Member LoginDividend CushionValue Trap

|

Economic Commentary – Politics, the WeWork Debacle, and How We Use the Valuentum Buying Index in the Newsletter Portfolios

publication date: Oct 27, 2019

|

author/source: Valuentum Analysts

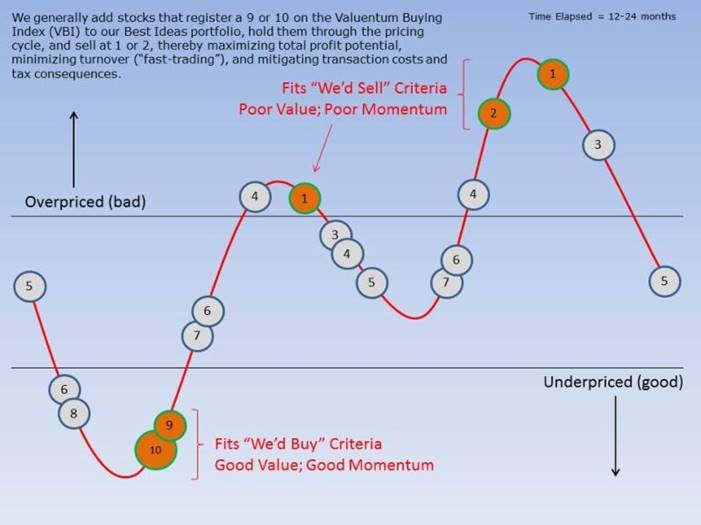

In our latest Economic Commentary, the Valuentum team continues its discussion on politics and the markets and the implications of a potential WeWork failure on the commercial real estate and construction markets. We’ll also address a very important question: Why are there lower Valuentum Buying Index ratings in the newsletter portfolios at times? The answer is rather straightforward and a good thing! Let’s get started. Christopher Araos: One comment about the upcoming elections. The previous one proved to the world how susceptible the general populace of America is to propaganda from abroad--when they could organize rallies for locals to go to and from countries like Ukraine and Russia (RSX). My concern is this literally opens up a can of worms/pandora's box. What would stop other countries from publishing their own propaganda to further their own interests that would contradict the US’? Granted this is already legally done via interest groups, but you get the general idea of the cause of concern for this snowball. Callum Turcan: We are witnessing the stress that rising global connectivity is placing on democracies. Democracies aren't walled gardens, and that creates openings for malevolent actors, particularly those backed by large geopolitical apparatuses. I would say this is a serious problem for all democracies (particularly "true" democracies), not just in the US, and the Eurozone has been another target for anti-Western actors. It's much harder for the West to respond in kind, but to be fair, Western geopolitical actors have long interfered/intervened in the political affairs of other nations. For instance, when the US pushed Ethiopia behind the scenes to invade Somalia in 2006. That geopolitical event came to light after WikiLeaks published cables indicating the US official Jendayi Frazer (who was then US Under Secretary of State for Africa) encouraged Ethiopia to invade in order to weaken the growing influence of the Union of Islamic Courts in Somalia at the time. Switching gears a bit, in other news, WeWork continues to have cash problems. I don't think our portfolios have too much direct or indirect exposure to WeWork's problems, however, given how WeWork is a really big player in Manhattan, London, and Washington DC while our REIT picks operate elsewhere or cater towards completely different markets entirely. For Realty Income Corp (O), a Dividend Growth Newsletter portfolio holding, this REIT has economic interests in properties across 49 states in the US--along with economic interests in properties in Puerto Rico and more recently, the UK (EWU)--and doesn't appear to be exposed to WeWork's problems in a significant way given its extensive geographical diversification. The REIT isn't really exposed to any potential Brexit headwinds either given how Realty Income expanded overseas for the first time this year, with its UK operations representing just ~1% of total annualized rental revenues. In the case of Corporate Office Properties Trust (OFC), an Exclusive idea (read more about the Exclusive publication here), the REIT has some exposure to WeWork's problems given its large presence in the Washington DC market. However, it is very important to note that this REIT caters to highly specialized Defense/IT needs (the properties in which Corporate Office Properties has economic interests in that cater to these needs represented ~88% of annualized rent revenues as of September 2019). More broadly, the REIT's performance depends far more so on annual federal defense and IT-related spending levels than anything else, aside from changes in interest rates and its credit rating (which is investment grade and S&P Ratings gives the firm a positive credit rating outlook). The outlook on all three of those fronts looks bright going forward. Regarding Eastgroup Properties Inc (EGP), another Exclusive idea, that REIT operates across the Sun Belt and not in markets where WeWork is a significant player. That includes properties Florida, Texas, Arizona, California, and North Carolina. In regard to National Health Investors Inc (NHI), another Exclusive idea, this is a specialty housing/nursing oriented REIT that has no exposure to WeWork's problems as it caters to seniors across America, not corporate office needs in the middle of Manhattan. For our Vanguard REIT ETF (VNQ) pick, a BIN holding, I think the extensive levels of security diversification removes any concerns we would have relating to the ETF's WeWork exposure. In summary, our newsletter portfolios and Exclusive ideas don't seem exposed to WeWork's problems in any significant way across the board, which may be a sleeper problem for some REITs (and portfolios comprised of those REITs, which have been big winners of late) in the near-future given how WeWork might run out of money (a liquidity crunch could send WeWork into bankruptcy, but the firm appears likely to still have at least some access to capital markets, at least across to reports from CNBC, WSJ, Bloomberg, etc.). Please note major financial media outlets are reporting that WeWork will likely get a major cash infusion from SoftBank Group (SFTBY), staving off a possible bankruptcy filing in November, but that doesn’t mean WeWork’s problems are over. Far from it, given the firm’s enormous losses and major long-term obligations. To the Valuentum team, what do you think would happen to key global markets for real estate (i.e. Manhattan, London) and thus certain REITs if WeWork went under (because it couldn't tap capital markets at realistic rates and decided to file for Chapter 11 instead sometime in the future)? Brian Nelson: The entire WeWork situation is rather interesting. For starters, that the investment banks were trying to push this offering to the markets and individual investors really