ETFs are rapidly becoming the preferred investment vehicle to gain broad exposure to a particular sector. The biotech industry is no different with two distinct ETFs dominating the niche. The article discusses the unique characteristics of the SPDR Biotech ETF to determine the merits of the idea.

By Alexander J. Poulos

Introducing the S&P Spider Biotech ETF

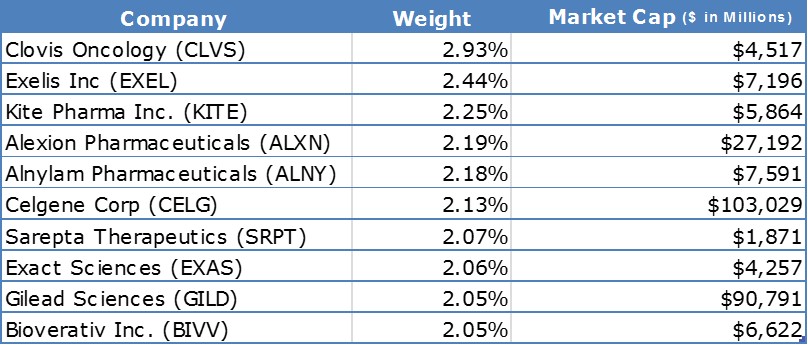

The SPDR S&P Biotech ETF (XBI) is a position weighted index with the top 10 components accounting for less than 25% of the overall assets of the index (see image below). The XBI differs sharply from its primary rival the iShares Nasdaq Biotech Index ETF (IBB) which is market-cap weighted with industry stalwarts such as Amgen (AMGN) accounting for over 8% of the portfolio. The iShares ETF runs a concentrated portfolio of large cap biotech entities, with the top ten holdings accounting for over 58% of all assets in the ETF (holdings not shown).

Top Ten Holdings of the SPDR S&P Biotech ETF (XBI)

Source: S&P SPDR Biotech ETF (XBI)

Upon first glance, outside of industry heavyweights Celgene (CELG) and Gilead Sciences (GILD), the top ten holdings in the SPDR S&P Biotech ETF (XBI) consists of an eclectic mix of exciting late stage companies. These late stage companies sometimes offer the greatest upside potential, but the upside is frequently tempered with an elevated level of risk. To pare overall firm-specific risk, however, we feel the structure of the XBI allows for broad exposure to a large basket of biotech equities without necessarily an excessive amount of exposure to the risks of any one biotech’s potential pipeline disappointments, a scenario that is all too familiar in the space and can result in wild swings in equity prices, particularly among small cap companies. Let’s examine some the top ten holdings of the the SPDR S&P Biotech ETF (XBI) further to gain a better understanding for the ETF.

Top XBI Holding Clovis Oncology (CLVS)

Clovis Oncology is a late-stage company with a focus in oncology. A bit of history is necessary to underscore the risky nature of drug discovery. Early investors in Clovis were severely burned in late 2015 when its clinical studies of breakthrough therapy-tagged Rociletinib in EGFR T790M+ lung cancer failed to gain approval from the FDA. Expectations were running high with shares trading comfortably above $100 when the first signs of non-efficacy began to assert themselves.

Clovis, however, decided to terminate ongoing studies, and the focus was thrust onto its other promising molecule, the PARP inhibitor Rucarapib. A product designated as a breakthrough therapy by the FDA failing to obtain marketing approval remains a rare event, but it is clearly not out of the realm of possibilities.

