VIDEO/TRANSCRIPT: 2021 Valuentum Exclusive Call: Inflation Is Good

Valuentum's President Brian Michael Nelson, CFA, explains why investors should not fear inflation, why government agencies such as the Fed and Treasury are prioritizing something other than price discovery, why the 10-year Treasury rate is a must-watch metric, and why Valuentum prefers the moaty constituents in large cap growth due to their net cash rich balance sheets, tremendous free cash flow generating potential, and secular growth tailwinds.

Transcript:

On behalf of the Valuentum team, I’d like to present to you our prepared remarks for the Valuentum Exclusive conference call for 2021. It is both an honor and a privilege to share our team’s work with you, and I personally am very grateful for your continued interest in our thoughts and outlook.

Let me be very clear. I am bullish on stocks for the long run and very bullish on the area of large cap growth.

Despite the fear mongering by much of the press, inflation is good for nominal equity prices, provided that interest rates, which capture the market’s expectations for inflation, remain at all time lows, which they continue to be.

Inflation helps to drive pricing power and outsized free cash flow growth at some of the largest and strongest companies, making their investment characteristics even more attractive. Elevated, but manageable inflation, and low interest rates are the best of both worlds for stock prices, in my view.

Let us further explore inflation because it can impact different investors in different ways.

For those in debt, inflation may very well be your best friend. Inflation reduces the value of your debt, whether student loan, credit card, mortgage or other, in real terms. This, again, is a good thing.

Some of our members that are in their 60s may understand this perspective. For example, they may be homeowners, having purchased their house for $50,000 in the 1980s, a house now worth perhaps $300,000, as they continue to earn an annual salary of $100,000 each year.

As their salary advanced over time, the nominal value of that mortgage debt stayed the same, however. The increased earnings power over the years made the debt service more and more manageable.

It may go without saying that with a large percentage of Americans in debt today, inflation running a little hotter than normal is a good thing. It gives a boost to net worth for those in debt, and a boost in net worth for savers and retirees exposed to the equity markets, provided again that interest rates do not spike aggressively to drive higher discount rates within the valuation context.

In my view, moaty stocks with net cash positions, strong free cash flow growth and secular growth tailwinds continue to be one of the best ways to combat inflationary expectations. You can find many of these ideas in the Best Ideas Newsletter portfolio.

As it relates to income investors, seeking strong dividend growth payers may be one way to help offset a rising cost of living with income expansion. We think many ideas in the Dividend Growth Newsletter portfolio can help in your analysis, and the Dividend Cushion ratio helps to showcase those with the greatest financial capacity for future dividend expansion.

We caution, however, that in general the higher the dividend yield, the higher the risk of a dividend cut, and we don’t think current elevated levels of inflation will be sustained for very long. The Fed may have retired the word “transitory,” but we don’t expect runaway inflation by any stretch.

Don’t overreact. Stick to your long-term plan.

My esteemed colleagues, members, friends, and guests, we are living in a changed world. It has become clear during these past two decades that we simply do not live in free markets anymore.

This is not your grandfather’s stock market. This is not your father’s stock market – this isn’t even the stock market when I first began my career as a humble research assistant nearly 20 years ago now.

The firemen, police officers and teachers whose pensions rely on stable and advancing equity prices…

The senior manager that has been contributing to her retirement for the past 40 years that requires stock values to keep inching higher…

The mom-and-pop investor that needs strong stock returns to afford what is becoming unaffordable college education for their family…

The set-it and forget-it target date funds where investors believe all will be just magically well in 30 years…

The asset allocation rebalancers that have no interest in calculating the intrinsic value of their assets…

The stock markets weren’t necessarily created to accommodate these purposes. The stock market was created as a market, in part, to act as a mechanism where buyers and sellers come together to uncover the value of businesses through price discovery.

However, today the use of equity markets has morphed into a greater purpose because of its myriad applications, and many now depend on it for so many valuable aspects of life – and this greater purpose is completely unrelated to its original intent of price discovery.

