Shares of former Best Ideas Newsletter portfolio idea Teva Pharmaceuticals have come under renewed selling pressure after reporting weak quarterly results due largely to deflationary price pressures felt in the generic drug division. Teva has been relatively powerless in stopping the trend. We had removed the shares from the Best Ideas Newsletter portfolio well before the last leg down, and the Dividend Cushion ratio warned of tremendous risk to the sustainability of the dividend far in advance.

By Alexander J. Poulos and Kris Rosemann

Generic Drug Deflation

Teva Pharmaceuticals (TEVA) maintains its position as one of the world’s largest manufacturer of generic medications, but the marketplace for a generic drug differs from the market dynamics of the branded space. We view the generic industry as an increasingly commoditized business. The generic drug industry enjoyed a favorable tailwind of increased demand in recent years from additional customers via the Affordable Care Act, and the increase in end user demand emboldened the main competitors in the field to embark on a wave of consolidation, which culled the field of competitors and paved the way for significant price hikes. Also, the FDA has made it a priority to clear the backlog of generic new drug applications (NDA) in an attempt to lower overall costs and increase competition, which will only accentuate the downward pressure on prices.

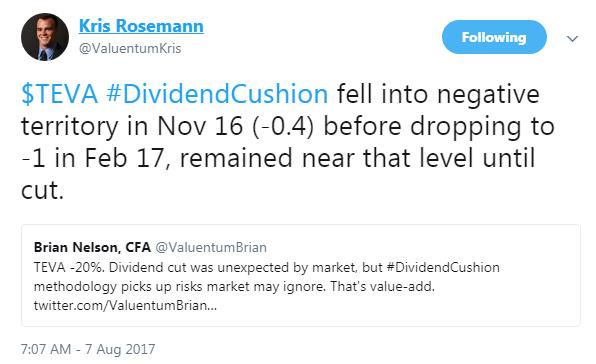

Teva, along with other generic drug makers, has come under fire for its pricing practices, with the most recent plot twist coming in the form of a lawsuit from a New York City-based hedge fund Och Ziff Capital Management. The lawsuit accused Teva and certain former executives of purposefully misleading investors regarding the strength of its business. Questions regarding the legality of its business practices that helped drive generic drug prices higher in recent years are the crux of the lawsuit, and we can’t help but feel misled to a degree as well as management’s huge bet on its ability to sustain past performance in the generic drug space via the Actavis acquisition has proven to be a bust. Though we removed Teva’s shares from the Best Ideas Newsletter portfolio well before the last leg down, “Spring Cleaning…,” and we successfully warned about the potential for a dividend cut in advance–its Dividend Cushion ratio fell into negative territory November 2016–we’re nontheless extremely disappointed. The company has also been on the ‘Dividend Yields to Consider Avoiding’ list in the Dividend Growth Newsletter for each of the past two months, so the cut should not be a surprise to members. Our original thesis on the generics space, which admittedly was off the mark, has been modified as follows.

Quarterly Sales

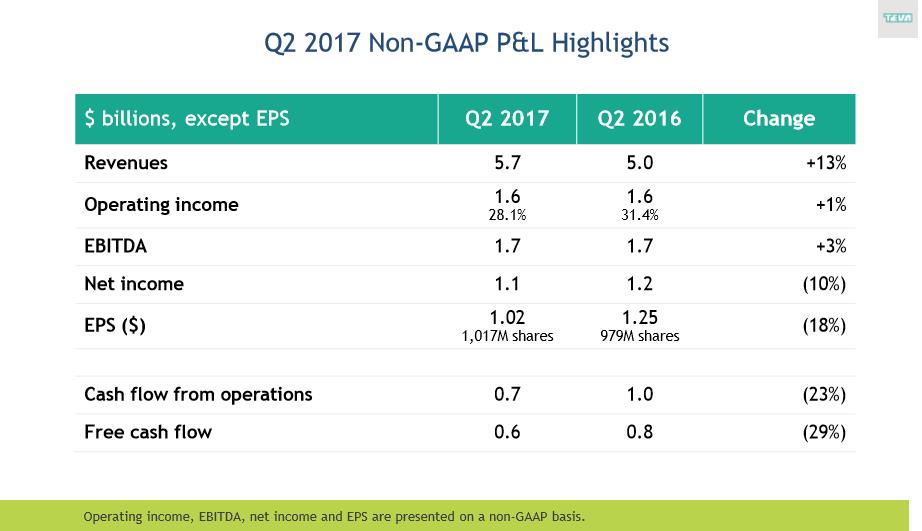

Image Source: Teva Q2 Results

Teva managed to grow its top line in the second quarter of 2017, results released August 3, thanks in large part to the recently completed acquisition of Actavis from Allergan (AGN). The Actavis acquisition was expected to fuel sales growth while projected cost synergies would allow for a boosting of EBITDA margins, but it is now our opinion that the deal for Actavis has been an unmitigated disaster. The changing competitive landscape has directly led to a decrease in margins–a radically different outcome than what was expected when the deal closed in August 2016.

