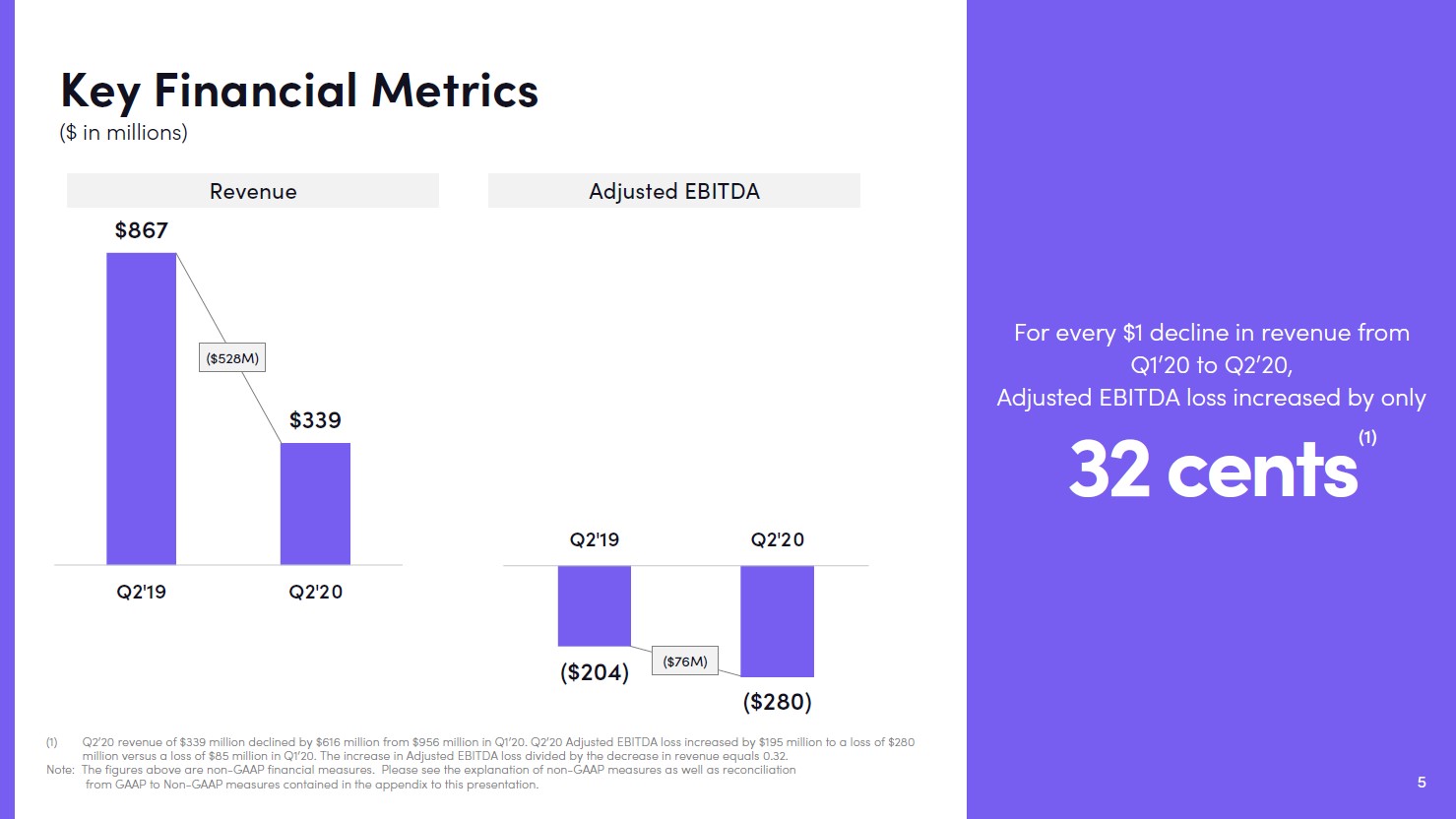

Image Shown: Lyft Inc’s business model is not well suited for the pandemic. Its financial performance was decimated during the second quarter of 2020 as its active rider base opted to stay home or use other methods of transportation. Image Source: Lyft Inc – Second Quarter of 2020 Supplemental Data

By Callum Turcan

On August 12, the ridesharing company Lyft Inc (LYFT) announced second quarter 2020 earnings that beat consensus bottom-line estimates but missed consensus top-line estimates. The ongoing coronavirus (‘COVID-19’) pandemic has posed a major headwind for Lyft due to workers commuting less, reduced demand from late-night bar patrons, and other factors. Management did note within Lyft’s earnings release that rideshares were up 78% in the month of July 2020 versus April 2020 levels, indicating a recovery is underway, though the firm has a long way to go before getting back to pre-pandemic levels of revenue.