In many ways, the stock market has become embedded in the core fabric of our society (and I’m not talking about how the #NASDAQ often trends on Twitter). The stock market affects the money we’ve saved to pay the rent, the money we need to put food on the table, the savings we require to put one’s kids through college.

The stock market is not about setting prices anymore as much as it has taken on the likeness of another government-subsidized savings mechanism, though one with greater risk and volatility.

It may not necessarily be the government’s fault, however. Only about 10% of trading today is from fundamental traders that are paying attention to intrinsic values. The rest is mostly quant and indexing.

In that respect, how could the government not be involved heavily in the markets, when the markets themselves are reflecting less and less of price discovery and more price-agnostic trading that adds little positive externalities to society.

It became very clear that the cost of indexing is not low. Most may not know that Vanguard, for example, was one of the largest owners of airlines heading into the COVID-19 crisis.

During 2020, we didn’t bail out the airlines with lifelines – they would have kept operating under Chapter 11 protection – we bailed out Vanguard’s equity stake in them – and irresponsible indexers.

That, my friends, is the true cost of indexing. When people don’t pay attention to intrinsic values and risk, the tax payer is the one that picks up the tab. Tax payers are subsidizing indexers if only to weaken the price discovery mechanism of the markets.

Sure, we can blame index funds for this as they buy anything at any price;

We can blame price-agnostic trading, perhaps the quants for only looking at basic valuation multiples and price trends,

Or the asset allocation models that care little about intrinsic value and only rebalancing at certain time intervals;

We can blame the efficient markets hypothesis for convincing people that any price for a stock is as good as the next;

[Learn about the fatal flaw of the efficient markets hypothesis here]

We can blame the financial industry for asset gathering being a primary goal, instead of achieving outsize returns.

We’re not pointing fingers. There’s really no point because here is the reality:

Millions are putting their money into the markets today not to help with price discovery by buying undervalued stocks and selling overvalued stocks, a process that enhances market efficiency and increases the fairness of prices to investors…

Rather, investors are contributing to secure their future retirement, in many cases, no more, no less. Again, only a small fraction are fundamental discretionary traders these days.

One might go so far as to say that the average investor today cares very little about the “right” price at all, but rather to make a quick buck.

Did the GameStop investor buying at $400 per share care about its fair value estimate being a fraction of that? I don’t think so.

Does the small cap quant investor really know anything about the individual stocks in their portfolio to make an informed decision about intrinsic value? Probably not. They’d be using forward-looking data, in my view, if they did.

But this is the reality of the markets today. We can’t change this, and therefore we must think more philosophically about its eventual outcome and how to position one’s portfolio for 2022 and beyond.

So then -- What is the answer to the stock market?

Perhaps we should answer this question with a few other questions? How about these:

Do we think Fed officials will allow pensions to grow vastly underfunded in the years ahead when they have the tools to prevent it from happening?

Will the Treasury simply ignore events that might punish severely the life savings of that senior manager that has worked hard for 40 years if it can use tools to avoid it?

Will government officials ignore the great problem of student loans by making it even more difficult for students to attend universities and local community colleges when they can prevent 529 plan values from faltering?

The answer, in my opinion, is no. Price discovery is no longer a priority of these markets, and it will only get worse in the coming decades. We will see levels of volatility never thought possible. [Read Value Trap for more on why the price setting mechanism is breaking down.]

However, it is also my growing contention that our governmental systems simply will not let markets disappoint savers in the longer run. They can’t. With everyone depending on the markets for almost every important part of their lives, they have too much riding on the markets now--and the historical evidence is clear, too.

The greatest flaw of former Fed Chairman Alan Greenspan, who served from 1987 through 2006, may have been that he believed in efficient markets, but the maestro, as he is often called, taught policy makers a very valuable lesson: that markets can be managed, and managed effectively.

By cutting rates aggressively in the years following the crash on that infamous October day in 1987, Greenspan showed that the government has the tools to drive markets from the depths of despair to soaring heights, setting a precedent that would eventually be used again following the dot-com crash to get the economy back on track.

[Remember our call that we were "going fully invested" in April 2020 shortly after the government stepped in to stem the crash of late March 2020?]