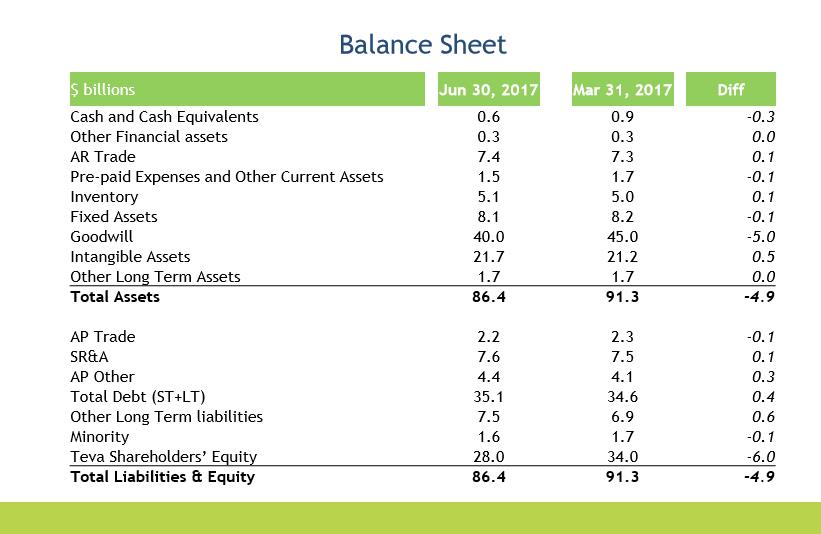

To consummate the deal, Teva agreed to pay $33.43 billion along with issuing an additional 100 million shares of Teva equity. The issuance of equity dilutes current shareholders, and the cash consideration caused its debt load to balloon to over $35 billion, placing an enormous strain on Teva’s balance sheet. In our view, to make this deal work, Teva will need to immediately utilize the expected increase in free cash flow to pay down debt as its net debt-to-EBITDA ratio was 4.56x as of the end of the second quarter of 2017. Unfortunately, the reverse has happened with free cash flow decreasing due to industry pricing dynamics.

In an effort to augment industry buying power, the largest overall purchasers of generic drugs have entered into exclusive purchasing co-ops with the drug wholesalers. The cooperatives have managed to push down drug costs by concentrating buying power, which is a boon to the largest pharmacy operators such as CVS Health (CVS), Walgreens (WBA) and Wal-Mart (WMT). The consolidation trend in the pharmacy industry does not bode well for Teva as an increasing share of buying power is being concentrated into a few well-capitalized hands. We view the consolidation in the pharmacy space as a long-term headwind for Teva–the company is likely to remain at the mercy of the buying co-ops.

Differentiating the Product Line-up

We feel the optimal scenario for Teva is a pivot to harder-to-produce generics with less competition as the pricing dynamics in areas such as inhalers offer a more stable margin profile with lower risk of price competition. The oral dosage forms of most generic medications such as tablets are rife with margin destructive pricing competition. The most profitable segment of the generic industry is the six-month window of exclusivity granted to the generic manufacturer who files the first approved NDA of a branded product.

The industry enjoyed a very favorable tailwind over the past few years based on numerous popular branded products losing patent protection, but the next few years appear relatively bare outside of the expected patent loss of GlaxoSmithKline’s (GSK) Advair inhaler. A first-to-market generic version of Advair would be helpful for Teva, but we expect the deflationary headwinds to persist well into 2018. The management team pegged drug price deflation at a high-single-digit clip for the remainder of 2017–we feel the number may prove to be a tad optimistic.

Foray into Branded Products

In our opinion, Teva’s brightest future will come via innovation—not in the heavily commoditized generic drug sector. Unfortunately, the company’s former management team has made a strategic blunder in increasing the company’s reliance on generics right when the winds of deflation are wreaking havoc on the balance sheet. To compound matters further, Teva is facing a pending biosimilar challenge to its best selling patent protected product Copaxone. Copaxone is a long-standing treatment for Multiple Sclerosis, and its success has fueled Teva’s bottom line for the past few years.

Teva is now faced with the unenviable task of replacing the revenue loss from the high-margin Copaxone as the patent protecting the IP estate has lapsed. The impact of a biosimilar has not affected the firm’s financials yet–management mentioned the impact of a competitor would reduce earnings by 20 to 25 cents for the quarter upon entry into the market. The exact timing of such a threat is not of importance, but rather the longer term trend, in our view. Sales of Copaxone have fared surprisingly well since losing exclusivity in 2015, but additional top-line and margin pressures should be expected as a result of increased competition in coming quarters.

