pressure on global equity prices, but when the dust settles, Oracle’s improving outlook and sound financials could make the firm stand out. Software Industry – ADBE ADSK EBIX INTU MSFT ORCL CRM Related: AMZN, GOOG, GOOGL ----- Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free. Callum Turcan does not own shares in any of the securities mentioned above. Oracle Corporation (ORCL) is included in Valuentum’s simulated Dividend Growth Newsletter portfolio. Alphabet Inc (GOOG) Class C shares are included in Valuentum’s simulated Best Ideas Newsletter portfolio. Some of the other companies written about in this article may be included in Valuentum's simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies. |

0 Comments Posted Leave a comment