Meta’s Free Cash Flow Generation Has Returned, But TikTok Has Permanently Changed the Competitive Landscape

Image: Meta Platforms’ free cash flow has bounced back a bit, but the firm’s top-line growth remains challenged as it transitions away from a secular growth powerhouse into a cyclical story with encroaching competition. Image Source: Meta Platforms

By Brian Nelson, CFA

As we outlined in our introductory note in the February edition of the Dividend Growth Newsletter (pdf), the Federal Reserve is slowing its pace of benchmark rate increases as signs of inflation start to slow. Though there may still be pockets of input cost pressures, particularly with respect to prices at the pump and food-at-home expenses, for the most part, the negative wealth effect from falling asset prices around the globe is successfully working itself through the system.

There are three reasons to be optimistic about equity prices: 1) the pace of inflation has likely peaked in June 2022, and this has increased investor risk appetite, 2) fourth-quarter earnings season, while mixed, has been coming in better-than-feared, and 3) we’ve witnessed impressive technical breakouts of the equal-weight S&P 500 (RSP), market-cap weighted S&P 500 (SPY), and the triple-Q’s (QQQ), which heavily weight some of out favorite tech names. These breakouts have had strong follow-throughs as well.

On the back of strong fundamental performance from Tesla (TSLA) and more expected capital-spending discipline from Meta Platforms (META), we continue to believe large cap growth remains the favored stylistic area for long-term investors, and we are hugely skeptical of the foundation of empirical quantitative research based on realized historical data, “What So-Called Statistical ‘Value Premium?” We talked about several earnings reports in our January 26 note, “Market-Cap Weighted S&P 500 Breaks Out; Have We Already Seen the Bottom?,” and here are some more big developments from fourth-quarter 2022 earnings season.

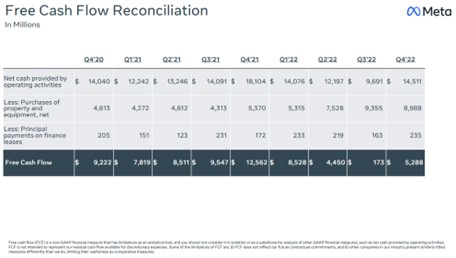

- Meta Platforms, Inc. reported terrible fourth-quarter 2022 results, with revenue falling 4.5% on a year-over-year basis and its non-GAAP earnings per share missing the consensus estimate considerably. However, the company’s free cash flow generation meaningfully returned, CEO Mark Zuckerberg noted that Meta would spend less on the metaverse, and the board announced a $40 billion stock buyback. We expect to increase our fair value estimate of Meta on the news, but we won’t be adding it back to the Best Ideas Newsletter portfolio. No longer is Meta a secular growth story, in our view, and encroaching competition from TikTok and potentially others has changed its competitive profile.

- Dividend Growth Newsletter portfolio holding Honeywell International (HON) reported mixed fourth-quarter 2022 results. Revenue for the period came in slightly lower than expected, but we can’t be disappointed in the firm’s strong backlog, which came in at $29.6 billion at the end of the year, up 7%, thanks to strength in its late cycle aerospace and energy markets. The company generated $5.3 billion in operating cash flow during the year and free cash flow of $4.9 billion, both measures down from last year, but still well in excess of cash dividends paid of ~$2.7 billion. Full-year 2023 sales guidance calls for organic growth of 2%-5%, adjusted earnings of $8.80-$9.20, and free cash flow in the range of $5.1-$5.5 billion, excluding certain one-time settlements (NARCO buyout, HWI Sale, and UPO Matters).

- Altria Group’s (MO) fourth-quarter 2022 results were about as expected, with revenue, net of excise taxes, falling modestly, and adjusted earnings per share advancing 8.3%. Though performance held up in the period, the company’s domestic cigarette shipment volume fell 12.1% in the quarter with the firm saying continued industry weakness and retail share losses were to blame. Sticks sold of Marlboro during the fourth quarter fell to 17.6 billion from 19.85 billion, down 11.3%. Shipped cans of Copenhagen and Skoal dropped 8.9% and 12%, respectively during the final period of 2022. We continue to monitor Altria’s efforts to transition to a smoke-free and less harmful product provider, and in the meantime, investors are getting paid a nice dividend. 2023 adjusted diluted earnings per share is targeted in the range of $4.98-$5.13, and management seeks to pay out ~80% of that as a dividend for the year.

- Advanced Micro Devices, Inc. (AMD) assuaged concerns across the semiconductor industry by putting up rather strong fourth-quarter results in the wake of Intel’s (INTC) disaster of a fourth-quarter report. AMD’s fourth-quarter revenue advanced 16% on a year-over-year basis, and while operating income and earnings per share faced pressure in the quarter, we were highly encouraged by the top-line resilience given Intel’s shocking weakness. We like AMD’s positioning to gain share, are huge fans of its strategic acquisition of free-cash-flow rich Xilinx, and believe the firm is much better able to handle a weakened PC market than rivals. For full-year 2022, AMD hauled in $3.1 billion in free cash flow and ended the year with a strong $3.4 billion position in net cash. Intel’s financial situation is the opposite—the chipmaker is burning through cash and holds a massive net debt position, all the while it is struggling to continue to pay too-large of a payout.

Concluding Thoughts

We’re loving this nice move higher in the stylistic area of large cap growth, and for those investors seeking broad-based exposure, we think this area is the place to be in the long run. Tesla’s strong financial performance coupled with Meta Platforms’ return to financial discipline are propelling large cap growth higher, but risks to the broader equity markets and economy remain. In any case, with inflation likely peaking in June 2022, fourth-quarter 2022 earnings season coming in better-than-feared, and technical breakouts of key indices across the board from the equal-weighted and market-cap weighted S&P 500 to the NASDAQ-100, equity investors have a lot to cheer about.

Tickerized for RSP, SPY, QQQ, TSLA, META, FB, HON, MO, AMD, INTC, SCHG

NOW READ: What So-Called Statistical “Value Premium?”

----------

Brian Nelson owns shares in SPY, SCHG, QQQ, DIA, VOT, BITO, RSP, and IWM. Valuentum owns SPY, SCHG, QQQ, VOO, and DIA. Brian Nelson's household owns shares in HON, DIS, HAS, NKE, DIA, and RSP. Some of the other securities written about in this article may be included in Valuentum's simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

0 Comments Posted Leave a comment