Wells Fargo Faces Regulatory Pressure Amid an Enormous Bad Debt Cycle

Wells Fargo is facing the same enormous bad debt cycle ahead just like its big bank peers, but it is also carrying a ton of its own baggage at just the wrong time. Earnings had already been under pressure before the bad debt cycle had hit, and the bank is facing a very difficult regulatory situation, with a cap on total assets that has been in place since 2018. This is causing the bank to forgo revenue growth opportunities and make difficult trade offs to help existing customers over new customers. This means that Wells is competing with one arm tied behind its back; it has also meant substantially higher costs as the bank has done a ton of hiring to help deal with the regulatory issues. Now Wells is under (optical) pressure to retain employees. All of this has resulted in sliding earnings over the past four quarters.

By Matthew Warren

Wells Fargo (WFC) posted very dismal first-quarter 2020 results April 14, missing analyst consensus estimates (wild guesses at times like these) on both the top and bottom lines. The bank’s revenue of $17.72 billion missed by $1.58 billion and earnings of $0.01 missed by $0.52 per share. The biggest swing in earnings came from a $2.9 billion build in (provisioning for) reserves, which comes in anticipation of bad loans coming straight ahead based on an economy in free fall and rapidly rising unemployment.

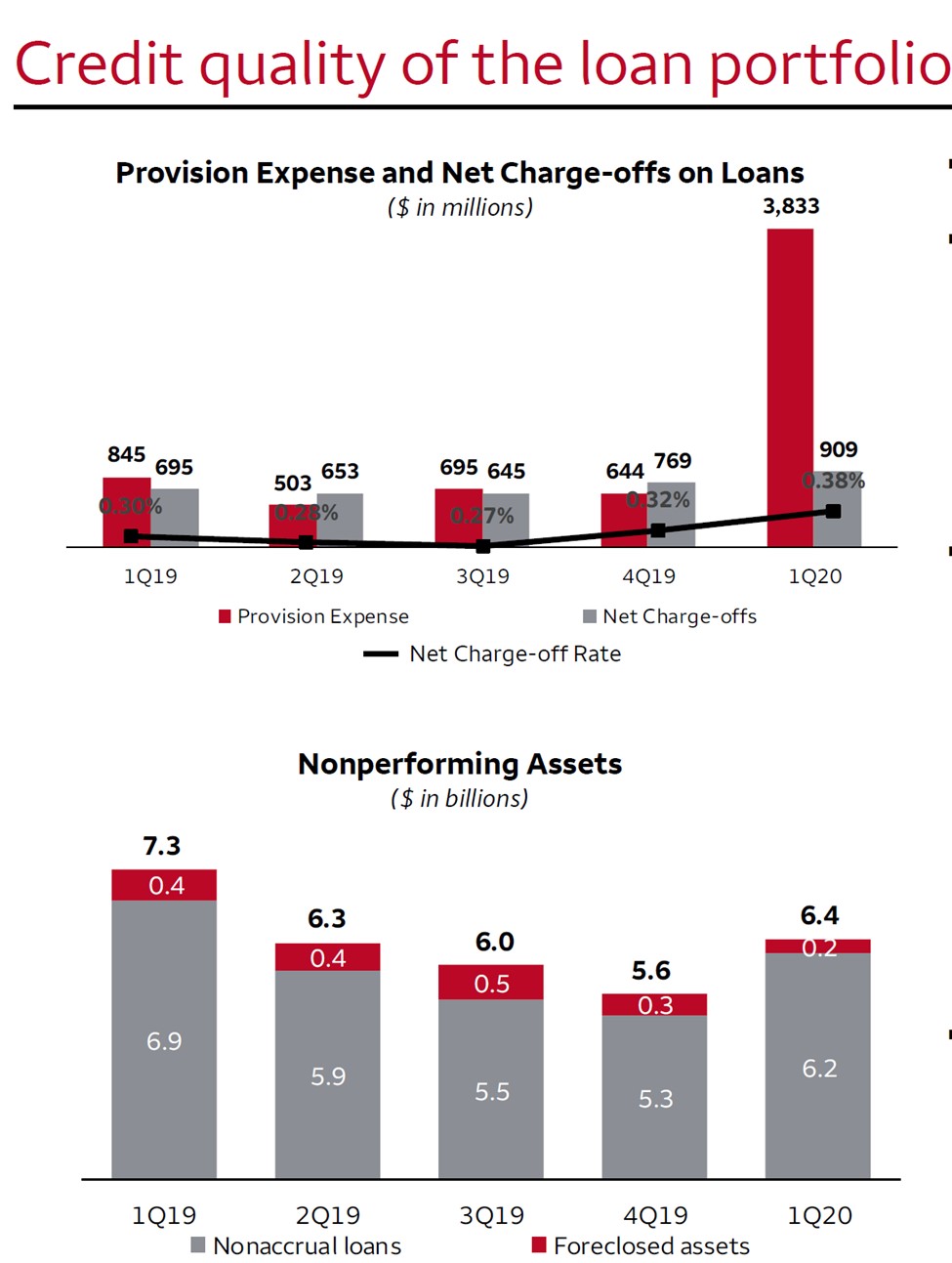

As you can see in the graphic down below, provisions for upcoming credit costs have skyrocketed. The bank also posted a $950 million securities impairment on equity and debt securities that needed to be written down to reflect a mark to market. Since dividends and share buybacks (suspended as at March 15) were greater than earnings, and loan growth due to companies pulling down their credit revolvers, Wells Fargo’s common equity Tier 1 ratio dropped to 10.7% from 11.1% at year end. We still view this as well capitalized.

