Image Source: Johnson & Johnson Fourth Quarter Earnings Presentation

Shares of Johnson & Johnson have performed well since being added to both the simulated Best Ideas Newsletter portfolio and simulated Dividend Growth Newsletter portfolio. We continue to be impressed with the depth of the clinical pipeline as Johnson & Johnson has an appealing mixture of mature and early-stage products that power the portfolio. Let’s examine the three main franchises of the portfolio to gain a better understanding of the depth of Johnson & Johnson’s Pharmaceutical division.

By Alexander J. Poulos

Immunology

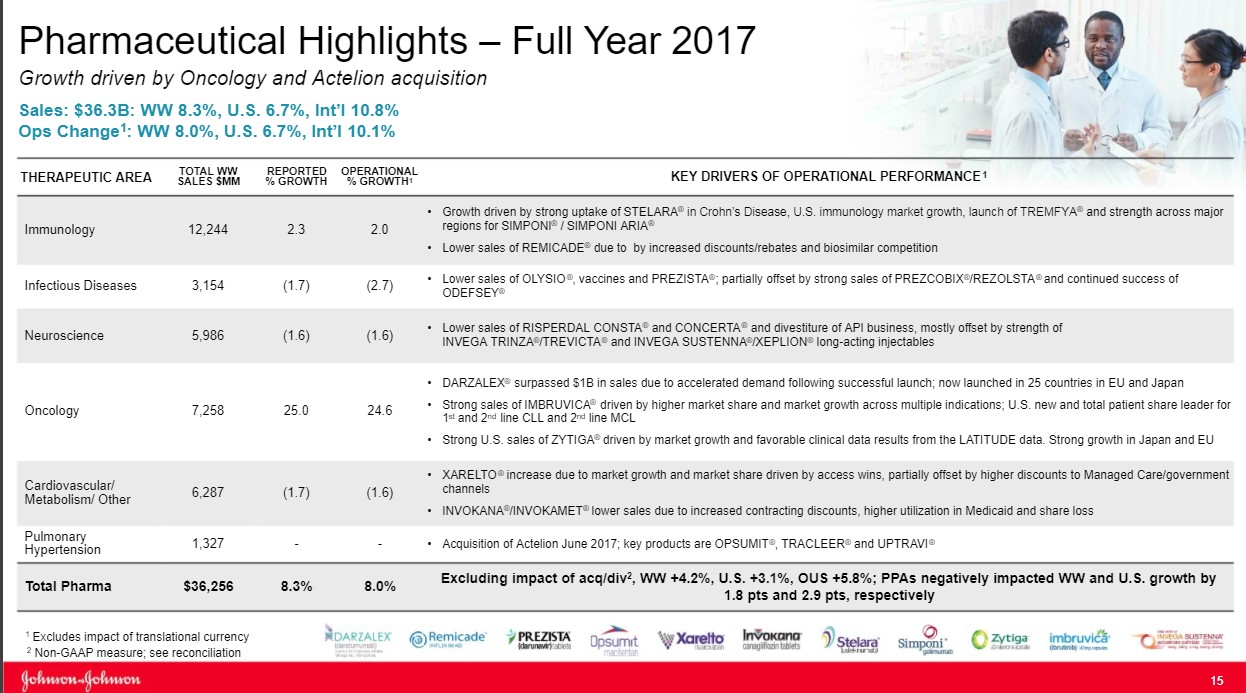

The Immunology Division remains the engine that drives performance at Johnson & Johnson (JNJ) as the group accounts for nearly one third of total sales. The division reported operational sales growth of 2%, which masks the challenges the group is facing.

The star of the show remains Remicade as the product posted sales of $6.3 billion for 2017, a tidy sum. Remicade accounts for over half of the Immunology group’s overall revenue. Under optimal conditions, Remicade would serve as a free cash flow powerhouse as minimal expenses would be needed to market the product as prescribers are well aware of its clinical profile. The challenge facing Johnson & Johnson is that the product has now lost its patent protection as biosimilar competitors have entered the market with Pfizer’s biosimilar the most notable example.

Johnson & Johnson and Pfizer are locked in a courtroom battle over the appropriate time for a biosimilar entry, but we feel this is an attempt to prolong the inevitable as the product has reached the end of its respective life cycle. Going forward, we expect Remicade to transition from a source of growth to a drag on revenues. We applaud Johnson & Johnson’s management team for going out into the marketplace and acquiring Actelion and its Pulmonary Hypertension division mitigate the loss of revenue in Remicade.

Stelara is the second main asset in the Immunology division. The product has recently won approval for use in Crohn’s disease, which is driving revenue growth for the time being. While a positive in the short run we feel the wave of new entrants, most notable the Jak-1 inhibitor class with its oral dosage formulation, will disrupt sales growth of older treatments such as Stelara going forward.

The same outlook holds for Simponi (rheumatoid arthritis and psoriatic arthritis are the predominant uses) as newer entrants, most notably the interleukin class thus far, possess a cleaner side-effect profile while boasting near equivalent or in some cases superior clinical outcomes. We are by no means disparaging the product class of Johnson & Johnson. We are merely attempting to point out we see the product class as challenged going forward, as the class is now overcrowded (which we expect payers to leverage to its advantage by driving down costs via favorable formulary placement). We think Johnson & Johnson’s future is in other product classes, with Immunology serving as a source of free cash but a potential drag on revenue growth as it cycles through the loss of patent exclusivity on Remicade.

