Member LoginDividend CushionValue Trap

|

As Expected--MLP StoneMor Partners Slashes Distribution!

publication date: Oct 27, 2016

|

author/source: Brian Nelson, CFA

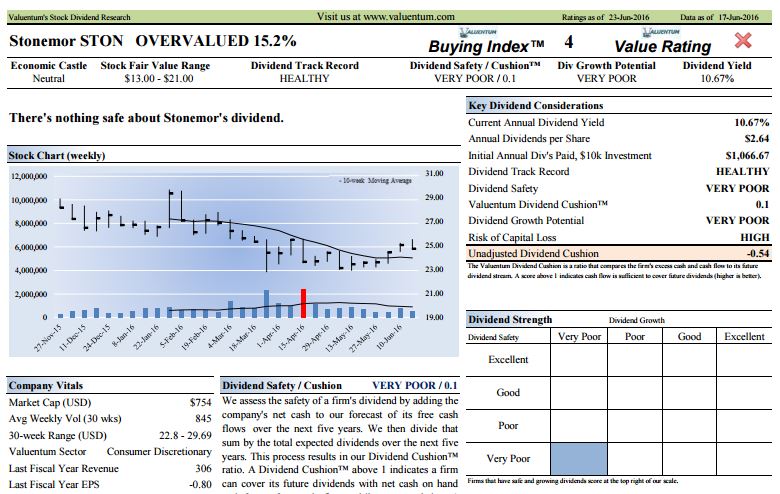

Image: A clipping of Valuentum's dividend report on StoneMor Partners. We continue to defend the individual investor! StoneMor Partners (STON) is about the most risky entity in all of our coverage universe, and it showed why after the trading session, October 27, by cutting its distribution! Yes, yet another MLP! For those that listened to us about the severe risks of its business model, we salute you. The MLP has been what we call a double whammy--it’s on Valuentum’s most overvalued list here, and it had a Dividend Cushion ratio of 0.1, now -0.7 (anything less than 1 is risky, but close to or below 0 implies significantly heightened risk). Shares are indicated down 25% after the close October 27. Before going further, I am pleading with you. If you are still reading free research and analysis, which told you that StoneMor’s dividend was okay (or is included in some “model” portfolio), I am begging you to stop reading the source of the work…for your own sake. You know that we continue to exceed the benchmark performance in the respective newsletters, and our efforts to help the income investor have been second to none! We are a paid service for a reason! It showed why in an absolutely huge way today. Okay – enough of my pleas. Here’s what we said about StoneMor’s distribution in its Dividend Report (pdf): Key Strengths There’s nothing that any bullish (optimistic) holder of Stonemor’s units could ever say to make us feel comfortable with an investment in the MLP. Its free cash flow is insufficient, and its balance sheet is “buried” under a significant amount of debt. The MLP is incredibly capital-market dependent and has used the issuance of new units (equity) to fund operating cash flow shortfalls to keep its distribution “alive.” In the past three years alone, Stonemor has issued ~$290 million in new equity (dilution). The company’s personal care trust funds are tied to market activity, and its pre-need business causes severe business cash-flow imbalances. Stonemor’s distribution may not make it through the most difficult times. Potential Weaknesses We’re going to call it how it is: Stonemor’s distribution is far from safe. The master limited partnership (MLP) business model is one that we’re not particularly fond of, and while some investors are comfortable with the term distributable cash flow, we are not. We prefer the traditional measure of free cash flow when evaluating the health of a payout, and Stonemor’s cumulative free cash flow generation during the past three years (2013-2015) of ~$5.3 million is a mere fraction of its cash distributions paid over the same time period ($190+ million). Long-term debt of ~$640 million relative to a negligible cash balance of $15 million should send income investors running for cover. We’d be scared “to death” holding Stonemor for income purposes. When a company’s or MLP’s Dividend Cushion ratio flashes a dangerous signal, my goodness, please take it seriously. It doesn’t guarantee disaster, but it spells significantly heightened risk given that the entity simply doesn’t have a lot of cushion to work to cover the payout. In StoneMor’s case, it didn’t have the capital it needed to support revenue initiatives, and therefore had to use cash that otherwise had been going to unitholders to do so. Our fair value estimate for StoneMor was $17 per share prior to the share-price collapse (now the fair value is $11). By the way, check out page 3 of the March 2016 Dividend Growth Newsletter here (pdf) – “StoneMor’s Shares Are Gravely Overpriced.” You can download StoneMor’s full report here (pdf). Please let us help! In order to make sure your membership is current, please contact us at info@valuentum.com. Don’t let free research and analysis cost you dearly! We’ll be here for you. Valuentum isn't going anywhere. We got yet another one spot on. Article updated following release of Valuentum's updated reports on StoneMor. Includes new fair value estimate and Dividend Cushion ratio. |

0 Comments Posted Leave a comment