showcases the importance of independent stock research. Independent stock research firms such as Valuentum play a very important role warning investors about the risks of these types of investment blunders. Second, WeWork isn’t just a troubled company, but truly a junk-rated one in a liquidity crunch. Fitch, for example, recently downgraded WeWork two notches to CCC+ -- that’s not good at all, and while there are deep junk-rated entities like Netflix (NFLX), as one example, that continue to prove the equity markets wrong, WeWork’s credit rating is just a few notches above the worst rating possible – and it was going to be take public! To me, this situation may be reminiscent of the dot-com bust, particularly in how WeWork’s expected value dropped from some $50 billion to a fraction of that today. Echoing Boston Fed President Rosengren’s concerns, the WeWork business model, which facilitates co-working and flexible workspaces could result in somewhat of a similar dynamic with what happened during the housing crisis late last decade, when homeowners just handed the keys back to the bank causing severe loss rates. Where during the Great Financial Crisis the pain occurred in residential markets and housing loans, WeWork’s business model could cause severe spikes in commercial vacancies during the next downturn, driving higher commercial loss rates at various banks. How severe these loss rates might be is anyone’s guess. In the event that WeWork files for Chapter 11 reorganization today, with a benign economic backdrop, it will likely be an orderly process, and the economy likely won’t feel it much (it could be a catalyst for more trouble to come, however). The assessment of the implications on WeWork’s failure changes, however, if we start heading down the road of recession. In this case, the failure of WeWork’s business model could exacerbate a general slowdown, with reverberations on the banks and commercial lending market and further implications across other sectors from construction to industrial goods and other related industries. Matthew Warren: WeWork’s whole business model seems like it’s on shaky ground. The company is essentially arbitraging long-term leases into short term rentals for (in some cases) questionable tenants. It would be one thing if the firm owned the properties like an AirBnB lessor, but it doesn’t. Not only is WeWork leasing the space, it is then re-leasing it--and also doing it via special purpose entities, so that the firm can mail in the keys on properties that don’t work out. The thing is if WeWork actually did that, no one would ever want to lease to them again and the business model would break. A downturn in the economy will also severely test the model, as we would see how their short-term rentals hold up--and that’s all assuming they can find the equity and debt capital the firm needs to keep covering operating losses as it “scales up”. The fundamental question is: are they truly scaling into profitability or did the firm expand beyond what the total addressable market (TAM) can absorb? If WeWork ultimately fails, the lenders would probably own them post-bankruptcy. That would only best time to answer the fundamental question of whether this business model works at this scale (there are smaller comps that have operated similar business models at much smaller scale for a long time). Brian: Fantastic commentary all. We continue to watch the political backdrop and commercial real estate markets closely. As we wrap up, I wanted to address something that may be confusing to new members. It has to do with why there are sometimes lower Valuentum Buying Index ratings in our newsletter portfolios. In short, this is a good thing – it means our ideas are working! -- but let’s elaborate on the topic. For new members, the Valuentum Buying Index, or VBI, helps to inform which ideas we include in the Best Ideas Newsletter portfolio. This is where some clarification is probably important. For one, the word choice “inform,” is critical, because the VBI is generally just one factor that goes into whether we add a company to the Best Ideas Newsletter portfolio, even if the VBI is one of the most important factors. Second, the timing element or duration concept is a key consideration. We've noticed via our statistical backtesting that a momentum factor can be much more pronounced (powerful) over longer periods of time. This was one of the interesting findings of our academic white paper study (2012). We try to consider this dynamic with the update cycle of our reports (and the time horizon for ideas to work out). That's why our reports are updated regularly…or after material events and not daily or weekly. Perhaps most practically though, we don't think portfolio churn is the way to generate outperformance. Momentum may be high turnover, but Valuentum is low turnover. Though the time frame varies depending on each idea that we consider for the Best Ideas Newsletter portfolio, we would expect our best ideas to generally work out over a 12-24+ month time horizon (on average). Not all ideas will be successful, however. Our "holding period" is targeted to be much, much longer for some ideas in the Dividend Growth Newsletter portfolio, as income and dividend growth are other key factors (in addition to the Valuentum Buying Index and capital appreciation potential). The time horizon or duration concept is where the Valuentum Buying Index rating system becomes more complicated than a simple 1, 2, 3. For example, we tend to "add" stocks to the Best Ideas Newsletter portfolio when they register a 9 or 10 on the Valuentum Buying Index, "hold" them for some time depending on a number of variables (the VBI, market conditions, sector weightings within the portfolio itself), and then we tend to "remove" stocks from our Best Ideas Newsletter portfolio when they register a 1 or 2 on the VBI. You'll notice that we have a qualitative overlay for the Best Ideas Newsletter portfolio (and one for the Dividend Growth Newsletter portfolio, too, based on dividend-related considerations).