After considering the current dynamics in the generic drug market, for Teva to successfully grow margins and revenue, additional funds will need to be devoted to bringing forth novel treatments for various disease states. Though Teva in recent years has made expansion of its specialty drug division a focus with new products expected to gain marketing approval, we remain relatively unimpressed with the branded product lineup. At this time, we are not confident adequate resources will be devoted to supporting innovative research. The pivotal decision to purchase Actavis would have been far better served if the funds were used to purchase innovative research entities or to partner with mid-stage biotech to market the products, in our opinion.

Executive Turmoil

Teva is actively searching for a new CEO to the right the ship, and the management team led by an interim CEO, was forced with the difficult decision-making to reduce the dividend by 75%. The Dividend Cushion ratio flexed its efficacy once again as the company’s Dividend Cushion ratio has been in negative territory since November 2016, and it fell to -1.1 (negative 1.1) in February of this year and remained near that level up until management’s decision to slash the payout.

The management team laid out a plausible scenario during its second-quarter conference call where Teva’s debt-to-equity ratio may exceed its debt covenants, and the persistent drug deflation coupled with the unknown entrant of a generic competitor for Copaxone has raised this possibility. It is our opinion that Teva needs to reduce costs aggressively and pay down some of its enormous debt load to give the new CEO ample opportunity to enact a turnaround.

To say the least, the earnings report was met with resounding thumbs down from Wall Street as the equity sold off over 20%. Though the low cost of generic medicines originally sounded appealing, we became increasingly wary of the industry dynamics which led to our decision to sell our position in Teva in May 2017. In hindsight, we should have removed our position after it took on a mountain of debt to finance the Actavis acquisition, and the ensuing breakdown has been a learning experience for the Valuentum team.

Future of the Generic Drug Industry

In our view, the most disturbing portion of the earnings release is Teva’s commentary on the outlook for 2018 as the deflationary spiral shows no signs of letting up. Michael McClellan, Teva Pharmaceutical Industries Limited – Senior VP & Interim CFO on the recent call stated:

All of this led management to revisit its long-term forecast for the U.S. Generics unit, as we see these pressures persisting into the near future, leading to lower revenue and profit most likely in the U.S. Generics in 2018 and potentially 2019. All of these factors, which became strongly evident during Q2, triggered us to review and impair our goodwill to align our revised expectations for the performance of this business in our balance sheet.

Our attraction to Teva was largely based on the copious amount of free cash flow the entity was generating. We felt with deal synergies included, as long as the industry remained rational the debt could be paired in a rigorous manner leaving the company in sound shape. Teva is now in the very uncomfortable position of having to sell assets in order to pay down its hefty debt load.

Image Source: Teva Q2 Results

GAAP net loss attributable to ordinary shareholders and GAAP diluted EPS loss were $6.0 billion and $5.94, respectively, in the second quarter of 2017, compared to net income attributable to ordinary shareholders of $188 million and diluted EPS of $0.20, in the second quarter of 2016. Non-GAAP net income attributable to ordinary shareholders for calculating diluted EPS and non-GAAP diluted EPS were $1.0 billion and $1.02, respectively, in the second quarter of 2017, compared to $1.2 billion and $1.25 in the second quarter of 2016.

Source: Teva Q2 press release

We view the series of unfortunate events in a similar lens to the saga that continues to unfold with Valeant Pharmaceuticals (VRX), which saw its share price crushed when allegations of channel stuffing and some unsavory business practices came to light. Valeant is unwinding years worth of deal making leaving behind a company that is a shell of its former self. We fear a similar fate may await Teva as it attempts to pare off some divisions to raise cash, and Teva is locked in arbitration with Allergan over a provision in the deal for Actavis.

Concluding Thoughts

The series of unfortunate events following the Actavis transaction underscores the inherently-risky nature of equity investments (especially those that pursue large debt-funded acquisitions), but we are not giving management a pass for its blunder in doubling down on a perceived competitive advantage that looks to have been nothing more than castles in the air. We are utilizing the failure of the deal as a case study of the effect of leverage in an industry that is rapidly commoditizing, and the adherence to position sizing (i.e. that Teva was only but a small position in the Best Ideas Newsletter portfolio and that we removed it well before the last leg down) will allow us to recoup from this misadventure. Stay tuned for future updates as we continue to follow Teva’s story.

Healthcare and Biotech Contributor Alexander J. Poulos is long CVS Health.

Tickerized for stocks mentioned in original thesis on the generics space as well as those mentioned in the article.

Related ETFs: XLV, IBB