Member LoginDividend CushionValue Trap

|

JPMorgan Reports Second Quarter, Notes Peculiar Times

publication date: Jul 15, 2020

|

author/source: Matthew Warren

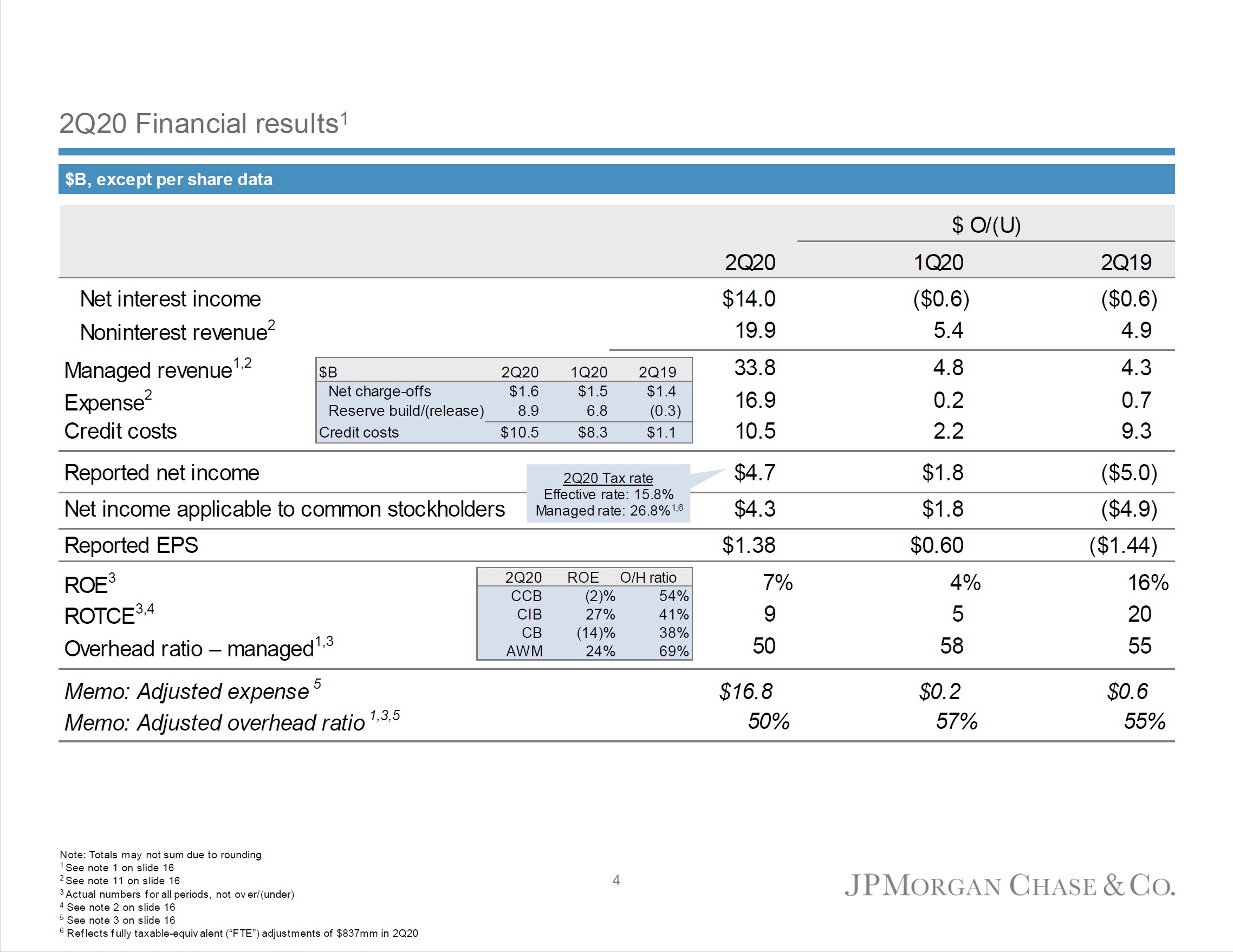

Image Shown: Overview of JPMorgan’s 2Q2020 earnings. Image Source: JPMorgan 2Q2020 Earnings Presentation There was a fair amount of discussion on JPMorgan’s conference call about how the company (and the rest of the banking industry) are taking large provisions now for charge offs that they expect to come in the future. The future and the timing and magnitude of the eventual write-offs are quite murky indeed, which helps explain the volatility of banking shares in general, and especially for those institutions that might fall over in an “adverse scenario.” JPMorgan is not one of those banks that is at risk. It stands on high ground in the industry thanks to its scale, diversification (a huge benefit this quarter), high quality management, and outsize earnings power as compared to many of its peers. By Matthew Warren JPMorgan Chase & Co. (JPM) reported very impressive second-quarter results July 14, considering the backdrop of the COVID-19-caused economic downturn, beating analyst consensus estimates on both the top and bottom lines. As one can see in the graphic above, managed revenue was actually up quite substantially thanks to dramatic gains in investment banking and markets activities. Net income (available to common stockholders) was of course down from last year to $4.3 billion due to a massive reserve build of $8.9 billion in the quarter. Essentially what management indicated in the conference call was that they are weighing the downside scenarios quite heavily as compared to their base case. So, if the base case indeed comes to fruition, there would be room for release of some amount of allowance for loan losses. While we would all hope a more-benign scenario plays out, JPMorgan management is actually preparing for the worst, and indicated that the board would even review cutting the dividend if the “adverse scenario” comes to fruition.

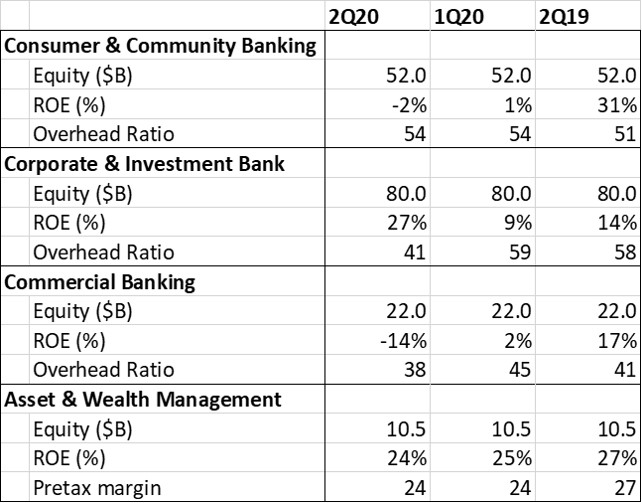

Image Shown: JPMorgan Key Metrics across segments. Image Source: Analyst collection of data from 2Q2020 Earnings Presentation

