Boeing’s Financials Are Absolutely Frightening

By Brian Nelson, CFA

On November 18, 2020, Boeing (BA) announced that the US Federal Aviation Administration (FAA) withdrew its order that had grounded its 737-8s and 737-9s (737 MAX) that had been involved in two terrible accidents during the past few years, a Lion Air flight that killed 189 people and an Ethiopian Airlines jet crash that claimed the lives of 157 more. We’ll never forget these tragedies and the impact on the families and the aviation industry, more generally.

In January 2017, we had added Boeing to the Dividend Growth Newsletter portfolio, but we had removed it March 16, 2018, prior to the unfortunate and high-profile accidents that occurred several months after. During the short time it was in the newsletter portfolio, the stock roughly doubled, producing a return 5 times that of the S&P 500’s performance. Here was the rationale for the removal at the time (bear in mind that this was before the terrible tragedies that occurred months later):

The primary reasons for the removal rest in a combination of Boeing’s value and technical/momentum considerations. Shares have soared to the high end of our fair value range, and now technically, they have started to roll over as investors, fair or not, worry about retaliation with respect to coming tariffs. We’re huge fans of Boeing on a fundamental basis, but a great company a great stock doesn’t always make.

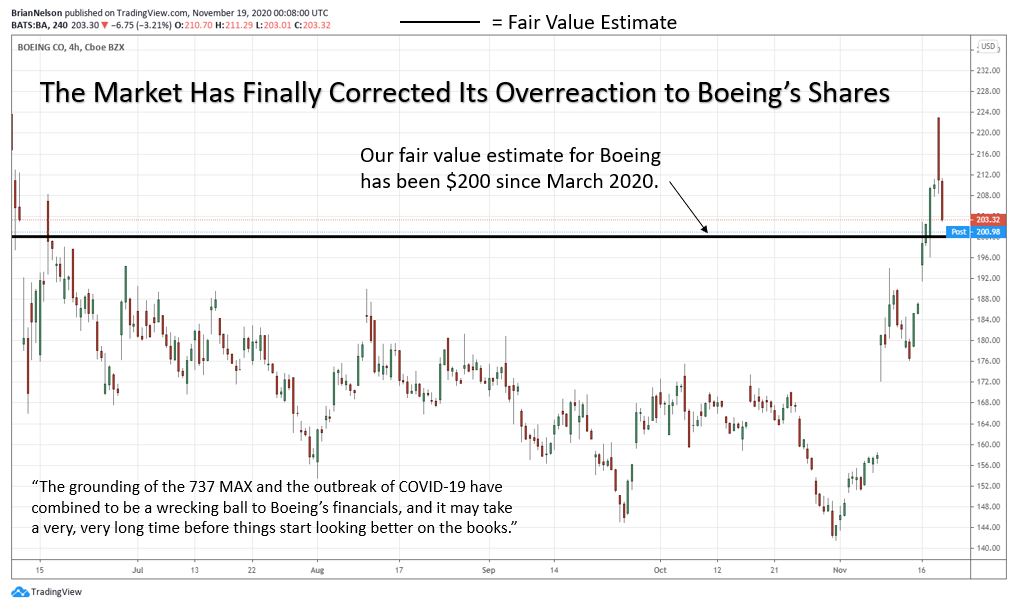

Fast forward to January 23, 2020--a month or so before the COVID-19 market collapse--when Boeing’s shares were trading at ~$320 per share, I penned a piece in frustration: “Why *NOW* Do You Care About Boeing’s Stock?” I said in that January 23, 2020 note in no uncertain terms: “In no, way shape or form should you *now* be interested in Boeing’s stock.” There was some more harsh writing in the note, and I wish I could have said it nicer – but at times, I just want our members to get a feel for exactly what we think about a stock. There’s always room for improvement in my tone.

But please let me put it nicely now: I really didn’t like Boeing’s shares at $320 in January 2020, especially since we had removed them from the Dividend Growth Newsletter portfolio for a huge win just a number of months prior. Now with the benefit of hindsight, I hope you can forgive me for that emphatic and colorful note (in analyst speak, we call that type of writing “pounding the table”). Boeing’s shares had fallen from ~$320 that day in January 2020, to a 52-week low of $89 per share in mid-March.

But that was then, and this is now. Shares of Boeing have finally bounced back, converging to our fair value estimate of $200 that we established near the depths of the COVID-19 meltdown. The company’s shares had rallied back to those levels in June of this year, and now they have settled again at our fair value estimate after technically basing for a number of months. We’re viewing this share price move, in particular, positively, but Boeing still has a long way to go to meet the fundamental/financial criteria we’re looking for to be reconsidered in any newsletter portfolio.

The reality is that Boeing’s financials are still pretty scary. During the first nine months of 2020, the company burned through an incredible $15.4 billion in free cash flow, even as it cut capital spending by a few hundred million. As of the end of the third quarter of 2020, its total consolidated debt now stands at $61 billion, with total cash and marketable securities of $27.1 billion. This compares to total consolidated debt of $24.7 billion and total cash and marketable securities of $10.9 billion, as of the end of the third quarter of 2019.