His successor Bernanke used the same playbook to save the U.S. economy from the housing crash, but Bernanke even took things further during the Great Financial Crisis of 2008-2009 by nationalizing the banks to stave off what would have become a depression. Current Fed Chair Powell during the COVID-19 crisis scooped up investment-grade corporate bonds to make sure markets remained orderly, in yet another example of the “invisible hand” of government assistance.

To the bears that have suffered this past decade, they have failed to recognize that the main function of the stock market is no longer one that facilitates and enhances the price-setting function, but rather it has become one that is managed closely by government officials to continue to advance the values of retirement accounts and the net worth of investors.

Short investors are not just swimming against the current as in the statistical upward drift of the markets over time due to the time value of money within the enterprise valuation construct; they are fighting against a tidal wave of government assistance that won’t ever go away.

To be successful, in my opinion, we must all recognize this new reality--but at the same time, we must all recognize that we are better off because of it, too. Were it not for the Fed’s and Treasury’s actions during the Great Financial Crisis now some 13 years ago, some might have told you there might not have been milk at the store. Were it not for the swift action by the Fed and Treasury during the COVID-19 crisis, the equity values of hundreds if not thousands of stocks would have simply been wiped clean.

We have a lot to be thankful for -- But what was the intent for not letting companies fail during the COVID-19 meltdown?

Certainly government and Congressional officials understand that we have an orderly Chapter 11 bankruptcy process that allows businesses to operate while restructuring their debt under adverse conditions. Why not just let the system work then? We’d still be able to fly just like when airlines have declared bankruptcy in the past.

The problem is that under the bankruptcy process, however, equity holders would be wiped out. The Fed and Treasury didn’t necessarily save businesses during the COVID-19 crisis, per se, as much as it saved the equity of those businesses -- or in other words, the retirement savings of investors – a good thing, of course, but a reality we must recognize, and one unnatural to free markets.

There’s no shortage of critics of the Fed and Treasury actions these days, but I’m not one of them. We are all better off because of the substantial booms created by accommodative policy and the massive support during crises. It may have been Greenspan that stated that, despite some of the crashes experienced during the past several decades, we have ended up in a better place than had we not gone through them at all.

Frankly, it’s hard to argue with this. At the closing bell on Black Monday in 1987, the Dow closed at 1,738.74. It was just recently that the Dow Jones surpassed 36,500. That’s a 20-fold increase since then, on a price-only basis. Some may not like these so-called government-managed markets because the game has changed for them (and maybe it isn’t fair to some professionals), but it’s hard to say that such markets are not effective in growing retirement savings.

And to put it bluntly, do savers really care that the game is rigged in their favor? Of course not. They love it. If they can index, and the government can bail them out as in the airlines, for example, why should investors pay attention. The government is delivering on all the unintended uses of the stock market, and the tax-payer is picking up the tab when things go wrong. This is the quintessential definition of moral hazard, but again, this is what the markets have become.

With this said, what type of markets should we expect going forward?

It is my opinion that we now live in a world where bull markets will continue to be prolonged, as they have been, but bear markets will be but a blink of an eye. Throughout history, the average bull market has lasted 4.4 years while the average bear market about 11 months. This is data from First Trust. The COVID-19 bear market, however, was just a little over one month. One month! -- while the preceding bull market was 11 years! I see more of the same.

Future bull markets will continue to be long in duration, as they have been throughout history, while future stock market drawdowns, in my opinion, will continue to be deep but much shorter in duration--almost too brief to even impact sequence of returns risk within traditional financial planning models. Information flow and expectations revisions are so swift these days that policy decisions can almost negate, or significantly mitigate, the next bear market before it even starts.

Case in point is the COVID-19 meltdown. Largely through Fed and Treasury intervention, the markets had recovered from the March 2020 lows to new highs again by August. We’re not talking about a modest retracement off the bottom, but brand-new highs in the market in a matter of five months--in a type of crisis we hadn’t witnessed since the Spanish Flu over a hundred years ago. Let me repeat: It took the stock market but five months to recover from the worst health crisis in over a century!