Earnings Update, Still No Earnings

During the second quarter, Lyft’s GAAP revenues were down 61% year-over-year, hitting $0.3 billion, as the number of rides taken on its service plummeted. While Lyft’s GAAP operating loss narrowed to $0.5 billion last quarter (versus a $0.7 billion operating loss in the same period last year) due to the sharp reduction in its operating expenses, the company remains a long way off from being profitable. Lyft posted a GAAP net loss of $0.4 billion last quarter.

In late-April, Bloomberg reported Lyft was cutting ~17% of its corporate workforce and ending its scooter business in some US cities to reduce its cash burn in the face of the pandemic. Not including restricted cash, cash equivalents or restricted investments on hand (totaled $1.2 billion at the end of June 2020), Lyft had $2.8 billion in cash, cash equivalents, and short-term investments on hand at the end of June 2020. During the first half of 2020, Lyft generated negative $1.0 billion in free cash flow as its net operating cash flows remained negative.

Lyft has enough cash and cash-like holdings on hand to cover its cash burn for now, but should the pandemic continue to reduce ridesharing activities (particularly in the US) for an extended period of time, eventually the firm will need to tap capital markets again (potentially at a very unfavorable time). Please note Lyft had a bit over $0.6 billion in total debt outstanding at the end of June 2020, all of which was long-term, after issuing $0.65 billion in 1.500% Convertible Senior Notes due 2025 last quarter.

Business Model Not Easily Scalable

Cost cutting measures are required to buy Lyft more time to ride out the pandemic, but more needs to be done than that. Even before the pandemic, Lyft never showcased or fully communicated how it would be able to become consistently profitable (though management put out targets to achieve positive non-GAAP adjusted EBITDA, we view adjusted non-GAAP metrics as fishy and malleable). For every incremental dollar of revenue, Lyft incurs meaningful incremental operating expenses, meaning its business is not that scalable. From 2017 to 2019, Lyft’s annual GAAP operating loss grew every year (its 2019 GAAP operating loss was quite large due to stock-based compensation expenses in light of its initial public offering). Back in April 2019 (link here), we published a piece on our website that noted:

Reminiscences of the dot-com boom came back to the markets with the over-hyped initial public offering of Lyft, a stock that continues to get shellacked as its first days as a publicly-traded enterprise. Those that know Valuentum know that we wouldn’t touch such investments with a 10-foot pole. The company lost $43 per share in 2018.

Since then, Lyft shares have fallen by ~59% as of this writing while the S&P 500 index (SPY) is up ~17% (before taking dividend considerations into account, which would see the outperformance of the S&P 500 grow over Lyft as the firm does not pay out a common dividend at this time). Instead of focusing on revenue per active rider, number of active riders, or other operational metrics, we focused on Lyft’s outlook and the trajectory of its free cash flows (which was and continues to be abysmal). During Lyft’s latest earnings call, management noted that (emphasis added):

“…[W]e’re executing on our previously announced cost reduction plans, as well as projects to improve our unit economics. We now expect we can achieve adjusted EBITDA profitability with 20% to 25% fewer rides, than what was assumed when we initially disclosed, this target last year.

While we can’t perfectly predict the timing of recovery, based on the reduced ride levels required for us to break even, as well as what we’ve observed in terms of the recovery to-date, we believe that there are multiple scenarios and levers that should allow us to hit this milestone, by the fourth quarter of 2021.” Logan Green, co-founder and CEO of Lyft

We will have to see if Lyft can eventually hit this moving target, though we prefer the firm focus more so on free cash flow (net operating cash flow less capital expenditures). Uber Technologies Inc (UBER) reported second quarter 2020 earnings on August 6, and its ride sharing business was also facing an immense amount of stress due to COVID-19. However, Uber Eats offered the firm some reprieve as households turned to the meal ordering app to stay at home. Lyft did not have the same benefit as it is not in the restaurant order/delivery business.

