Stock Markets Still Healthy, Big Cap Tech and Large Cap Growth Safe Havens

Image Shown: The S&P 500 has been trading above our fair value estimate range (shaded blue area) for some time now. A modest sell-off should be expected. We continue to be bullish on equities for the long run and point to the areas of big cap tech and large cap growth as sources of fundamental and financial resiliency.

By Brian Nelson, CFA

The S&P 500 (SPY), chart shown above, is trading above our fair value estimate range. The recent sell-off should not be surprising, and it has been predominant in speculative free-cash-flow burning technology stocks, of which we tend to avoid. In January of this year, we “raised” 10%-20% cash in the Best Ideas Newsletter portfolio and Dividend Growth Newsletter portfolio, “ALERT: Raising Cash in the Newsletter Portfolios” on account of expectations of a pullback to put some new money “to work,” where applicable. We’re not making any moves quite yet.

In January, we had grown concerned about price distortions caused by price-agnostic trading (i.e. trading not focused on free-cash-flow based intrinsic value calculations). For example, a stock market where GameStop (GME) can trade at $180 per share and $350 per share on the same day with no news is one where prices have the potential to become distorted in even larger names. At the time, we just wanted to be a bit more cautious under such conditions, and the decision is now bearing fruit as others are seemingly starting to panic sell. Valuations matter.

Not much has changed with respect to our concerns about price-agnostic trading, as we outlined in the book Value Trap many moons ago now. Index fund-driven distortions, the meme stock frenzy, and the crypto craze have been a few examples. Even today, a cryptocurrency that started out as a joke (Dogecoin) still has a market capitalization in the tens of billions as of this writing, even after Elon Musk’s skit on Saturday Night Live that called it a “hustle.” We think it still makes sense to have dry powder ready for potential opportunities.

There may be other contributing factors to the sell-off, too--other than rising inflation expectations. From what we can tell, many speculators have been able to lever up multiple times to gain exposure to cryptocurrencies, and such deleveraging from the Dogecoin route may also be impacting some of the aggressive growth free-cash-flow burning equities, causing outflows in speculative instruments such as the ARK Innovation ETF (ARKK). This, in turn, may be driving even more deleveraging in some stronger names. All of this just has to work through the system, in our view.

Where Are We Focused?

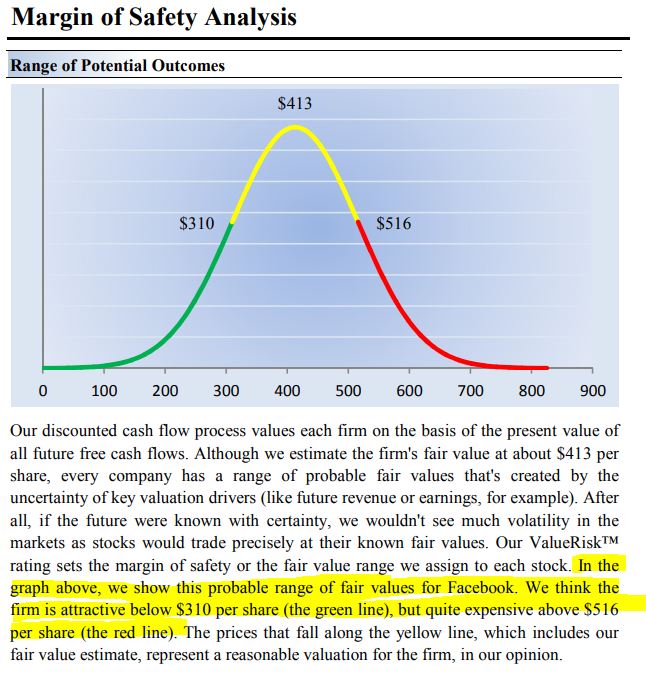

Image Shown: Facebook’s shares are trading below the low end of our fair value estimate range at the time of this writing. The social media giant registers a 10 on the Valuentum Buying Index as it boasts a tremendous financial position with respect to net cash on the balance sheet and future expected free cash flows. Image Source: Valuentum.