The Fed and Treasury have become the ultimate trump cards. The Greenspan put. The Bernanke put. And now the Powell put.

With government officials that have the tools to flood the markets with trillions in liquidity, nationalize the banks, buy investment-grade bonds, and perhaps even some day buy common stock, if they ever need to, it’s very, very hard for things to go wrong. We’ve seen the worst financial crisis since the Great Depression in the Great Financial Crisis, and we’ve seen the worst health crisis since the Spanish Flu in COVID, and the markets still have prevailed.

Not only prevailed, but soared.

The markets, in my view, are rigged in favor of the long-term investor, not rigged against the investor. The American people and their representatives in Congress have far too much skin in the game to risk catastrophe in the long run, and there are far too many tools at the Fed's and Treasury’s disposal to passively let the train go off the tracks.

Okay, so what does all this mean?

Well, in spite of all of this, it shouldn’t change one’s approach to investing much, if at all. It’s not changing ours. The largest indexes today continue to be dominated by the largest stocks, and that’s where we think the implicit backing rests and an asymmetric risk/reward resides.

The Fed and Treasury don’t care much about a languishing Russell 2000 index when trillion-dollar companies dominate retirement accounts these days. This is why it shouldn’t be too surprising that we’ve seen a junk-tech crash during 2021, despite no indication that tapering will be stopped--all the while we still have a very attractive 10-year Treasury rate (which should have helped those long-duration small cap names).

There’s simply no implicit backing behind the smaller names. They represent risk in the purest sense – risk as it once was -- and that’s why many ultra-speculative investors have been demolished during 2021. The Fed doesn’t care about these speculative names, and asymmetric rewards aren’t as prevalent. Pick your stocks wisely.

Let’s now take it down a notch.

Being prudent and diversified with stock selection shouldn’t change as a result of implicit government support, and sensible financial planning shouldn’t change much either. However, the financial planning profession may need to rethink some of its old ways, especially if bear markets grow briefer in nature, as I think they will. More exposure to risk assets could make a lot of sense for many more types of investors, as drawdowns become shorter in duration.

Here’s an example. Those that took a standard annual withdrawal in retirement in early 2020 and the next one a year later in early 2021, not much happened from their perspective. In fact, they may not have felt the impact of COVID-19 on their withdrawal targets at all. For starters, the markets had already recovered to new highs by early 2021. It’s my view that investors worrying too much about drawdowns could be leaving a considerable amount of return on the table.

With all this background, what do we like?

Well, we continue to like the area of large cap growth, which has dominated small cap value in recent years and most all asset allocation models, namely the standard 60%/40% stock/bond allocation. But it’s important to understand why we like this area.