Operations Update

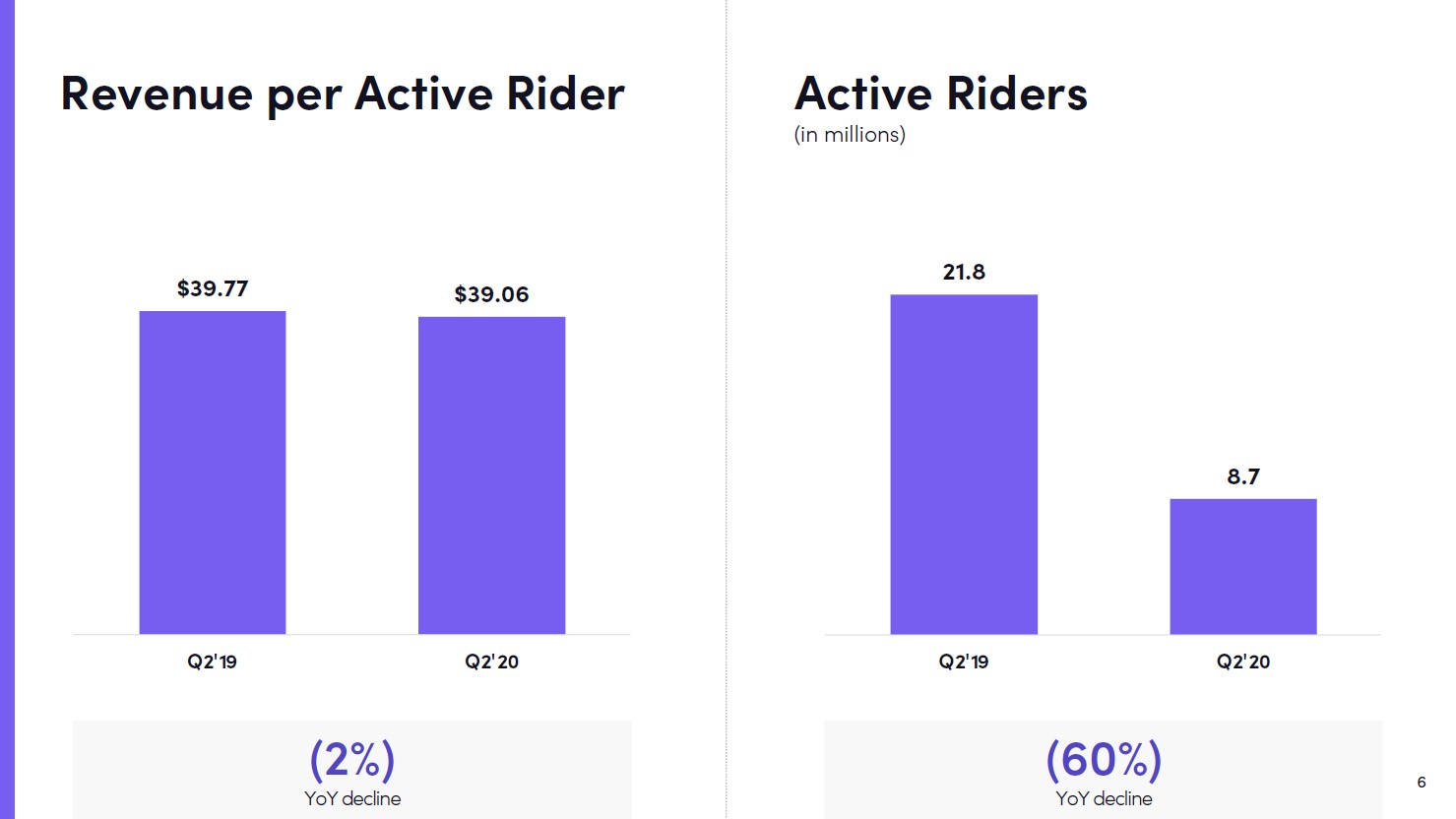

As you can see in the upcoming graphic down below, Lyft reported that its active riders base plummeted in the second quarter of 2020 versus the same period a year-ago, though its revenue per active rider was only down marginally during this period. Should active riders return, Lyft’s outlook would improve considerably (assuming huge promotions are not required to get active riders to return) though in one of Lyft’s big markets, California, various pandemic containment efforts remain in effect.

