Asset Allocators Fail, Advisors Should Pick Stocks, Save Investors $34 Billion Annually

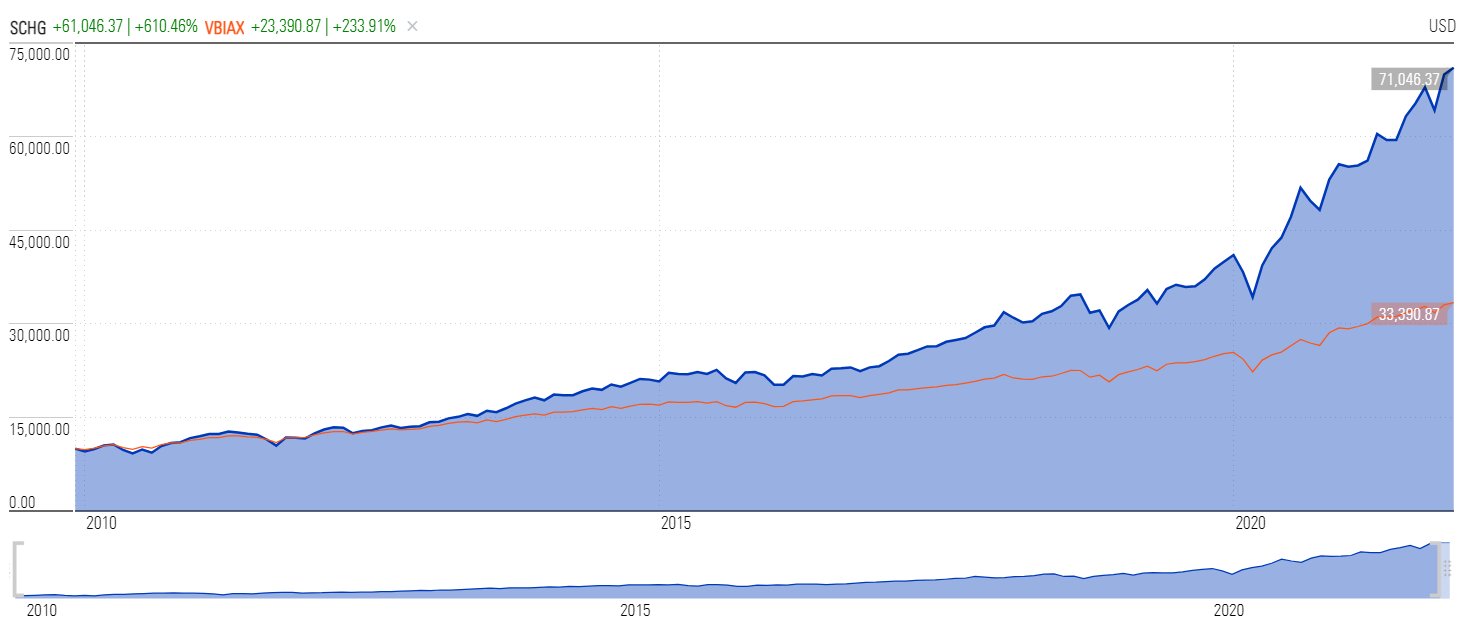

Image: The area of large cap growth has trounced that of the 60/40 stock/bond portfolio for more than a decade. Image Source: Morningstar.

By Brian Nelson, CFA

We’ve all heard the stories.

Professional stock pickers can’t beat a bunch of monkeys throwing darts at the pages of the WSJ. A cows’ investment decisions are just as good as the pros’. Stock prices reflect all available information so not even professionals have an edge (e.g. the efficient markets hypothesis). Most professionals can’t outperform their respective benchmarks, so how could mom and pop? Look at this from one of today’s bloggers:

The traditional argument, which you’ve probably heard many times before, goes as follows: since most people (even the professionals) can’t beat the index, you shouldn’t bother trying.

