|

|

Recent Articles

-

Public Storage Picks Up Simply Self Storage; M&A Remains Hot in Self Storage

Public Storage Picks Up Simply Self Storage; M&A Remains Hot in Self Storage

Jul 24, 2023

-

Image Source: Public Storage.

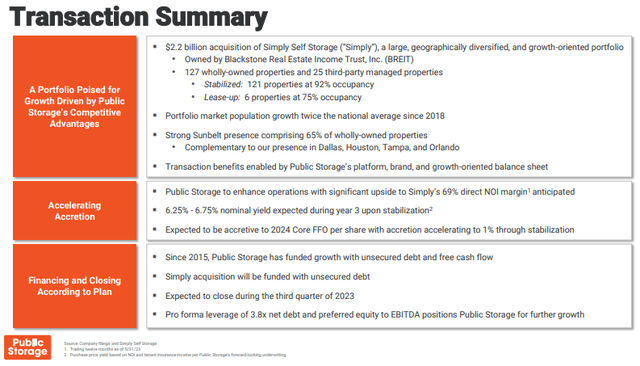

On July 24, Public Storage announced that it had agreed to acquire Simply Self Storage from Blackstone Real Estate Income Trust (BREIT) for $2.2 billion. The news follows the Public Storage-Life Storage takeout saga that ended with Life Storage running to Extra Space Storage for a deal. A PSA-LSI deal had made a lot of sense, and we’re not sure why LSI wanted nothing to do with PSA, but it may have had to do with a poor cultural fit. LSI apparently said it wasn’t for sale right before it tied the knot with EXR--moves that just didn’t seem to add up, in our view. In any case, we’re glad PSA walked away from a possible “winner’s curse” had it pursued LSI, and we’re largely indifferent to the smaller transaction regarding Simply Self Storage.

-

Tesla Is A Net-Cash-Rich, Free-Cash-Flow Generating, Secular-Growth Powerhouse

Jul 24, 2023

-

Image: Tesla’s Cybertruck showcasing its versatility. The truck is on track to begin production at Gigafactory in Texas in the coming months. Image Source: Tesla's second-quarter press release.

The cash-based sources of intrinsic value (and the trajectory of growth in them) are the most important considerations when it comes to assessing the attractiveness of an equity. Two of the most important cash-based sources of intrinsic value are net cash on the balance sheet and future expected free cash flows, and in these two areas, Tesla excels. Though we won’t be adding Tesla to any of the newsletter portfolios anytime soon, we like it within a diversified basket of large-cap growth equities, of which the Best Ideas Newsletter in some ways approximates.

-

AT&T: A High Yield Dividend Disaster, Now An ESG Nightmare

Jul 24, 2023

-

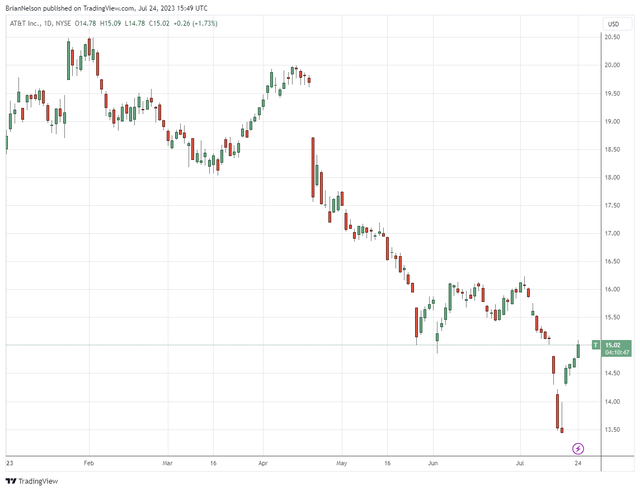

Image: AT&T’s shares continue to disappoint.

We’re not interested in AT&T at all and believe that shares may remain under significant pressure until 1) material top-line growth resumes, 2) the firm’s capital-intensity lessens, 3) free cash flow improves significantly, 4) dividend increases resume 5) its leverage improves and 6) there is more visibility related to the potential contingent liabilities associated with lead-covered cables. We doubt all six of these things will happen, and therefore we believe the best days are likely behind AT&T.

-

Philip Morris’ Cash-Flow Dividend Coverage Resilient, ZYN Performance Impressive

Jul 24, 2023

-

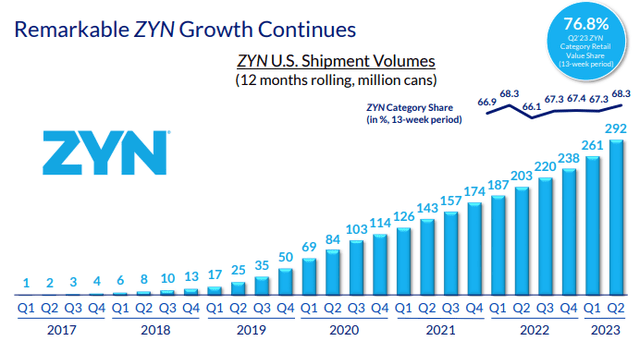

Image Source: Philip Morris.

Our fair value estimate for Philip Morris stands at $105 per share, and we don’t expect to make any material changes to our valuation of the company following the quarterly report. Philip Morris’ combustible tobacco revenue continues to be strengthened by pricing power, while its smoke-free momentum, particularly with ZYN, continues. Though adjusted financial measures continue to look good at Philip Morris, more and more we’re paying closer attention to reported diluted earnings per share, which will face material pressure in 2023 ($5.36-$5.45 per share) compared to $5.81 per share in 2022. The company’s free cash flow remains robust, but its total debt levels are not ideal, in our view. Philip Morris is trading just shy of $100 with a dividend yield of ~5.2% at the time of this writing.

|