Image Source: Wells Fargo 1Q2020 Earnings Presentation

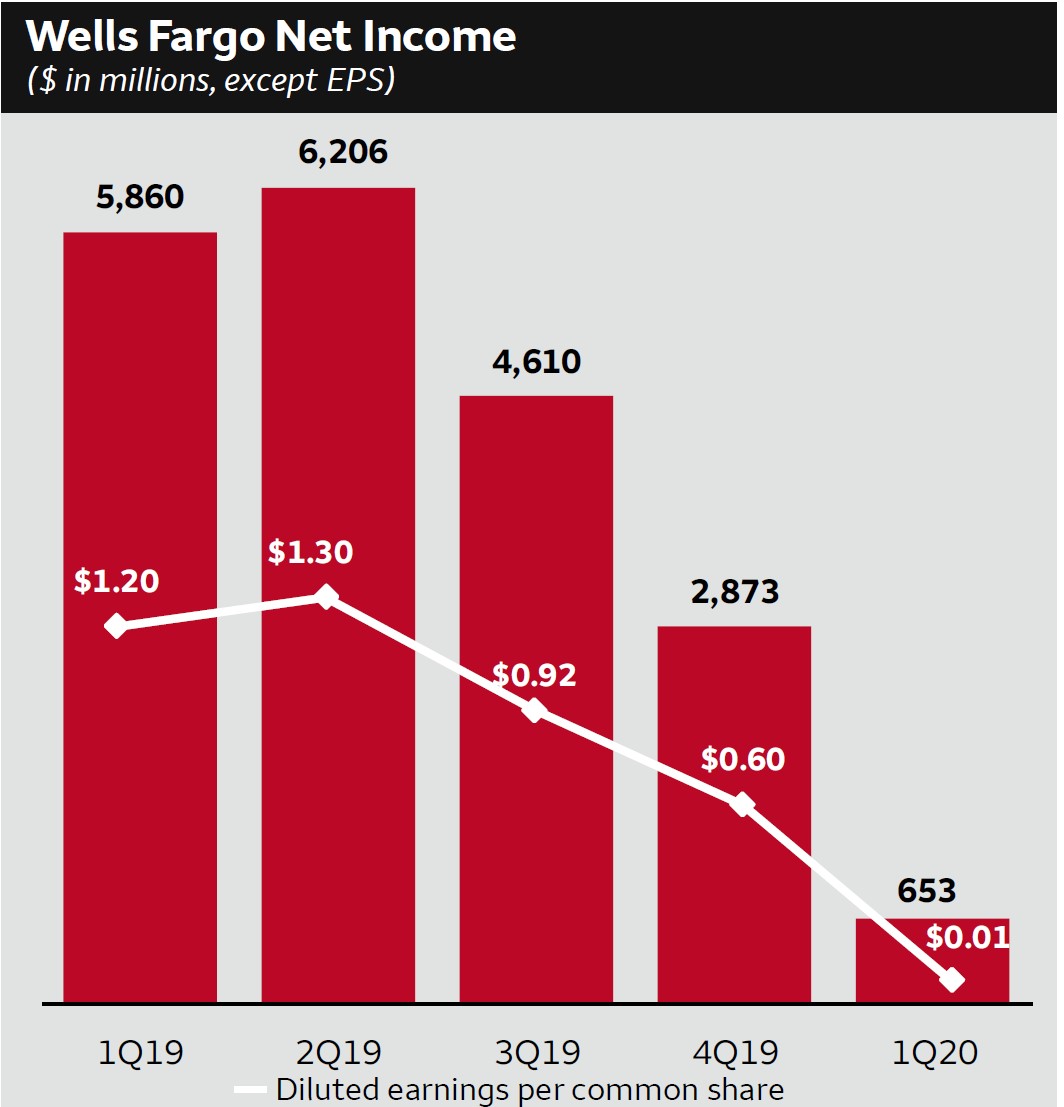

While Wells Fargo is facing the same enormous bad debt cycle ahead just like its big bank peers, it is also carrying a ton of its own baggage at just the wrong time. As you can see in the graphic down below, earnings had already been under pressure before the bad debt cycle had hit. The bank is facing a very difficult regulatory situation, with a cap on total assets that has been in place since 2018. This is causing the bank to forgo revenue growth opportunities and make difficult trade offs to help existing customers over new customers. This means that Wells is competing with one arm tied behind its back; it has also meant substantially higher costs as the bank has done a ton of hiring to help deal with the regulatory issues. Now Wells is under (optical) pressure to retain employees. All of this has resulted in sliding earnings over the past four quarters.

Image Source: Wells Fargo 1Q2020 Earnings Presentation