The data backing this argument is undeniable. You can look through the SPIVA report for every equity market on Earth and you will see (more or less) the same thing—over a five-year period 75% of funds don’t beat their benchmark. And remember, this 75% consists of professional money managers working full-time with teams of analysts. If they can’t outperform with all of these resources, what chance do you have?

This stuff is everywhere.

I am a CFA charterholder with over 15 years’ experience. A couple years ago, I was considering studying for the CFP exam to expand Valuentum’s services into managed portfolios (we’ve since opted to stick exclusively with publishing). On the first page of one of the books of the CFP study materials, there it was, more propaganda being thrown at me:

We know now that asset allocation policy usually explains 100% of the typical return level because most active management does not actually add any alpha. This is particularly true on average, by definition, because in aggregate all money managed can only sum to a broad market return (Foreword, The New Wealth Management, CFA Institute).

Here, the author was referring to Sharpe’s Arithmetic of Active Management, which he just assumes to be correct. Well, it’s not. For some reason, Sharpe and Bogle and their disciples use the return on the average dollar and not average returns in the explanation (for the proof that disproves Sharpe’s Arithmetic, read Value Trap)! Here's a simple way to think about it: In a hypothetical market with 101 investors, where one is Warren Buffett and the other 100 are small-time Robinhood (HOOD) traders with ~$240 balances, if Warren Buffett trails the index by $100 million, you better believe that the average returns of those other 100 investors outperformed the market return.

The industry doesn’t want stock selection to come back into favor, for whatever reason I don’t know. STOCK SELECTION IS FREE! – meaning those expense ratios on many index ETFs are costing investors money, and lots of it. For example, instead of free, the industry has created $34 billion in annual ETF fees. There are some ~7,600 ETFs representing $7.74 trillion USD, and the average ETF expense ratio stands at ~0.44%. Do the math. Indexing is costing investors some serious change. Everybody is ecstatic over low-cost index funds, but now they don’t like free? There’s obviously something else going on.

After all, research has shown that holding 15-25 diversified equity securities across sectors is adequate diversification (these stocks can all be bought and held for free), and from our perspective, holding bonds today makes very little sense. Who wants to lock in a 2% return on a 30-year Treasury? The ICE BofA US High Yield Index stands at a paltry 4.36%. Jeremy Siegel, of Stocks for the Long Run fame, probably would agree. To consider dropping money into various cryptoassets out there is rather treacherous. I hold a little Bitcoin and the BITO not because I want to, but because I have to know this business inside and out--and monitoring crypto helps me stay on top of trends. I’d say I own it against my will.

Debunking the Indexing Propaganda (Again)

Let’s get to brass tacks.

Why am I writing this? Because I’m disgusted by developments in the industry, and perhaps I am more disappointed in myself for not recognizing these biases earlier in my career. Throw the monkey and cow stuff out as they are just straw man arguments to get a chuckle, but how effective they have become as a marketing tool -- am I right? Well, let’s talk efficient markets hypothesis (EMH). EMH is a non-falsifiable hypothesis--something that is not right nor wrong, meaning that theorists can wave their hands at anything and everything, and say it’s incorporated in the price. EMH is the “worst-est, evil-est” game ever played on financial students, and in the name of empirical science it should be removed from the textbooks.

Now, on to something that I used to hold dear--the comparisons of active fund managers to their custom, often holdings-based benchmarks. Many, including random walker Burton Malkiel, have sold investors on the idea that most investors can’t beat the "market" after fees. All I tend to see, however, is that researchers are picking the benchmarks that best approximate the funds, themselves. At face value, this may make sense, but why in the world would we expect a large cap fund after fees to outperform a large cap index with no fees in the first place?

Fund analysis these days seems “rigged,” and the consistent and never-changing interpretations reveal that perhaps the process of evaluating active funds is just plain wrong, or biased. Again, large cap growth after fees versus large cap growth index with no fees? Geez, what do we think will win?!?! The whole point of investing is to pick the right stocks/areas for the long haul--large cap when it is outperforming and other areas when it is not. Comparing large cap growth after fees to itself without fees seems but a silly exercise. We know the answer even before we do the research.

