Wells Fargo Has Become An “Epic Disappointment”

Wells Fargo is so far out of line with its large US banking peers that it is truly competing with one arm tied behind its back. Or perhaps both arms. While some might try to be heroic and bet on a huge turnaround, we think it is more prudent to watch from the sidelines. What an epic disappointment this bank has become, so far a fall from grace as compared to when it used to be regarded as one of the best in class of the biggest US banks. What a shame!

By Matthew Warren

Wells Fargo (WFC) delivered a stinker of a second quarter July 14, missing on both the top and bottom lines, and cutting the dividend by 80%--a move that helps the bank preserve capital as it continues to rack up losses during the COVID-19 pandemic and associated economic downturn.

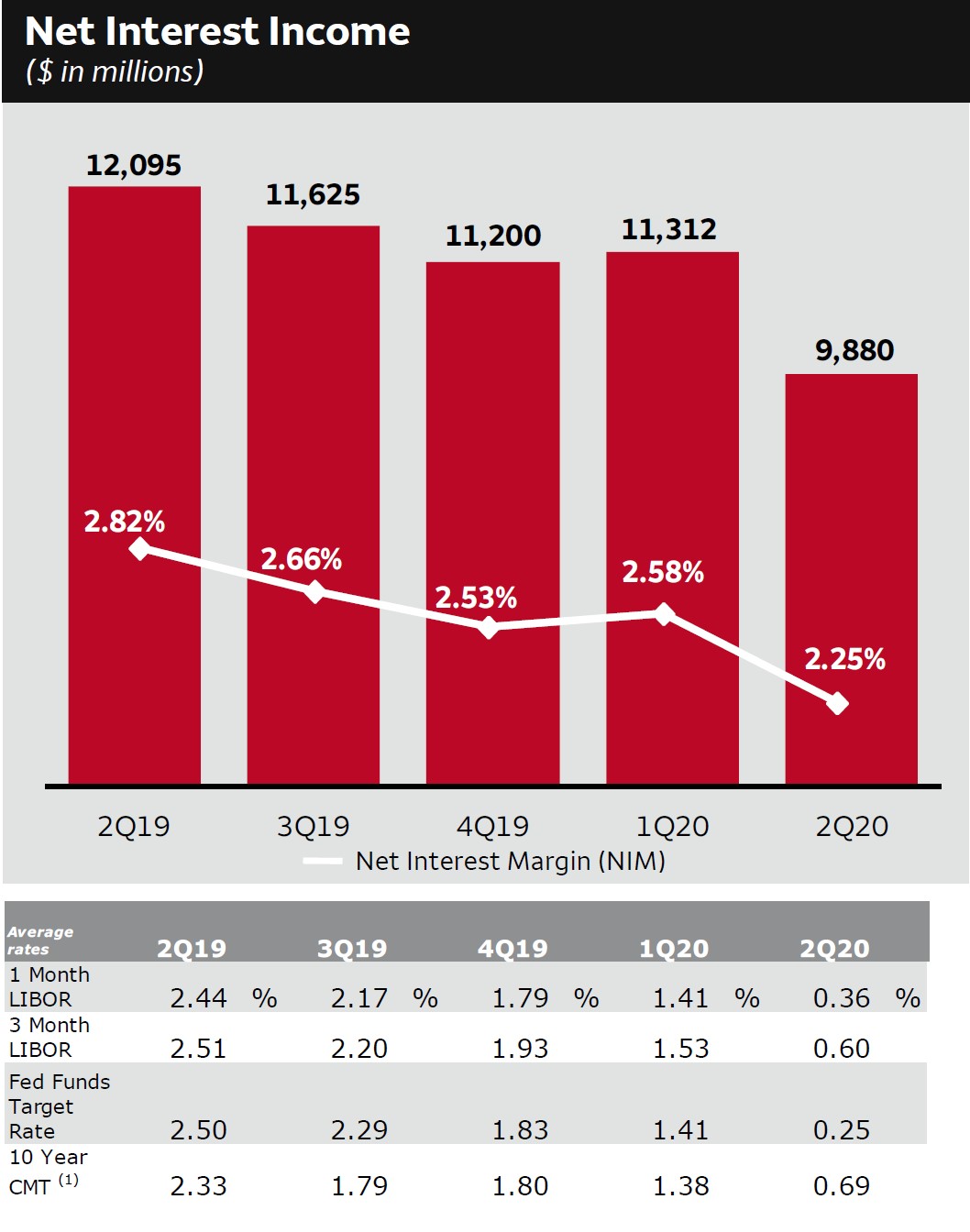

Wells Fargo is facing pressure from all sides, as it continues to deal with the asset cap put in place by its regulators. Not only are revenues under pressure from low rates and a flattish yield curve (as one can see in the upcoming graphic down below), which dents net interest margins, but non-interest revenues are also under pressure from the effects of the economic recession we are facing.

Unlike other banks, Wells Fargo cannot grow its balance sheet to offset some of these revenue pressures. It is also a minor player in the investment banking and trading worlds, where revenues are growing rapidly the past couple quarters.

