Member LoginDividend CushionValue Trap

|

China Trouble: Plenty of Pain to Go Around

publication date: Jun 24, 2013

|

author/source: RJ Towner and Brian Nelson, CFA

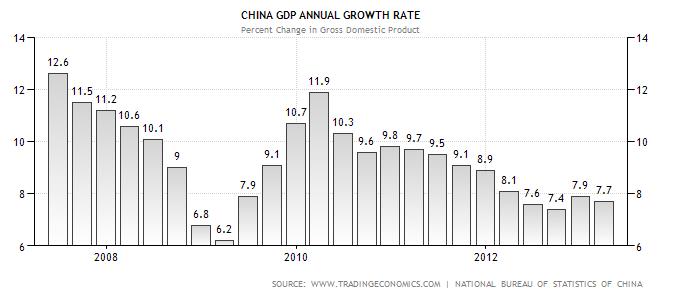

Global stock markets have struggled mightily over the past few weeks, mostly in conjunction with the Federal Reserve hinting at a possible change in monetary policy. There have also been signs that global economic expansion is starting to weaken (read the World Bank's lowered global outlook for GDP growth here), particularly in China--something we had identified a number of weeks ago as cause for concern prompting us to add protection to our Best Ideas portfolio at that time. It's clear from recent data that economic growth in China will no longer be in the 9-11% range that the market has grown accustomed to, and it is our view that expansion will never return to such a pace due simply to the size of the country (absent, of course, during a recovery in the event that a deep recession does occur).

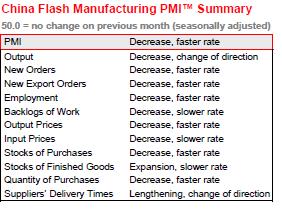

Image Source: TradingEconomics But now, credit overexpansion in China has become a very serious issue, gaining enough attention for the People’s Bank of China (PBOC) to let interbank lending rates increase in order to eliminate excessive credit creation. Though the PBOC believes the banking system has ample liquidity (it thinks the system just needs to be run more efficiently), what we learned from the recent financial crisis and Great Recession in the US is that banks and financial intermediaries tend to think liquidity is sufficient…until it's not. And investors usually don't want to be holding equities whose health depends on the healthy-functioning of the global credit markets at a time when liquidity dries up (think REITs, MLPs, BDCs). What we find most concerning about recent credit developments in China is the existence of the country's shadow banking system, where lenders, borrowers, and the quality of assets cannot be clearly identified and/or estimated. Such conditions clearly speak to increased systemic risk, in our view--something that was the primary cause of deteriorating confidence in the most recent credit crunch that toppled Lehman, Bear Stearns and others. We're also puzzled by China Bank Everbright's default on an interbank loan. If liquidity is really no cause for concern as the PBOC suggests, then why is this happening? Or better yet, how could this happen? It's our view that liquidity crises have to start somewhere, and they often start with seemingly benign indications (often readily dismissed), which spark deteriorating credit confidence between intermediaries (and eventually credit and/or liquidity events). Overall credit in China is estimated at some $23 TRILLION, or about twice its GDP. Credit has grown faster in China during the past five years than in any other place or at any other time in history. Whether the Chinese banking system is intentionally bursting its credit bubble or simply trying to correct poor banking practices is not as important as the potential impact of the Chinese credit bubble actually popping. The market is heavily focused on the liquidity issue (and rightfully so), but we also note China’s manufacturing PMI has come under pressure. HSBC’s China flash PMI (initial) for June, released last week, came in at a very poor 48.3, a nine-month low indicating ongoing manufacturing weakness (the reading was 49.2 in May--any number below 50 indicates contraction). Importantly, ‘new orders’ and 'backlogs of work’ seem to be decreasing at a faster rate in the country than before, according to the flash PMI summary.

Source for Images: HSBC (compiled by markit) - pdf The most obvious consequence of tightening credit in China is a domestic slowdown in the country, which would hamper performance of constituents in the iShares FTSE China Large-Cap ETF (FXI), the Global X China Financials ETF (CHIX), the EGS INDXX China Infrastructure ETF (CHXX), and the iShares MSCI Hong Kong Index Fund (EWH). We'd grow particularly bearish on the Global X China Financials ETF should events head south in the country. It lists the Bank of China (Beijing), China Construction Bank Corp, and Industrial and Commercial Bank of China as its top 3 holdings, collectively accounting for about 30% of the ETF's market value. We're less concerned about a global contagion to the US banks, given recent stress test performance. However, a China slowdown will still have far-reaching implications. The mining sector is particularly sensitive to Chinese economic growth, with iron ore purchases largely driven by Chinese consumption. Among the firms particularly sensitive to China are miners such as BHP Billiton (click ticker for report: BHP) and Rio Tinto (click ticker for report: RIO), as well as mining equipment makers such as Caterpillar (click ticker for report: CAT) and Joy Global (click ticker for report: JOY). We could also see steel makers such as Arcelor Mittal (click ticker for report: MT) suffer from weak end-market demand for its products. A Chinese slowdown will also impact several consumer names. Nike (click ticker for report: NKE), for instance, reported poor results in China during its third quarter, and we could see the company report negative sales figures yet again when it issues its fourth quarter earnings. The luxury sector could also struggle, as Tiffany (click ticker for report: TIF), Coach (click ticker for report: COH), Louis Vuitton Moet Hennessey (LVMH), PPR, and even Saks (click ticker for report: SKS) generate a large portion of their sales from Chinese tourists. A number of auto makers may also experience earnings pressure from a China slowdown. General Motors (click ticker for report: GM) International Operations, which includes the firm’s Chinese business, contributed $495 million to EBIT during the first quarter, making the segment GM’s second-largest profit center. Toyota (click ticker for report: TM) already has its own problems in the Chinese car market, with consumers in China responding negatively to Japanese brands. Weakness in the broader market could put further downward pressure on the company's sales. Though we’ve noted that Best Ideas Newsletter portfolio holding Ford (click ticker report: F) hopes China can drive future profits, the country isn’t a profit driver at this time. In this respect, Ford’s slow entry into the Chinese auto market could potentially prove to be a prudent move. Valuentum’s Take We have long been concerned about developments in China, to the point where we passed on Baidu (click ticker for report: BIDU) as a holding in the portfolio of our Best Ideas Newsletter, despite the firm’s large valuation discount (we also hold Google in our portfolio as well, so we didn’t want to get overly exposed to global search). Still, it’s worth noting that none of the holdings in the portfolio of our Best Ideas Newsletter are predicated strictly on a China bull-case scenario, or even a bear-case scenario. In fact, the vast majority of our portfolio has little exposure to China. Altria (click ticker for report: MO), Republic Services (click ticker for report: RSG), Precision Castparts (click ticker for report: PCP), eBay (click ticker for report: EBAY), Buffalo Wild Wings (click ticker for report: BWLD), and DirecTV (click ticker for report: DTV) are just some our best ideas without significant exposure to China. Given the combination of potential fraud, weakening economic growth, and the incredible amount of uncertainty in the country (especially with respect to the “shadow banking system”), we plan to keep our exposure to China relatively low. NOTE: We previously warned that weakness in China is one of the largest risks to the global economy going forward, and we think this remains the case. We continue to protect the large gains in the portfolio of our Best Ideas Newsletter with a put option on the SPDR S&P 500 Trust (SPY), a position that has already jumped more than 50% since we added it one month ago. |