|

|

Recent Articles

-

Chipotle’s Long-Term Growth Outlook Intact

Chipotle’s Long-Term Growth Outlook Intact

Oct 26, 2023

-

On October 26, Chipotle Mexican Grill reported better-than-expected third-quarter results with the top line increasing 11.3% on a year-over-year basis and non-GAAP earnings per share beating the consensus estimate. Comparable store sales advanced 5% in the period, while the company drove meaningful improvement in its operating margin, despite nagging inflationary pressures in beef and cheese prices. We’re huge fans of Chipotle’s long-term unit growth story, and we expect the rollout of Chipotlane drivethru’s to pave the way for an expanded menu, maybe in the breakfast daypart in the years ahead.

-

Brief Take: Altria’s 10% Dividend Yield Is Too Hard to Pass Up

Brief Take: Altria’s 10% Dividend Yield Is Too Hard to Pass Up

Oct 26, 2023

-

Altria Group’s forward estimated 10% dividend yield is too hard to pass up as it is comfortably covered by traditional free cash flow. The tobacco giant reported third-quarter 2023 results on October 26 that showcased how its asset-light business model continues to throw off tons of cash. Traditional free cash flow generation came in at ~$5.9 billion during the first nine months of 2023, while cash dividends paid came in at ~$5 billion, resulting in a very nice free cash flow cushion on a ~10%-yielding stock. Though revenue growth at Altria remains under pressure, gross profit continues to move in the right direction. Altria has raised its dividend 58 times during the past 54 years, and the firm continues to target mid-single-digit dividend growth annually. For income investors that aren’t worried about ESG-related criteria, Altria could make for a great diversifier in a high-yield dividend income portfolio. Our fair value estimate stands north of $60 per share (shares are trading under $40 at the time of this writing).

-

Albemarle and ASML Holding Remain Key ESG-Focused Ideas

Oct 26, 2023

-

Two of the companies included in the simulated ESG Newsletter portfolio are Albemarle and ASML Holding. Recently, concerns over the supply/demand dynamics for lithium have hurt Albemarle’s stock, but we’re being patient with this ESG-focused idea. On October 18, ASML Holding reported decent third-quarter results. We think ASML is one of the most competitively advantaged players in the semiconductor space, and we won’t be removing it from the ESG Newsletter portfolio anytime soon.

-

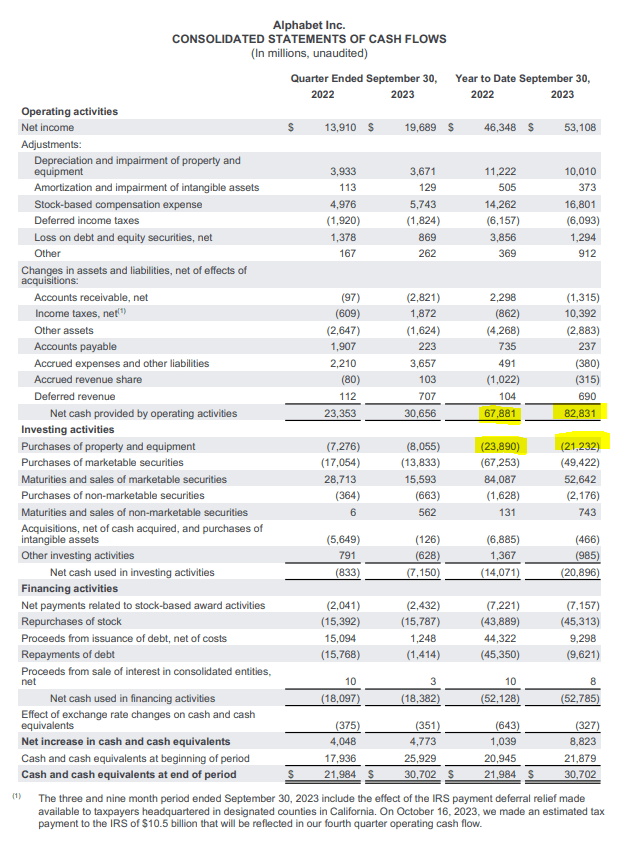

Alphabet and Meta Are Net-Cash-Rich, Free-Cash-Flow Generating, Secular-Growth Powerhouses

Oct 25, 2023

-

Image: Free cash flow growth at Alphabet has been phenomenal during the first nine months of 2023.

Both Alphabet and Meta are net-cash-rich, free-cash-flow generating, secular-growth powerhouses. Though cloud revenue growth and the pace of expense expansion at Alphabet are concerns, and while Meta may experience some softness in advertising revenue during the current quarter, both entities’ quarterly performances during the calendar third quarter showcased why they have been market darlings during 2023.

Note: We’ve corrected our updated report on Alphabet. We had previously uploaded an incorrect version, but this version (pdf) has now been corrected. There is no change to the updated fair value estimate of $133 per share.

|