The grounding of the 737 MAX and the outbreak of COVID-19 have combined to be an absolute wrecking ball to Boeing’s financials, and it may take a very, very long time before things start looking better on the books. S&P, Moody’s and Fitch still give the company investment-grade credit ratings (BBB-/Baa2/BBB-), but we’re not sure the aerospace giant deserves them. Here’s what Fitch noted October 2020: “…many of the company's quantitative rating factors will be inconsistent with the 'BBB' category for three years (2019-2021) and into 2022.” It’s probably fair to say that Boeing’s corporate debt should be rated junk, but that would cause some severe reverberations in the credit markets, in our view.

It's worth sharing Fitch's views on expectations for airline traffic in coming years:

Fitch's base case for airline passenger traffic (domestic and international) assumes revenue passenger kilometers (RPKs) will not recover to 2019 levels before FYE23 and at FYE21 will still be 30% below 2019 levels. Underlying this forecast is the assumption that an effective vaccine/treatment is available, but not at scale, through 2021, and there will be a continued collapse in travel until there is widespread vaccine/treatment availability.

Our base case assumes domestic traffic recovers to 2019 levels around the middle of 2023, while international traffic returns to 2019 levels after 2023, perhaps the summer of 2024. Available information so far supports this assumption of domestic recovering first, including the data coming out of the important Chinese domestic market. We expect capacity will recover before RPKs, and we believe load factors will remain lower than the record levels seen in 2019 (source).

Here is what the International Air Transport Association (IATA) had to say about the 5-year outlook for air passenger demand (July 2020):

…we have revised down our passenger forecast over the next five-year period. In our new forecasts, we expect RPKs to decline by a little more than 60% in 2020 compared to 2019, with a return to pre -COVID levels not occurring before 2024. Many uncertainties remain around the outlook and in this update we have investigated various possible future scenarios. The main point is that the risks around our latest forecast remain clearly tilted to the downside...The upside could see travel demand return to 2019 levels in 2023, while the downside could be much more severe (source).

The airlines are certainly not over the hump, by any stretch, and we think the credit rating agencies are probably giving Boeing the benefit of the doubt that it will start raking in material free cash flow in 2022 due to pent-up demand and accelerated deliveries (an optimistic, but still an assumption with reasonable basis). However, as we’ve learned time and time again, supply chain issues can pose problems, and lower airline traffic will almost certainly impact its services operations.

In the longer run, new aircraft are extremely expensive to build and come with substantial “unknown” risks (e.g. think 787 delays, the recent 737 MAX incidents), and key rival Airbus (EADSY) is not backing down either, with competition only intensifying as the duo vie for orders during these troubled times (Boeing hasn’t had a new aircraft order since August). It's only a matter of time before China and Russia will be key players in the aircraft-making industry, too. Boeing has no margin of error left; should it be hit with another negative exogenous event in the near term, things could get really, really ugly for shares.

When it comes to our favorite ideas, we continue to prefer net-cash-rich, free cash flow generating powerhouses with strong competitive advantages that facilitate recurring revenue business models that can take advantage of secular tailwinds (see the concentrated nature of the Best Ideas Newsletter portfolio). With Boeing’s dividend suspended, too, there’s simply no place in any of our newsletter portfolios for this troubled airframe maker, despite a hugely attractive backlog of unfulfilled deliveries ($393 billion, ~4,300 commercial airplanes). The company falls within what we'd describe as the “too hard bucket,” in our view. One day--many years from now--the aerospace giant’s financials may return to some “normalcy,” but until then, Boeing is likely dead money with a severely-bloated balance sheet walking on thin ice.

---

Related aerospace: ITA, PPA, XAR, SPR, TGI, HXL, HWM, HEI, TDG, RX, DCO, BAESY, EADSF, SAFRY, CAE, BDRAF, BDRBF, ITT, ATRO, CSTM, DCO, MOG.A, WWD, KAMN, HON, TXT, AVAV, LHX, AIR, ERJ, RYCEF, RYCEY

Related airlines: JETS, ALK, LUV, AAL, ACDVF, DAL, UAL, HA, SAVE, GOL, CPA, RYAAY, AZUL, ICAGY, EJTTF, DLAKF, DLAKY, AFRAF, DRTGF, WZZAF, AERZY, FNNNF, NWARF, AIBEF, QUBSF, ESYJY, LTM, SKYW, MESA, ANZFF, CEA, ZNH, AIRYY, ALGT, KLMR, JAPSY

Related lessors: AL, AER, GE

Related travel stocks: TCOM, TRVG, BKNG, EXPE, TRIP, TZOO, CTRP, DESP, SABR

Related air freight: UPS, FDX

Related country ETFs: FXI, MCHI, RSX

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Brian Nelson owns shares in SPY, SCHG, DIA, VOT, and QQQ. Some of the other securities written about in this article may be included in Valuentum's simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

0 Comments Posted Leave a comment