Member LoginDividend CushionValue Trap

|

Valuentum Dividend Cushion Catches Another: Cliffs Natural Resources!

publication date: Feb 13, 2013

|

author/source: RJ Towner

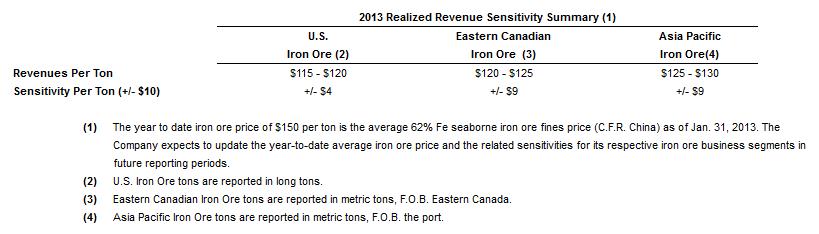

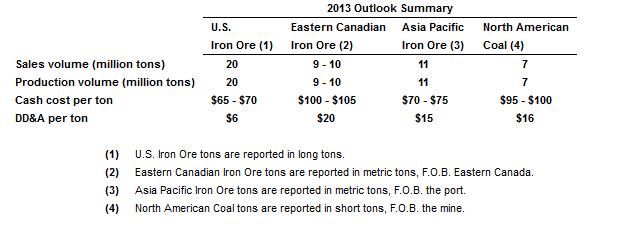

After we predicted a dividend cut in November 2012, Cliffs Natural Resources (click ticker for report: CLF) finally cut its dividend after posting poor results for 2012. The firm slashed its quarterly payout 76% to $0.15 per share. Results for Cliffs were actually a bit better than consensus estimates on both the revenue and earnings side. Total revenue declined 4% year-over-year to $1.5 billion, while earnings dipped 59% year-over-year to $0.62 per share (after adjusting for a $1 billion goodwill impairment). Free cash flow for the year was incredibly weak, falling to a negative $613 million, explaining why the dividend needed to be cut. If we only took into account the payout ratio, Cliffs’ adjusted earnings per share of $3.45 for 2012 would seem to give the dividend ample cushion (its prior annual dividend payout was $2.50 per share, an adjusted payout ratio of 72.5%). However, Cliffs is a perfect example of the significant and potential tragic pitfalls of using the payout ratio as a measure of dividend safety and why the Valuentum Dividend Cushion is one of the most important metrics for income investors to use to safeguard their portfolios from dividend-growth blow-ups. << FAQ: Where Can I Find the Valuentum Dividend Cushion Score? Capital management at the firm seems relatively weak, as the company had to write down $1 billion related to its acquisition of Thompson Iron Mines in 2011. The company also had to raise capital by selling 9 million shares of common stock and 20 million shares of preferred stock. With the firm giving relatively positive guidance (shown below) for 2013, we’re a bit shocked by this move since it has upset existing shareholders (Sources of Images: CLF).

The company’s outlook suggests stronger profitability, as China and the US are expected to have improved industrial performance in 2013. The move to raise capital is fairly prudent, in our view, since Cliffs’ balance sheet is not great, and some of the new equity will be used to reduce the company’s debt balance. Also, commodity prices have been particularly volatile—to the point that it has been rumored that producers may be buying in the spot market to help control supply. The company also intends to allocate $800-$850 million for capital expenditures during the year, so even significantly improved operating cash flow may not be able to cover the increased capital investment. We’re currently taking a close look at the firm’s valuation, and we expect to publish an updated report soon. We don’t think the dividend will return to the previous bloated levels anytime in the near future. After the firm’s steep price decline today, we continue to believe shares of Cliffs are fairly valued. We have no interest in adding the company to the portfolio of our Best Ideas Newsletter. |