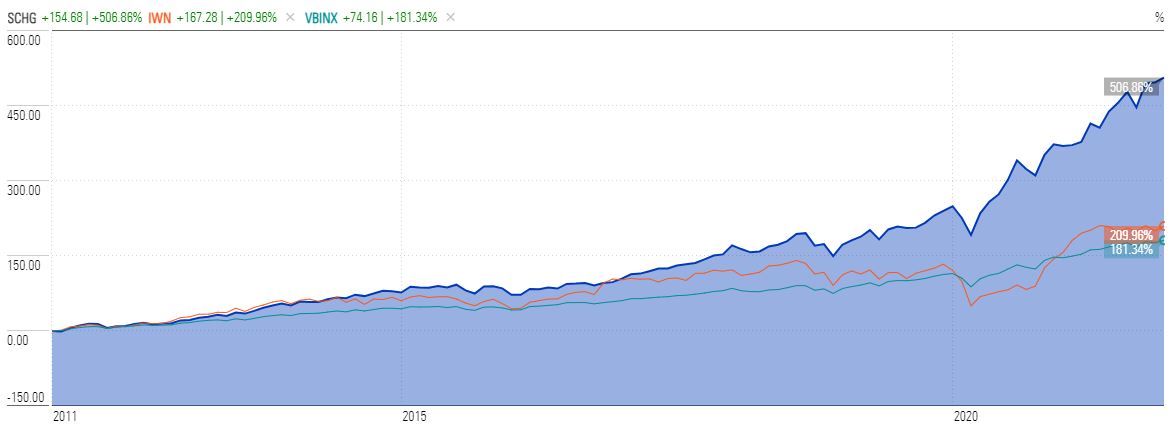

Image: Prudent and diversified stock selection among the largest, strongest, most well-known large cap growth equities (SCHG, blue fill) has outperformed exposure to the two most widely-accepted quantitative explanatory factors to stock returns, small cap value (IWN, orange line), and the most widely-accepted standard asset allocation model, the Vanguard Balanced 60% stock/40% bond (VBINX, turquoise), by nearly 300 percentage points and approximately 325 percentage points, respectively, during the past 10 years. Image Source: Morningstar.

It’s not because of its strong track record the past decade-plus, but rather because most constituents are moaty, net cash rich, secular growing, free-cash-flow generating powerhouses. It is simply amazing that we continue to see companies such as Meta Platforms, formerly Facebook, and Alphabet trading at substantial discounts to their intrinsic value estimates, even in an environment where the Fed put has prevailed time and time again (across decades).

Large cap growth is overflowing with companies that have considerable cash-based sources of intrinsic value: net cash on the balance sheet and future expected free cash flow. We mentioned that we’re huge fans of the likes of Meta Platforms and Alphabet, but ideas like this are scattered among the top considerations in this area. Apple, Microsoft, and the list goes on and on--again among some of the larger players.

That said, not all ideas of this sort are cut and dry. My colleague Callum Turcan makes an important point:

Not all firms that represent high-quality opportunities for investors will have net cash positions. It’s just one part of the value equation – the other being future expected free cash flow. There are plenty of solid companies out there with manageable net debt loads, too, including ones that we’ve highlighted in the Exclusive publication as well as the High Yield Dividend Newsletter portfolio.

If our ideas do have net debt positions in certain cases, however, we prefer that they have solid free cash flow generation, pricing power and excellent corporate credit ratings. Overleveraged companies often experience the worst amount of pain during downturns and crises, and we want to avoid that entirely if we can.

Now, what may change our bullish stance?

Not traditional inflation measures, which counterintuitively are positive for nominal equity prices as nominal future free cash flows advance.

Not even the omicron variant.

But rather – [we're watching closely] the discount rate, namely the 10-year Treasury, which is used as the benchmark rate for bond pricing and within most equity valuation models. At 1.46%, however the 10-year Treasury rate is well off its highs this year, and this tells me stocks can still go higher. We’re having a hard time not being bullish on stocks for the long run.

Everybody is worried about prices at the gas pump, so let’s now talk about energy resource prices.

Years of subdued levels of capital investments on upstream projects, the kind involved in extracting raw energy resources from the ground, combined with the sharp rebound in energy demand seen of late has resulted in oil & gas prices surging higher over the past year. We expect this dynamic will continue into the new year.

Oil prices have also been driven higher in part by the coordinated activities of the OPEC+ cartel limiting global supplies through a program enacted last year, and in part due to the ongoing recovery in petroleum products demand as households and businesses slowly return to pre-pandemic activities. Gasoline and diesel consumption levels have largely recovered from the pandemic, though it will take a while longer for demand for jet fuel to recover, with an eye towards variants of COVID-19 weighing negatively on international travel demand.

Natural gas prices have boomed higher since January 2021 as the global industrial economy staged a robust recovery from the worst of the pandemic, driving up demand for gas-powered electricity and natural gas feedstocks. Near term liquefied natural gas deliveries to Europe and East Asia are now incredibly expensive at a time when many households in these regions, and elsewhere, are turning to natural gas to meet their heating needs this winter. Geopolitical concerns are also at play.

Subdued levels of capital investments on upstream oil & gas projects since the middle of the 2010s decade has resulted in the world increasingly relying on production from mature fields that are in decline at a time when demand for energy is robust and will likely continue to grow going forward. We expect raw energy resources pricing to remain elevated throughout 2022. Furthermore, we do not see the recently announced and relatively modest releases of emerging oil stockpiles from a handful of nations, including the US, as fundamentally altering this dynamic.

