Good News from High Yielding AT&T

Image Source: AT&T

By Brian Nelson, CFA

On Thursday, April 22, AT&T (T) reported solid first-quarter results that gave the market confidence that it can make good on its payout to shareholders. The company offers high yield dividend investors an attractive risk-reward profile given its healthy earnings (and free cash flow) coverage of the dividend, in our opinion.

During the period, AT&T’s consolidated revenue advanced 2.7% while adjusted diluted earnings per share came in at $0.86 versus $0.84 in last year’s quarter. Operating cash flow leapt 12% while free cash flow soared to $5.9 billion, up by more than half over the same tally in the year-ago period.

Here’s what CEO John Stankey had to say about the quarter in the press release:

We continued to excel in growing customer relationships in our market focus areas of mobility, fiber and HBO Max. We had another strong quarter of postpaid phone net adds, higher gross adds, lower churn and good growth in Mobility EBITDA. We also continue to increase penetration in markets where we offer fiber broadband and we’re moving quickly to deploy more fiber. HBO Max continued to deliver strong subscriber and revenue growth in advance of our international and AVOD launches planned for June.

AT&T’s 2021 guidance calls for consolidated revenue expansion to be in the 1% range, and adjusted EPS to be roughly even with 2020 performance. Free cash flow generation expected in the $26 billion range for 2021 should handily cover expected cash dividends paid in the year, anticipated at ~$15 billion based on our forecasts within our discounted cash flow model.

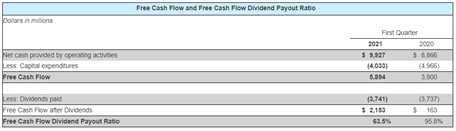

Image Shown: AT&T’s dividend payout ratio is expected to continue to improve. Image Source: AT&T’s first-quarter earnings press release.

AT&T’s dividend payout ratio in the quarter of 63.5% is a big improvement, and management expects its full-year total dividend payout ratio in the high 50%s range. The company doesn’t garner a high Dividend Cushion ratio because of its large net debt position, but free cash flow generation should allow AT&T to keep paying the dividend for the foreseeable future.

We view the Dividend Cushion ratio as a ranking mechanism of dividend health, much like a credit rating ranks credit health. The higher the ratio, the healthier the dividend payout, in most cases. In general, we prefer dividend growth equities that have large net cash positions because a huge net cash load can provide a much-needed backstop to support the dividend during tough times.

AT&T’s net debt stands at a whopping $168.9 billion, however -- though we note its annualized net debt to adjusted EBITDA of ~3.1 is risky but not terrible for its size. By the end of this year, management expects its net debt to be ~$154 billion. Investors should be aware of the risks that a huge net debt position brings to the dividend during times of tough credit, which often coincides with broad-based economic weakness and reduced consumer spending.

Concluding Thoughts

We liked AT&T’s first-quarter results and outlook for 2021 that calls for free cash flow generation to be well in excess of expected cash dividends paid for the year. Investors should be aware of its hefty net debt position, but with a ~7% dividend yield, the company may be hard to pass up for high yield dividend focused investors. We plan to make some tweaks to our valuation model following this report, but our fair value estimate of $34 per share remains unchanged at this time.

AT&T's 16-page Stock report (pdf) >>

AT&T's Dividend report (pdf) >>

Other

Telecom Services: CMCSA, LUMN, DISH, T, TMUS, VZ, SBAC, AMT, CCI, VIAC

Presentation: How to Use our 16-page Stock Reports (pdf) >>

-----

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Brian Nelson owns shares in SPY, SCHG, QQQ, DIA, VOT, and IWM. Brian Nelson's household owns shares in HON, DIS, HAS. Some of the other securities written about in this article may be included in Valuentum's simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

0 Comments Posted Leave a comment