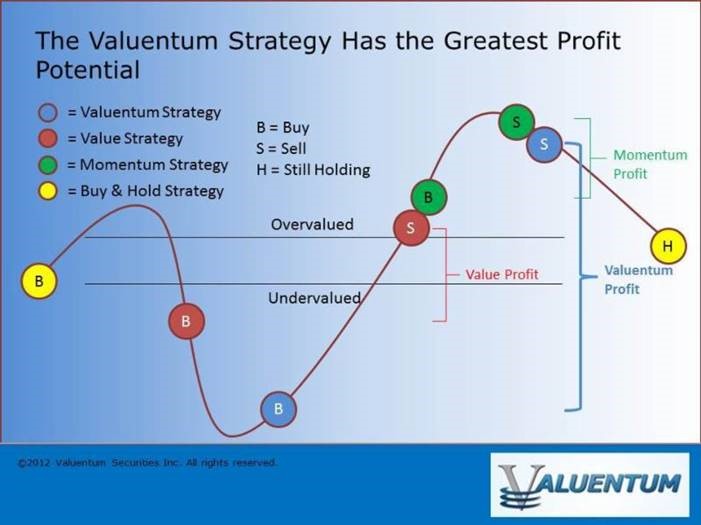

Image shown for informational/illustration purposes only. Valuentum is an investment research publishing company.--- But why don't we churn our ideas by updating daily and trading a lot? Obviously, we don't think that's the secret to investment success. In quite the opposite approach, we strive to maximize “profits” on every idea that we pursue, with the understanding that momentum does exist and that prices over and under shoot intrinsic value all of the time. For example, as shown in the image above, a value strategy (10 --> 5) truncates potential profits, while a momentum strategy (4 --> 1) ignores profits generated via value assessments. At Valuentum, we're after the entire profit potential of each idea. So, for example, if a firm is added to the Best Ideas Newsletter portfolio as a 10 and is removed as a 5, we would have truncated profit potential by not letting it run to lower ratings. Most of our highly-rated Valuentum Buying Index rated stocks have generated the "outperformance" of the Best Ideas Newsletter portfolio, but these stocks' ratings declined over time as they were held (a good thing -- a declining VBI rating generally means the share price has advanced, assuming all else is well).

Image shown for informational/illustration purposes only. Valuentum is an investment research publishing company.--- Regarding the Valuentum process, as it is executed in the Best Ideas Newsletter portfolio, we do not "add" all stocks that register a 9 or 10, nor do we add the ones we do immediately thereafter. For example, Google (GOOG, GOOGL), now Alphabet, a current Best Ideas Newsletter portfolio holding, registered a 10 on the Valuentum Buying Index, but we remained patient and didn't add the company to our portfolio until after it reported earnings at the time, providing us with an even better entry point (as new information came to light). There are more "structural/timing" instances like the one with Alphabet, for example, that are extremely difficult to capture in any model, and understandably aren't as obvious to those outside looking in. Macro-economic, broader market valuation, and sector weighting considerations are other factors that impact the qualitative portfolio management process. But why not add every highly-rated stock on the Valuentum Buying Index to the Best Ideas Newsletter portfolio? Think of it as if you were to imagine a value investor not adding and holding every undervalued stock to his/her portfolio. He or she wants the very best ones, in his or her opinion -- obviously, that means having to leave some good ideas behind. And then, of course, there are always tactical and sector weighting considerations in any portfolio construction, yet another reason why the human touch remains a vital aspect of the Valuentum process. At the core of how we use the VBI in the Best Ideas Newsletter portfolio, however, is a qualitative portfolio management overlay. The VBI rating helps to inform the process, but the Valuentum team makes the allocation decisions of the newsletter portfolio on the basis of a number of other firm-specific and portfolio criteria. Sometimes, under certain market conditions, we may even have to relax the VBI criteria entirely in order to do what we think is required to achieve newsletter portfolio goals. In all, the Valuentum Buying Index rating system, as with all methodologies, helps to inform the investment decision process, but in constructing the newsletter portfolio, a qualitative overlay is not only necessary, in our view, but helps to optimize performance. If the returns of the Best Ideas Newsletter portfolio during the past 5+ years are any measure of the VBI rating system, it is performing fantastically well. Of course, please always contact your financial advisor to determine if any idea or strategy may be right for you. |

0 Comments Posted Leave a comment