Image Shown: Wells Fargo net interest income is under pressure due to lower rates and a flat yield curve. Image Source: Wells Fargo 2Q2020 Earnings Supplement

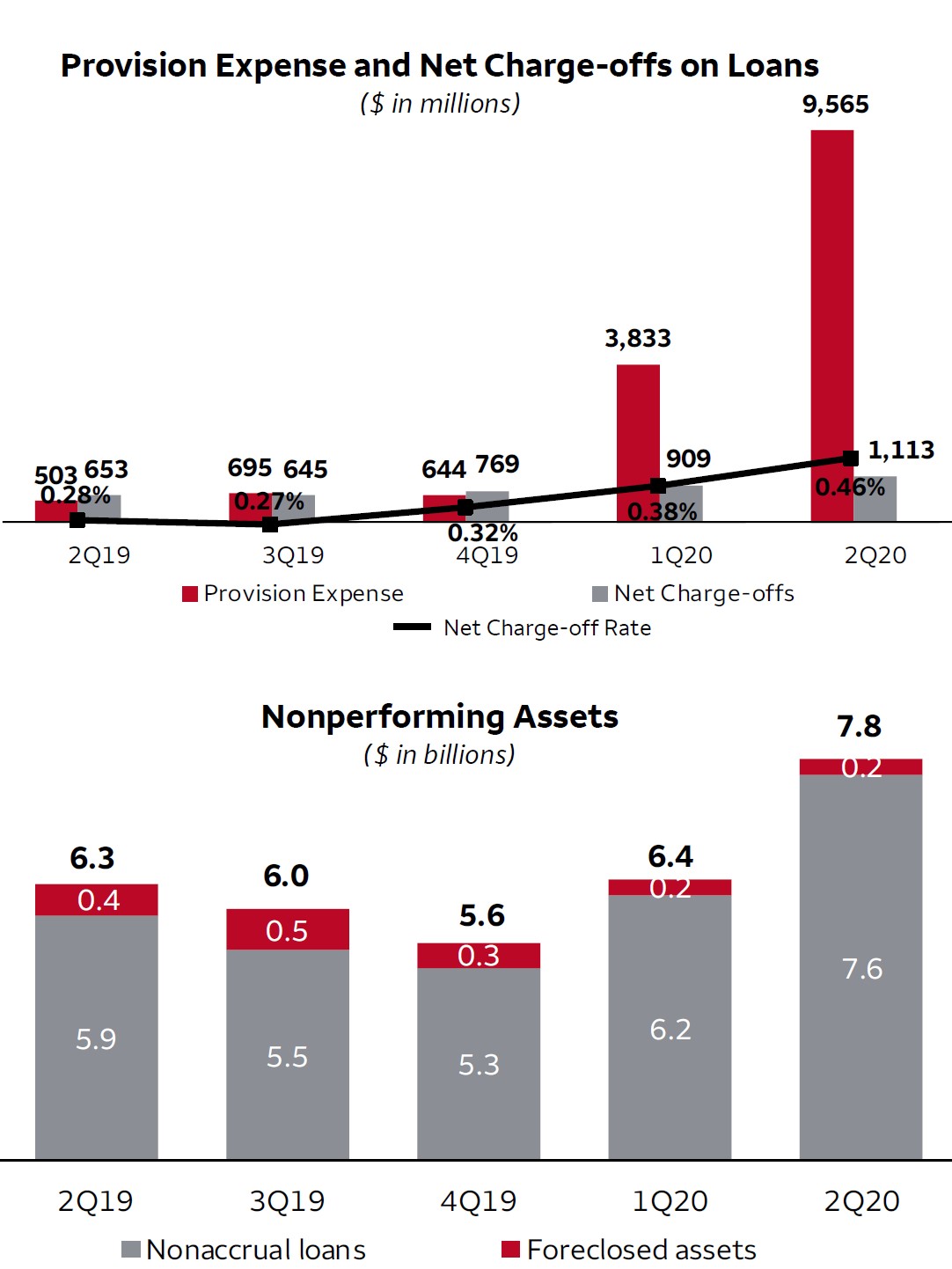

Aside from revenue pressure, the bank is also facing major cost pressure on multiple fronts. First and foremost, the bank is taking massive provisions to account for current and upcoming net charge-offs resulting from pressure on the consumer and commerical accounts alike. In the upcoming graphic down below, notice how much the provision has grown from last quarter, even though the bank is supposed to provision for losses through the cycle at each quarter end. This means Wells Fargo is either slow-walking the losses through the profit and loss statement, or that the economic and client specific outlook has deteriorated rapidly during the past 3 months. We suspect it is a bit of both.