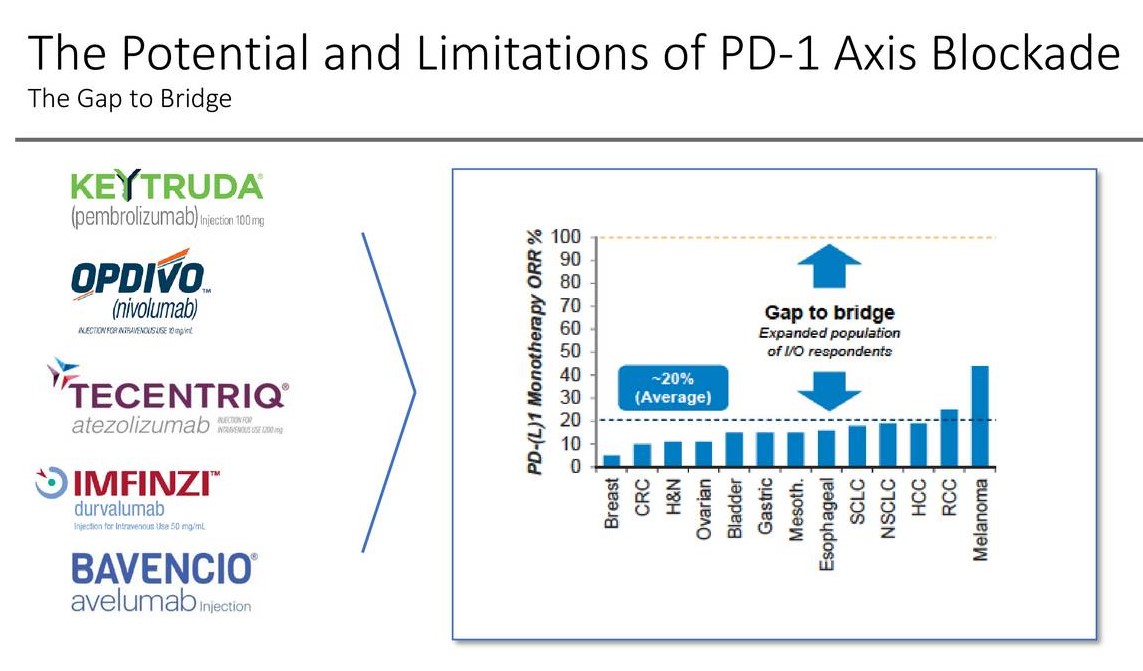

In what must have been a relief for long-term Clovis bulls, the FDA has granted marketing approval for Rucarapib under the trade name Rubraca. Rubraca is the third entry into the field, but we feel the potential of the class is vast as additional combination therapies to pair with PD-1’s are necessary. The overall response rate (ORR) utilizing a PD-1 as monotherapy is less than 20% outside of Renal Cell Cancer (RCC) and Melanoma.

Image Source: Incyte ASCO Investor Presentation June 2017

We feel Clovis has a viable product but additional trials are necessary for multiple indications that will ultimately determine the overall sales potential of the product. Clovis has wisely used the euphoria over the clinical win to enter the market with a secondary share offer to raise funds to use for additional clinical trials. We are watching events as they develop at Clovis–stay tuned for updates.

Top 10 XBI Holding Sarepta Therapeutics (SRPT)

Sarepta Therapeutics has a bit of a checkered history that is worth examining. Its lead product is EXONDYS 51 a treatment for Duchenne Muscular Dystrophy (DMD). Duchenne’s is an inherited genetic disorder where the body lacks dystrophin, a key component that allows muscles to remain intact. Symptoms begin to develop at the age of three with an ultimate life expectancy in the mid-teens. The primary areas affected are the arms and thighs making everyday activities such as climbing stairs or raising your hand complicated. Patients afflicted with DMD often become confined to a wheelchair.

As part of the clinical trials process, Sarepta began testing the product on children afflicted with DMD. Parents felt their children made significant improvements but the FDA deemed the results inconclusive. An aggressive lobbying campaign began with multiple state and Senate representatives voicing their support for the parents of the children afflicted with DMD. The issue was the lack of viable alternatives–the parents believe they should have been granted access to hopefully stave off symptoms as long as possible. The FDA finally relented, and the product was approved for use in September 2016.

In our view, the most appealing late stage biotechs are those that have a large addressable market or a key niche with limited competition. An example of a large addressable market with limited competition is Regeneron Pharmaceuticals’ (REGN) recently approved (May 2017) product Dupixent for atopic dermatitis. The atopic dermatitis market looks to be a large, well-defined patient population with little in the way of competition, and shares of Regeneron are beginning to reflect the promise of Dupixent.

EXONDYS 51 falls into the category of a well-defined niche product with an absence of competition. Thus far, uptake remains challenging as payers initially balked at covering the product. Some feel the product is an “elegant placebo”–hence they are reluctant to authorize lofty rare drug prices for the product as drug prices remain a hot button issue in the US. Though the breaking of barriers to improved uptake may be an ongoing battle, if more positive data regarding the efficacy of the drug becomes available, EXONDYS 51 has material potential as a viable commercial product.

Conclusion

Biotech-related ETFs, especially either the XBI or IBB, may be an interesting way to gain exposure to the true innovators in medicine without taking on the risks associated with any one company’s potential pipeline disappointments. In our view, the iShares Nasdaq Biotech Index ETF (IBB), with its aggressive allotment to the large cap well-established biotechs can be viewed as a more conservative play on the sector (it does have some firm-specific concentration risk at the top, however), while those that may wish to gain exposure to smaller companies that are relatively more sensitive (in terms of both upside and downside) to the outcome of any one clinical trial, the SPDR S&P Biotech ETF (XBI) may be a more appealing consideration.

Disclosures: Healthcare and biotech contributor Alexander J. Poulos is long Regeneron, Bioverativ and the XBI.