|

|

Recent Articles

-

Main Street’s Dividend Track Record Is a Sight to See

Main Street’s Dividend Track Record Is a Sight to See

Aug 22, 2024

-

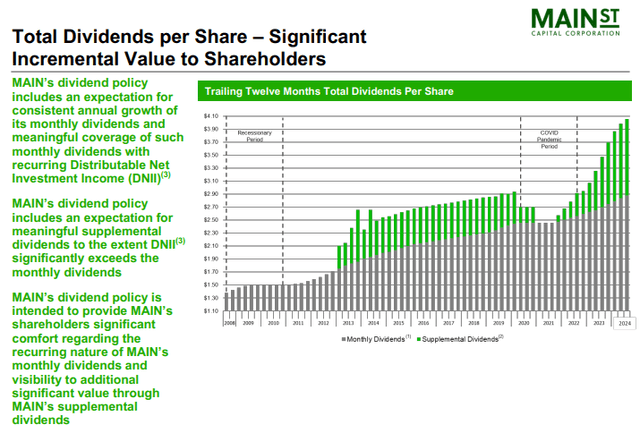

Image: Main Street has never lowered its monthly dividend, and it has paid supplemental dividends to bolster its yield. Image Source: Main Street.

Main Street has never decreased its monthly dividend rate, with monthly dividends up more than 120% from $0.33 per share in the fourth quarter of 2007 to its declared dividends of $0.735 per share in the fourth quarter of this year. On a regular monthly dividend basis, shares of MAIN yield ~5.9%, but its supplemental dividends help to pad that annual rate. The company’s investment-grade credit ratings offer it the ability to take advantage of opportunities in the market, and we think shares are worth a look for the income investor.

-

ExxonMobil’s Free Cash Flow Remains Impressive

Aug 22, 2024

-

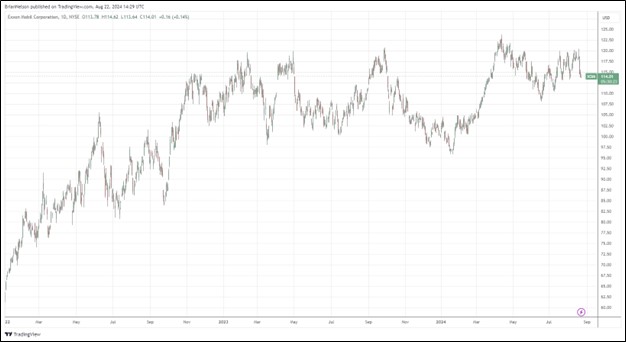

Image: ExxonMobil’s shares have done quite well since the beginning of 2022.

We like the cash-flow profile of ExxonMobil, and its purchase of Pioneer offers the company continued integration and synergy benefits. Exxon’s record production in Guyana and Permian was welcome news, with total Upstream net production advancing 15% in the second quarter from the first quarter of the year. The company has achieved $10.7 billion in cumulative structural cost savings since 2019, and management noted that it is on track to deliver cumulative savings totaling $5 billion through the end of 2027 versus 2023. Our fair value estimate of ExxonMobil stands unchanged at $114 per share.

-

TJX Companies Boosts Profit Guidance

Aug 21, 2024

-

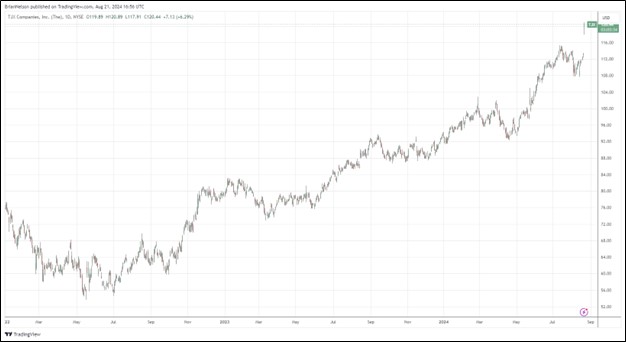

Image: TJX’s stock has been on a tear over the past couple years.

TJX expects consolidated comparable store sales growth to be between 2%-3% in the third quarter. Pre-tax profit margin is expected in the range of 11.8%-11.9% for the quarter, while diluted earnings per share is targeted in the range of $1.06-$1.08. For the full year fiscal 2025, consolidated comparable store sales are expected to be up ~3% (was 2%-3%), and the company raised its pre-tax profit margin to 11.2% and raised its diluted earnings per share outlook to be in the range of $4.09-$4.13 (was $4.03-$4.09). Though we liked the quarter and raised profit guidance, TJX’s shares are not cheap. We’re sticking with our $106 per share fair value estimate at this time. Shares yield 1.3%.

-

Target’s Second Quarter Results Better Than Feared

Aug 21, 2024

-

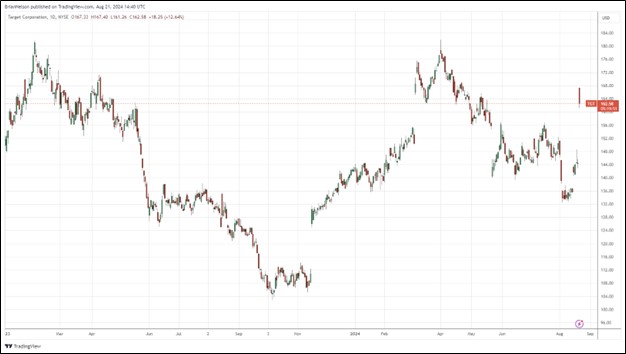

Image: Target’s shares have been quite volatile since the beginning of 2023.

Target expects a 0%-2% increase in comparable store sales and adjusted earnings per share in the range of $2.10-$2.40 in the third quarter (consensus was $2.24). For the full year, management thinks that comparable store sales growth will be in the 0%-2% range, with an increased likelihood that the increase will be in the lower half of the range. Target, however, now expects full-year GAAP and adjusted earnings per share in the range of $9.00-$9.70, which is up from previous expectations in the range of $8.60-$9.60 and the midpoint higher than the consensus forecast of $9.22 per share. Our fair value estimate of $155 per share remains unchanged at this time. Shares yield 3.1%.

|