ALERT: Replacing Qualcomm with McDonald’s in Dividend Growth Newsletter Portfolio

Image: The semiconductor space is experiencing a number of headwinds, and while we still like Qualcomm’s long-term prospects, we’re replacing it with McDonald’s in the simulated Dividend Growth Newsletter portfolio. Image Source: Qualcomm

By Brian Nelson, CFA

The technology industry has been wrecked during 2022, and the semiconductor space has been no exception. The VanEck Semiconductor ETF (SMH) is down ~41% so far this year, as many of its top holdings, including wireless technology giant Qualcomm (QCOM) languish. As we walk through our views in this work, please note that Qualcomm’s fiscal third-quarter 2022 is calendar second quarter and its fiscal fourth-quarter 2022 is calendar third quarter.

We recently highlighted our expectations for near-term weakness across the semiconductor space in this note here, and Qualcomm’s fourth-quarter report for fiscal 2022 for the period ending September 25, released November 2, all but confirmed our incrementally negative take on the space. As with many tech stocks, we were bullish in early 2022, as signs indicated that things were going well through the calendar first quarter, but things changed rapidly during the summer.

Qualcomm got caught in the mix, with the firm offering reduced guidance for its fiscal 2022 fourth-quarter (calendar third quarter, now just reported) in late July. In its third-quarter fiscal 2022 (calendar second quarter, reported in late July), Qualcomm recorded earnings per share that exceeded the high end of its guidance range with impressive 50%+ year-over-year growth. However, management warned on that conference call about the company’s fiscal fourth quarter (calendar third quarter, now just reported) at the time:

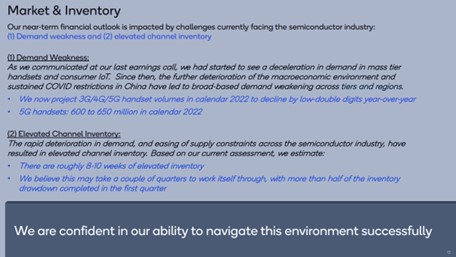

From July 2022: Looking forward to global 3G, 4G, 5G handset forecast. We now expect calendar ‘22 global handsets to decrease by mid-single-digit percentage on a year-over-year basis, including 650 million to 700 million 5G handsets. Our guidance reflects the continuation of the trends that adversely impacted handset volumes exiting the June quarter.

We expect the elevated uncertainty in the global economy and the impact of COVID measures in China will cause customers to act with caution in managing their purchases in the second half of calendar ‘22.

In the fourth fiscal quarter, we are forecasting revenues of $11 billion to $11.8 billion and non-GAAP EPS of $3 to $3.30. The midpoint of our guidance includes an estimated impact of approximately $0.20 due to the macroeconomic headwinds and the reduction in the global handset forecast.

Fast forward now to November 2, and Qualcomm’s fiscal fourth-quarter 2022 results (calendar third quarter), and we’re seeing an acceleration of the weakness at Qualcomm that the firm had noted in July. During its fiscal fourth quarter 2022 results, Qualcomm’s non-GAAP revenue advanced 22%, while non-GAAP diluted earnings per share growth came in at 23%. No doubt these are fantastic growth rates by themselves, but they are a slowdown from the company’s annualized pace of non-GAAP top-line expansion of 32% and non-GAAP diluted earnings per share of 47% during fiscal 2022 (ending September 25, 2022).

Qualcomm management’s commentary in its fiscal fourth-quarter 2022 press release wasn’t great – please compare this November commentary to the commentary from July above:

From November 2022: Given the uncertainty caused by the macroeconomic environment, we are updating our guidance for calendar year 2022 3G/4G/5G handset volumes from a year-over-year mid-single-digit percentage decline, to a low double-digit percentage decline. The rapid deterioration in demand and easing of supply constraints across the semiconductor industry have resulted in elevated channel inventory. Due to these elevated levels, our largest customers are now drawing down on their inventory, negatively impacting the mid-point of our EPS guidance for the first quarter of fiscal 2023 by approximately ($0.80). This is the primary driver of the variance relative to our prior expectations.

Today, in the Dividend Growth Newsletter portfolio, we’ll be replacing Qualcomm with McDonald’s (MCD), which we think is much better positioned to deal with the current economic malaise given its mostly-franchised business model, its ability to reap higher fees from higher revenue due to inflation, the company’s tremendous value offering to consumers, and the idea that even affluent customers are trading down to fast-casual and quick-service from fine-dining during the current economic climate. McDonald’s was recently added to the Best Ideas Newsletter portfolio, and the change to the Dividend Growth Newsletter portfolio will be reflected in the next edition of the Dividend Growth Newsletter.

Concluding Thoughts

We’re huge fans of Qualcomm’s business model over the long haul, but risks continue to add up. First, the adjustment in the pace of Qualcomm’s expectations for handset volumes for calendar 2022 is rather concerning, given the delta from its commentary in July and over a period of what is only a couple months remaining this year. In light of U.S.-China geopolitical tensions, new export restrictions on chip technology to China (announced October 7) that are further complicating industry matters, and Qualcomm customers retrenching by drawing down on their inventory, we’re going to remove the small “position” in Qualcomm in the simulated Dividend Growth Newsletter portfolio. McDonald’s will be taking its place in the portfolio. This change will be reflected in the next edition of the Dividend Growth Newsletter.

Tickerized for holdings in the SMH.

---------------------------------------------

About Our Name

But how, you will ask, does one decide what [stocks are] "attractive"? Most analysts feel they must choose between two approaches customarily thought to be in opposition: "value" and "growth,"...We view that as fuzzy thinking...Growth is always a component of value [and] the very term "value investing" is redundant.

-- Warren Buffett, Berkshire Hathaway annual report, 1992

At Valuentum, we take Buffett's thoughts one step further. We think the best opportunities arise from an understanding of a variety of investing disciplines in order to identify the most attractive stocks at any given time. Valuentum therefore analyzes each stock across a wide spectrum of philosophies, from deep value through momentum investing. And a combination of the two approaches found on each side of the spectrum (value/momentum) in a name couldn't be more representative of what our analysts do here; hence, we're called Valuentum.

---------------------------------------------

Brian Nelson owns shares in SPY, SCHG, QQQ, DIA, VOT, BITO, and IWM. Valuentum owns SPY, SCHG, QQQ, VOO, and DIA. Brian Nelson's household owns shares in HON, DIS, HAS, NKE. Some of the other securities written about in this article may be included in Valuentum's simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

0 Comments Posted Leave a comment