Image Shown: Lyft’s active riders base stayed home or used other forms of transportation last quarter as the pandemic took its toll. Image Source: Lyft – Second Quarter of 2020 Supplemental Data

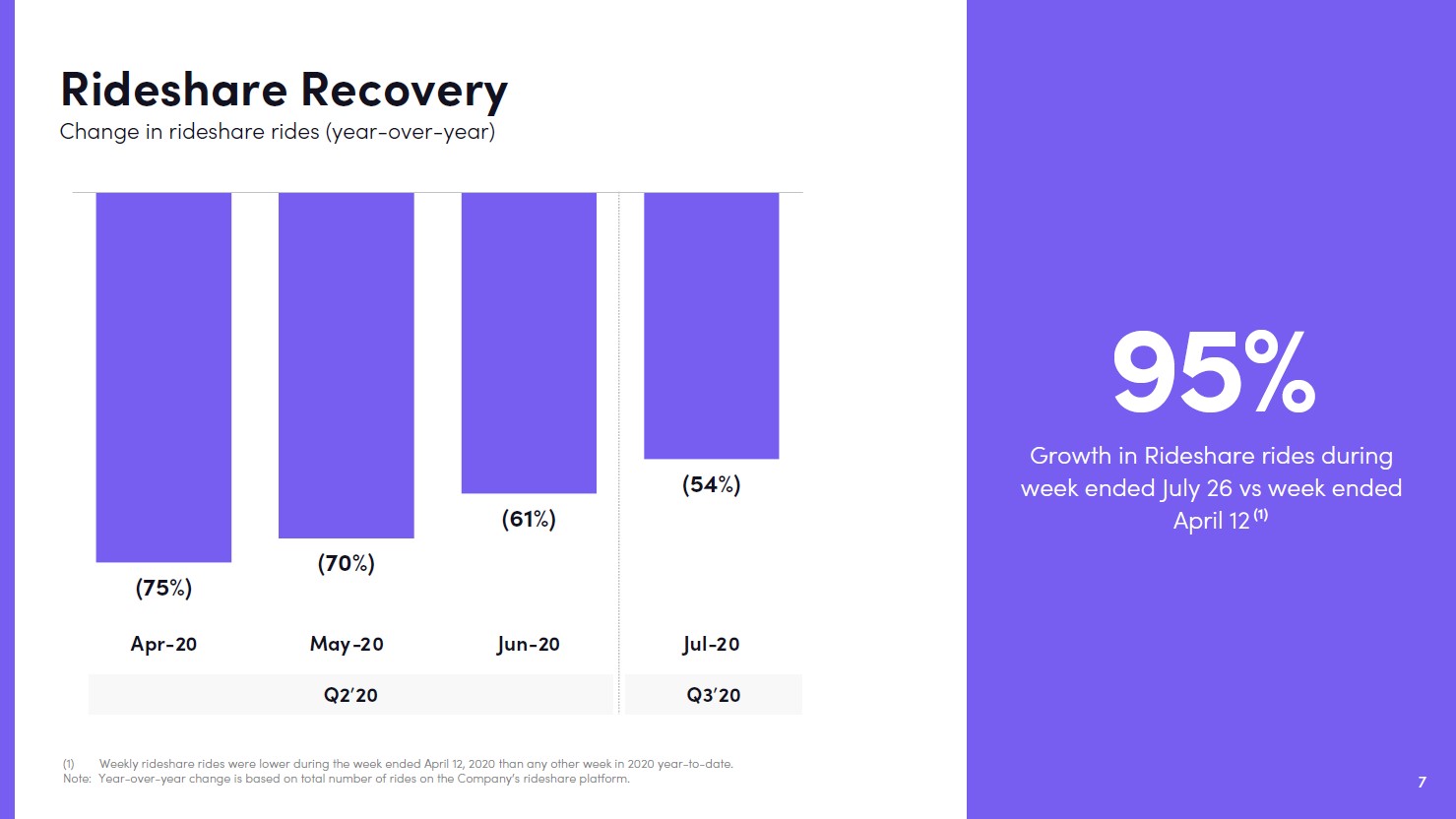

Lyft also provided an update on the recovery in ridesharing services as you can see in the upcoming graphic down below, though even in the month of July 2020, Lyft’s business was still down considerably year-over-year.

Image Shown: Riding services are recovering, particularly in the US, though off an extremely low base. Image Source: Lyft – Second Quarter of 2020 Supplemental Data

Concluding Thoughts

We are still not interested in Lyft, and we generally prefer the companies included as holdings in the Best Ideas Newsletter portfolio (link here) when it comes to finding investments with solid capital appreciation upside (along with income generation upside, depending on the firm). Lyft still needs to prove that its business is scalable, and the pandemic has stymied those efforts immensely. Even if Lyft reaches “profitability” on a non-GAAP adjusted EBITDA basis at the end of next year, the firm will likely still be a way off from generating positive free cash flows on a consistent basis.

—–

Related: LYFT, UBER, QQQ, SPY, AWAY, IPO, IBUY, GIGE, XTN

—–

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Callum Turcan does not own shares in any of the securities mentioned above. Some of the companies written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.