Oncology

We view the oncology division as the most important division for Johnson & Johnson going forward as an appealing mixture of assets in various stages of their respective life cycles and should power growth well into the rest of the decade. That said, Johnson & Johnson is facing some near-term pressure as patent protection expected to lapse on Velcade, a treatment for multiple myeloma ($1.1 billion in sales for 2017) and Zytiga a treatment for prostate cancer ($2.5 billion in 2017).

Johnson & Johnson is locked in a protracted legal battle in an attempt to stave off generic competition for Zytiga. We feel the odds do not favor Johnson & Johnson and a generic may enter the marketplace shortly. Johnson & Johnson, in a clever bit of lifecycle management, has won approval for Erleada (apalutamide) for the niche treatment of non-metastatic, castration-resistant prostate cancer, a nice win but in our view not adequate to ensure the survivability of the overall prostate cancer franchise.

The real growth molecules remain Imbruvica (treatment of various lymphomas) and Darzalex (multiple myeloma) as both molecules are firmly in the early stages of their respective growth trajectories. Imbruvica posted total sales in 2016 of $1.25 billion, cementing its blockbuster status. Imbruvica followed up in 2017 with overall sales of $1.89 billion as the treatment continues to gain favor with healthcare providers. We remain confident growth will continue for the foreseeable future as the competitive landscape remains devoid of a competitive threat for now.

The investment landscape for Darzalex neatly mirrors the path of Imbruvica as sales have jumped from $572 million in 2016 to its current perch of $1.2 billion in 2017. While the treatment paradigm in multiple myeloma is far more crowded, the very favorable overall survival profile augurs well for continued growth of this franchise. We feel the continued growth of Imbruvica and Darzalex will more-than-offset the loss of patent protection from Zytiga and Velcade.

Cardiovascular

We remain somewhat pessimistic on Johnson & Johnson’ Cardiovascular group, in aggregate, as a combination of the loss of patent protection on drugs coupled with recent regulatory decisions may have irrevocably altered the growth trajectory of the division.

Let’s break down our review of the group into three key drugs as they account for the lion share of the overall revenue generated by the franchise. The first is Procrit, a longstanding injectable treatment for anemia. The product has lost patent protection with numerous biosimilars now having entered into the marketplace. To illustrate the irrevocable decline of the fortunes of this treatment, the largest dialysis provider in the world, Fresenius, has switched to a generic version of Epoetin Alpha, the active ingredient in Procrit. The product was originally intended for those with chronic kidney conditions such as those on dialysis. With Fresenius switching to a biosimilar, in our view, signals the death knell for the branded product.

With respect to Invokana, a subtype 2 sodium-glucose transport (SGLT2) inhibitor for the treatment of diabetes, the revenue growth outlook has darkened considerably in 2017. Invokana suffered the double whammy of a label change, which we feel will forever alter its growth trajectory:

Amputations. INVOKANA® may increase your risk of lower-limb amputations. Amputations mainly involve removal of the toe or part of the foot; however, amputations involving the leg, below and above the knee, have also occurred. Some people had more than one amputation, some on both sides of the body. You may be at a higher risk of lower-limb amputation if you: have a history of amputation, have heart disease or are at risk for heart disease, have had blocked or narrowed blood vessels (usually in leg), have damage to the nerves (neuropathy) in the leg, or have had diabetic foot ulcers or sores. Call your doctor right away if you have new pain or tenderness, any sores, ulcers, or infections in your leg or foot. Your doctor may decide to stop your INVOKANA® for a while if you have any of these signs or symptoms. Talk to your doctor about proper foot care

Quote Source: Invokana prescribing label

While we acknowledge Invokana has first-mover advantage, the label change is an impediment, which has opened a clear path for a competing product to emerge and capture the market. That competitor for the immediate future is Jardiance, as the product posted superior outcomes data, which in our view cements its viability and severely limits Invokana. We have begun to witness the decline since the second quarter as sales have softened Interestingly, the field may become disrupted further by Novartis (NVS) as it has an SLT1&2 inhibitor that has shown a weight loss of 15-20% in one year of treatment. Weight loss of this magnitude, if sustained, and coupled with a clean side-effect profile, in our view, would dominate the field. We’ll continue to monitor the path forward to see if this promising molecule will make its way to market.

Rounding out the roster in the Cardiovascular franchise is Xarelto—what we would term a new age blood thinner for the treatment of atrial fibrillation and various forms of blood clots. The product’s economics remain in a favorable uptrend, but we can’t help but point out that a competing product with an inferior dosing regime has captured a larger overall percentage of the market. Johnson & Johnson is hoping additional trials will expand the overall base of eligible patients. However, we can’t help but point out the combination of Pfizer (PFE) and Bristol-Myers (BMY) should not have stolen share in the manner in which it has transpired, as the duo was third-to-market with a twice-a-day dosing regimen versus daily for Xarelto. We can’t help but point out this is a missed opportunity in our book.

Conclusion

We remain constructive on Johnson & Johnson as we view the company as one of the best in class with a stellar credit profile backed with significant firepower in the form of on-hand cash and borrowing capacity. We would not be at all surprised if Johnson & Johnson re-entered the marketplace and acquired another company akin to the Actelion purchase. Our fair value estimate remains $130 per share, in line with where shares are trading at the time of this writing, but the high end of the fair value range implies a value north of $150. We remain comfortable continuing to include the idea in the simulated newsletter portfolios as the dividend rate remains very attractive.

Related: XLV, IBB

—–

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Independent healthcare and biotech contributor Alexander J. Poulos is long Johnson & Johnson. Some of the companies written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.