US oil production remains well below levels seen before the pandemic hit, and it will take a long time to recover that lost ground, a process made all the more difficult due to labor shortages and rising oilfield services costs. Domestic oil production growth going forward is unlikely to match the levels of growth seen in the years preceding the COVID-19 pandemic, in our view, especially as plenty of the most prolific well locations have already been developed. The US is still loaded with oil & gas supplies, but those incremental barrels will be more expensive to extract.

In summary, there is not a lot that we’re concerned about these days – we think you should stay safe when it comes to your health and the omicron variant, but we don’t think it will impact markets much.

We’re viewing inflation in a positive way, provided that interest rates (especially the 10-year Treasury rate) remain subdued, and we continue to like stocks for the long haul--and large cap growth in particular.

We’re pleased with the performance of the newsletter portfolios across the board, and we’re very happy with the success rates of ideas in the Exclusive publication.

With that being said, let’s answer a few previously submitted questions from members.

First question.

If you had to choose a single technical indicator to help you make entry/exit decisions for a stock (that was under/overvalued), what would you choose?

On the plus side, we think by far the most powerful technical indicator is the breakout from the downtrend of an undervalued stock. Meta Platforms, formerly Facebook, is approaching this sweet spot as we speak. Other areas include a breakout of the traditional cup-and-handle.

What gets us concerned, as it relates to technical downside, is if we have a stock that has an elevated net debt position, mature growth and is stalling a bit in terms of strategy.

If its shares start to roll over (break through support), we take notice. AT&T was one example where even though we thought shares were cheap, we removed it from the High Yield Dividend Newsletter portfolio in the process of its technical breakdown.

Our consider buying discipline is based more on undervalued ideas that are breaking out of downtrends, while our consider selling discipline is more fundamentally weighted with an eye toward the balance sheet and technical breakdowns.

There is a lot more that goes into both aspects, of course, but this hits on the high points that we’re looking at from a technical standpoint. We combine both qualitative and quantitative analysis in our work.

Second question.

When you highlight capital appreciation and equity income ideas in the monthly Exclusive, why do you not include a DCF valuation and a comparison to the closest comparative peer companies? Thanks for all the great work.

We’ve had a tremendous amount of success with the DCF process on the Valuentum website, but we’ve found that many Exclusive members love the format of the existing letter.

That said, we often comment extensively on the valuation considerations of ideas highlighted, and we plan to do more and more of this going forward. You shouldn’t be surprised if we start adding more DCF-related content, and even attach a model in future editions.

As it relates to relative valuation, these are areas we pay attention to, but in this particular market, we think it very important to use the DCF as the baseline, as relative valuation could lead to a whole industry to become detached from a reasonable valuation.

The Exclusive ideas can take on a variety of different approaches from catalyst-driven to valuation driven and beyond, so the format is one of free-form that many of our members enjoy.

Third question.

You made an excellent call several years ago to be bearish on MLPs. Are they still uninvestible?

We’re still very cautious on the MLPs because their business models tend to be very net debt heavy, and many have a difficult time covering cash distributions paid with traditional free cash flow.

That said, many have moved toward greater transparency in recent years and have now been disclosing measures of free cash flow in their press releases, a huge step in the right direction.

We include a couple energy pipeline MLPs in the High Yield Dividend Newsletter portfolio, but the area is not our favorite. Our favorite area to look for new ideas continues to be in the strongest area of large cap growth.

For those that asked questions about a particular Exclusive idea, please expect a response in the next edition of the Exclusive newsletter, to be released Saturday, January 8.

This concludes the Valuentum Exclusive call for 2021. Thank you for your attention and your membership.

----------

Tickerized for the SPY.

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Brian Nelson owns shares in SPY, SCHG, QQQ, DIA, VOT, BITO, and IWM. Valuentum owns SPY, SCHG, QQQ, VOO, and DIA. Brian Nelson's household owns shares in HON, DIS, HAS, NKE. Some of the other securities written about in this article may be included in Valuentum's simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

0 Comments Posted Leave a comment