I won’t get into how active funds/ETFs are but 15% of the stock market, and how the industry is making widespread conclusions about stock selection from that, but can you imagine if active investors just picked 15% of the outperforming fund managers for marketing in the same manner; the index fund gang would be out for blood. The industry demands empirical evidence, yet it accepts EMH while making a conclusion on 15% of the stock market supported by questionable analysis that pretty much ensures active funds disappoint. What can I say – index fund fees are hot today:

Morningstar Indexes continued its strong momentum, with revenue increasing by 86.9%, or 83.2% on an organic basis, driven by higher index data licensing sales and strong asset flows and market growth for investable products linked to Morningstar Indexes (Morningstar’s third-quarter 2021 results).

But what about the paradox of skill we've heard so much about? Well, this seems to be the latest add-on development to try to explain why active funds are struggling. Instead of dismissing active fund analysis as being too small of a sample set and that the results are more because of “overbenchmarking” than anything else, some believe that professionals have become more skilled, and this is why variance of their returns is decreasing. Come on. Is it more likely that we’ve all become too smart or maybe there is another reason for active return converging performance:

In investing, the trend toward conformity is clear. For example, portfolios today look more like their benchmarks than they did thirty years ago. The average active share, a measure of how different a mutual fund portfolio is compared to its benchmark, has fallen from 75 percent in 1980 to about 60 percent in 2010 in the United States. Leaders in sports as well as in business fear straying too far from convention, even in cases where the convention isn't all that great (page 174)." - The Success Equation (2012)

Asset Allocation Is Far Overrated

Now, let the rubber hit the road.

Let’s just say you agree with me that comparing stock picking to monkeys and cows is silly, Sharpe’s Arithmetic of Active Management doesn’t use the right measurement stick, EMH is non-falsifiable, we don’t have enough evidence to conclude much of anything about active stock selection from active fund analysis, and that maybe conformity and fear of losing one’s job is more the reason for portfolio returns converging than all of the industry being Einsteins. Well, let’s look at the results from asset allocators that focus more on allocating assets than picking individual stocks.

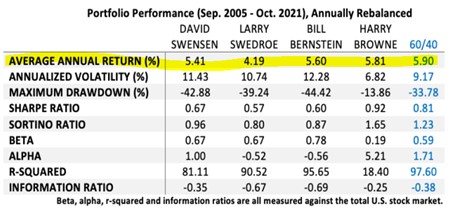

Image: Most asset allocators can’t even keep pace with the underperforming 60/40 stock/bond portfolio. Highlight added by author. Image Source: Wealth Management.

I haven’t met any of these individuals, and recently I heard of Swensen’s passing (he seemed like a great man), but when looking at the results, they should frighten many investors. The highlighted line item above is the performance, as presented by Wealth Management, from the period September 2005 – October 2021, and it shows that some of the more heavily-followed asset allocators failed to keep up with even the 60/40 stock/bond portfolio the past 16 or so years--the same stock/bond portfolio that has trailed the S&P 500 by ~170 percentage points the past 10 years!

From December 31, 2009, through November 15, 2021, a large cap growth ETF (SCHG) outperformed the 60/40 stock/bond portfolio by 375 percentage points. Let’s say that you didn’t fall into the trap of using past results to predict future returns as in overweighting small cap value during this time (maybe you read Value Trap!), and stuck to large cap growth and overweighted some of the best performers this decade like Apple (AAPL), Microsoft (MSFT) and Facebook (FB). That’s not at all too ridiculous to assume, and from our standpoint, made a whole lot of sense the past many years.