Digging into the business segments in the graphic above, one can see that the usual crown jewel of ‘Consumer & Community Banking’ is under substantial pressure due to the aforementioned reserve builds—mostly against the credit card book. The savior in the quarter was the ‘Corporate & Investment Bank,’ which put up a stunning 27% return on equity in the period—closer to what you might normally see from the consumer bank. Management was quick to point out that this was due to outsized capital raising (both common, converts, and debt offerings) amongst the client base and outsize trading volumes and margins given the many dislocations in the market during the quarter. The executive suite guided for both of these revenue streams to normalize lower in the coming quarter, though these lines are notoriously hard to predict. The ‘Commercial Banking’ segment was the worst of the group and highlights why the long tail of thousands of US banks that focus on these activities are generally sub-par investments—with a very few notable exceptions. The ‘Asset & Wealth Management’ segment continued to shine with a mid-twenties return on equity capital. It’s too bad that, despite being one of the largest asset managers in the world, it nearly gets lost in this enormous entity. Just to round out our commentary on JPMorgan’s earnings, we thought we would highlight the below commentary from company CEO Jamie Dimon, in order to flesh out the strange nature of this macro-economic downturn: “…just to amplify, in the normal recession, unemployment goes up, delinquencies go up, charges go up, home prices go down. None of that's true here. Incomes go down, savings go down. Savings are up, incomes are up, home prices are up. So, you will see the effect of this recession. You're not going to see it right away because of all the stimulus and the fact, 60% or 70% of the unemployed are making more money than they were making when they were working. So, it’s just very peculiar times.” There was a fair amount of discussion on JPMorgan’s conference call about how the company (and the rest of the banking industry) are taking large provisions now for charge offs that they expect to come in the future. The future and the timing and magnitude of the eventual write-offs are quite murky indeed, which helps explain the volatility of banking shares in general, and especially for those institutions that might fall over in an “adverse scenario.” JPMorgan is not one of those banks that is at risk. It stands on high ground in the industry thanks to its scale, diversification (a huge benefit this quarter), high quality management, and outsize earnings power as compared to many of its peers. --- Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free. Matthew Warren does not own any of the securities mentioned. Some of the other securities written about in this article may be included in Valuentum's simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies. |

0 Comments Posted Leave a comment