We’re sticking with the highest quality, net-cash rich, free-cash-flow generating powerhouses. Our top idea continues to be Facebook (FB). Based on consensus expectations, the company is expected to grow revenue 35% and 19% during 2021 and 2022, respectively, driving EPS of $13.14 and $15.23 over the next two years. Backing out Facebook’s $64.2 billion net cash position at the end of the first quarter, it’s trading at just ~18.5x 2022 earnings expectations. Facebook has a huge moat, a firm financial foundation, and grew revenue 48% in the first quarter. The market may be frothy in certain areas, but it is not frothy in the stronger areas of big cap tech and large cap growth.

From our perspective, the anecdote of Facebook being lumped into a basket of names that have weak competitive positions and that are burning through free cash flow tells us the current sell-off might just be the market taking a breather. We expect big cap tech (and large cap growth) to remain resilient, and while others rotate into banks, energy, and metals and mining, we’re sticking with high quality, net-cash-rich, free-cash-flow supported entities. Our fair value estimate for Facebook stands at $413 per share (~26x 2022 earnings, excluding cash), and there may be more upside to our fair value estimate based on new initiatives Facebook has in its pipeline, the cost levers the company has available to pull, and the option value of net cash just sitting on its books. Share buybacks, in Facebook’s case, are value creating.

The markets may not be done with the sell-off quite yet, and we continue to be active while patient. Once we start to see signs of technical support, we’d be looking to “add” to the areas of big cap tech and large cap growth. For those seeking commodity-driven exposure, we continue to like Newmont Mining (NEM), and for those looking to participate in the rotation into energy and financials, we prefer broad-based ETFs such as the Energy Select Sector SPDR (XLE) and Financial Select Sector SPDR (XLF). An idea in the Best Ideas Newsletter portfolio, Berkshire Hathaway (BRK.A) (BRK.B) is also the top weighting in the XLF.

For investors seeking equity exposure higher up the dividend-yield chain, AT&T (T) may be a solid consideration, a stock of which we may look to increase our “weighting” within the High Yield Dividend Newsletter portfolio and add new to the Dividend Growth Newsletter portfolio to bolster the forward estimated dividend yield of the latter portfolio to better offset a potentially higher cost of living. We don’t like AT&T's net debt position, but the company handily covers cash dividends paid with traditional free cash flow. Management is also laser-focused on paying down debt. AT&T may be in the early innings of a financial transformation.

Concluding Thoughts

It’s easy to get spooked sometimes by the market’s volatility, but what we’ve witnessed the past few days is nothing compared to the volatility during the COVID-19 crisis and the Great Financial Crisis before it—and what we eventually expect the proliferation of price-agnostic trading to do to the markets in the years ahead.

We continue to like the areas of big cap tech and large cap growth thanks to their strong competitive positions, solid net cash profiles, and robust and growing future expected free cash flow. Facebook remains our top idea for capital appreciation potential.

Newmont Mining is our favorite “inflation hedge” within the metals and mining arena, and investors that would like greater exposure to energy and financials may look to more diversified ETFs to gain access to the broader themes of rising energy resource prices and net interest margins. AT&T is a top equity consideration for the high-yield dividend crowd.

In the coming weeks and months, we’ll be looking to put some of the dry powder we raised in January “to work” in some of the areas we outlined in this article. In the meantime, we’re going to continue to watch this orderly sell-off that’s being driven by valuation model adjustments (to factor in higher inflation expectations) and modest deleveraging from cryptocurrency volatility.

All is well.

Downloads

Facebook's 16-page Stock Report (pdf) >>

Related electric-vehicle stocks: TSLA, NIO, LI, FSR, RIDE, WKHS, RMO, QS, SOLO, HYLN, BLNK, GOEV, XPEV

Related cryptocurrency securities: PYPL, SQ, GBTC, RIOT, OBTC, MSTR, SOS, OSTK

-----

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Brian Nelson owns shares in SPY, SCHG, QQQ, DIA, VOT, and IWM. Brian Nelson's household owns shares in HON, DIS, HAS. Some of the other securities written about in this article may be included in Valuentum's simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

0 Comments Posted Leave a comment