Vanguard Claims

But what about volatility? -- the question that turns everything upside down (and is a favorite question to ask when one is underperforming). Well, this, too, shows how indexing and asset allocation comes up short during crises. A 60%/40% stock/bond portfolio, for example, as measured by the Vanguard Balanced Index Fund Investor Shares (VBINX), for example, fell 17.6% year-to-date through March 18, 2020, and it only “saved” investors from a mere 8 percentage points of underperformance during the worst of the COVID-19 swoon relative to the S&P 500 during that time

However, according to Vanguard’s website, the relative cost to an investor that held the VBINX for its diversification benefits during the 10-year period ending July 30, 2020--arguably to protect against the volatility of the exact adverse market outcome as that driven by the COVID-19 crisis--was over 110 percentage points of cumulative total return underperformance compared to the S&P 500, or roughly $11,324 on an initial $10,000 investment. Yet, advisors say that rebalancing actually adds value, 26 basis points in fact, according to Vanguard!!!

It seems like Vanguard can claim just about anything and get away with it these days. The indexing giant has said for a long time that “all of (its) profits are returned to Vanguard shareholders in the form of cost savings,” but then somehow also pays partnership profits and could have “total profits that could top $1 billion,” according to some estimates, while it only recently dropped its “no profit” claim in SEC filings, no less. According to The Inquirer, the company was saying recently it was providing services to its member funds on an "at-cost basis, with no profit component.” I liked Jack as much as the next guy, but this is wrong.

It seems that Vanguard can say anything it wants and own anything at any price, too. How about that? From April 29, 2020:

How seemingly wrong is it for Vanguard to buy anything at any price, as in indexing, and receive implicit support via lifelines to the airlines (Vanguard owns about 6-9% of the major airlines). Furthermore, the public backlash against Boeing...remains in light of 737 MAX troubles, yet Vanguard, which again is not doing any due diligence on individual holdings in the traditional sense, is the largest owner of the company at 7%+.

It seems flat-out wrong that Vanguard’s lack of due diligence and its buy-anything-at-any price strategy isn’t being drilled by Congress at the moment (in fact, nobody is talking about it), and that the U.S. is not looking to tax index funds due to their irresponsible behavior (and to pay for their implicit bailout given their equity stakes in the airlines), or even consider raising corporate taxes to support the growing fiscal deficits and sovereign debt load.

Not good.

Concluding Thoughts

Let’s get this industry back on track.

This isn’t about going all-in on cryptoassets or being reckless with one’s capital the past 10 years, but merely picking stocks as a risk/wealth management strategy that approximated the S&P 500 for the past 10 years, and how that has crushed not only the best that quant has had to offer in small cap value but also indexing and asset allocation. One hundred and seventy percentage points of difference relative to the 60/40 stock/bond portfolio, which itself beat many of the “best” asset allocators out there!!!

This isn’t about taking on more risk, but rather that active stock selection should be viewed in the same vein as asset allocation. Why does the industry continue to publish the obviously-biased research in favor of indexing and asset allocation when stock selection could have delivered so much more for investors while saving them billions in annual fees from ETFs, etc.

Today, the SEC has a lot on its plate regarding SPACs, cryptocurrency, new issues, ETF approvals and beyond, but in our view, the SEC shouldn’t necessarily be prioritizing 2 and 20 fees more than the index-fund fee chain, and it shouldn’t necessarily be trying to eliminate payment for order flow (PFOF) any more than it should seek to eliminate low-cost index funds. Let us not kid ourselves: It's clear why index funds and passive is winning -- the fees are tremendous!

All things considered, if investors want to believe risk is volatility and suffer with indexing and asset allocators, that is their prerogative, but what worked in the past (deviations from equity selection as in the 60/40 stock/bond portfolio) bolstered by high interest rates in the 1980s is far from relevant today (and making up alternative assets isn't going to help). We don’t need more indexing and asset allocation books these days. We need more common sense. Stop selling index funds and start trying to help investors.

----------

Image Source: Value Trap

----------

Tickerized for the DIA.

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Brian Nelson owns shares in SPY, SCHG, QQQ, DIA, VOT, BITO, and IWM. Valuentum owns SPY, SCHG, QQQ, VOO, and DIA. Brian Nelson's household owns shares in HON, DIS, HAS, NKE. Some of the other securities written about in this article may be included in Valuentum's simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

0 Comments Posted Leave a comment