Image Shown: Wells Fargo Provisions are skyrocketing in advance of increasing nonperforming assets and net charge-offs. Image Source: Wells Fargo 2Q2020 Earnings Supplement

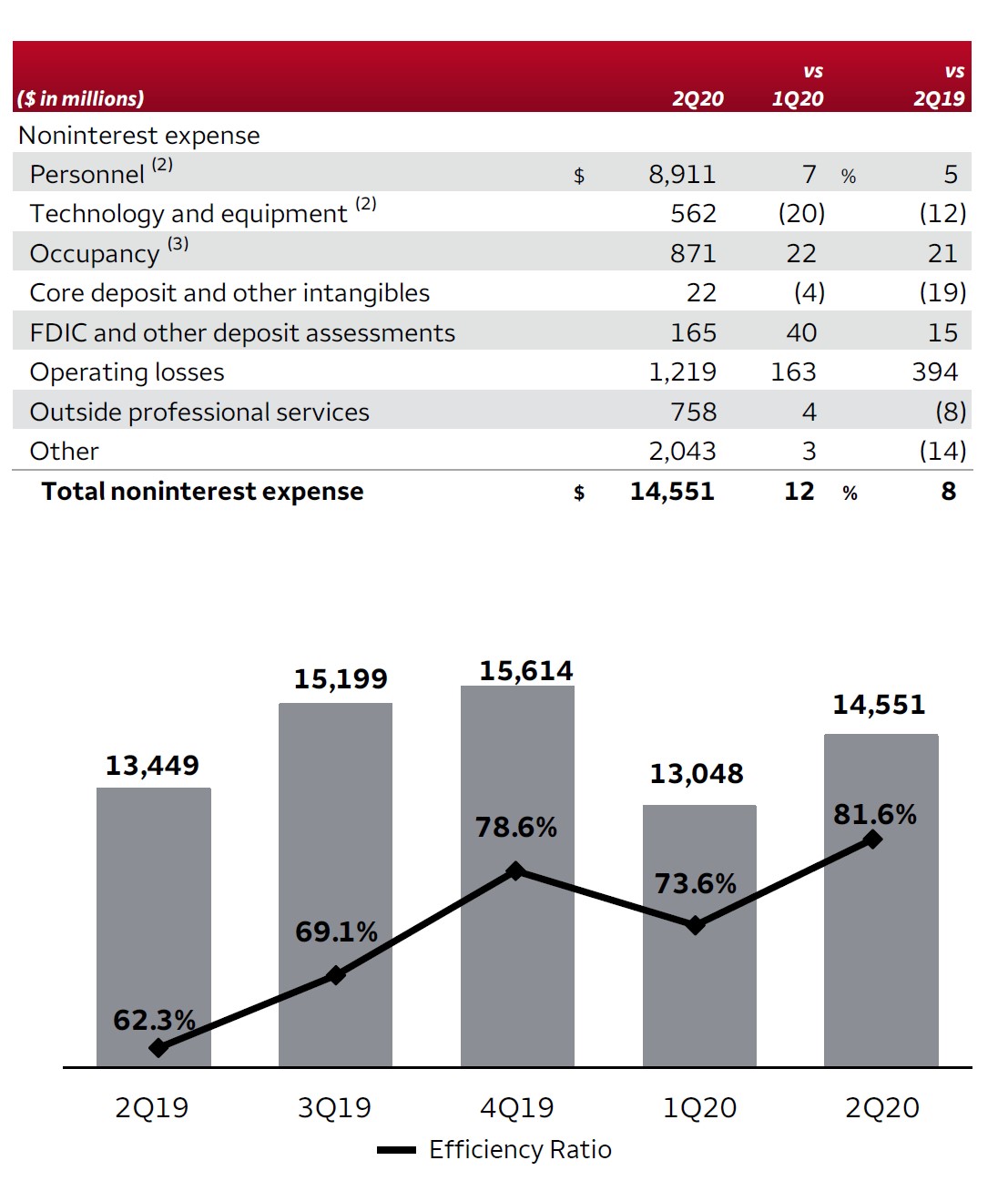

The other area of cost that has been a near constant source of trouble at Wells Fargo is in regards to its personnel cost and efficiency ratio. As one can see in the upcoming graphic down below, the bank’s efficiency ratio has ballooned to 81.6%, which is a far cry worse than its large US banking peers. This is roughly 30 percentage points worse in fact. Management has now come out on the conference call and admitted to the fact that they need to cut out $10 billion out of a $54 billion cost base. That is one Herculean task--all while the regulators continue to pressure the bank to improve the quality of its controls and processes to prevent future problems like what has occurred in the recent past.

Image Shown: Wells Fargo Personnel expenses are out of whack compared to peers, as is its efficiency ratio. Image Source: Well Fargo 2Q2020 Earnings Supplement

Wells Fargo is so far out of line with its large US banking peers that it is truly competing with one arm tied behind its back. Or perhaps both arms. While some might try to be heroic and bet on a huge turnaround, we think it is more prudent to watch from the sidelines. What an epic disappointment this bank has become, so far a fall from grace as compared to when it used to be regarded as one of the best in class of the biggest US banks.

What a shame!

---

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Matthew Warren does not own any of the securities mentioned. Some of the other securities written about in this article may be included in Valuentum's simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

0 Comments Posted Leave a comment