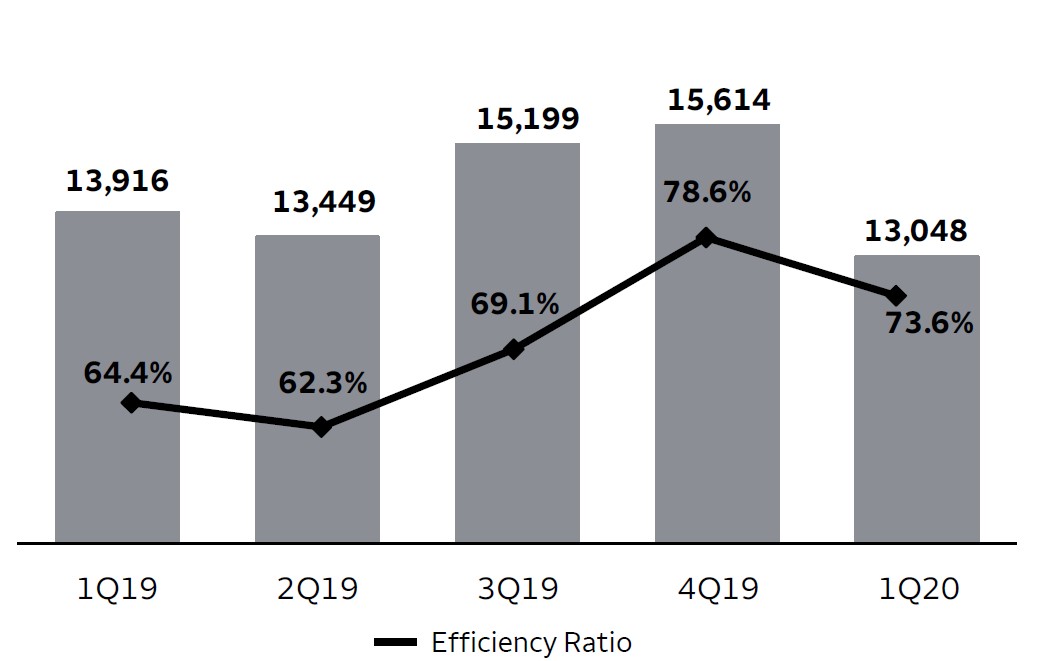

Though net interest margins (NIMs) ticked up slightly sequentially, they are down substantially year over year and non-interest revenue is under a great deal of pressure. Efficiency ratios (see graphic down below) are high and out of line with peer banks and the CEO Charlie Scharf admitted that it will be some time before they can cut costs in a meaningful way (other than revenue related costs that are in fact under pressure.)

Image Source: Wells Fargo 1Q2020 Earnings Presentation

We are maintaining our recently reduced $36 fair value estimate, but the risks appear to the downside. We would also highlight that Wells Fargo’s dividend might be at risk, since the bank is so dramatically underearning the payout right now, and we suspect the rest of the year will remain extremely difficult.

---

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Matthew Warren does not own any of the securities mentioned. Some of the other securities written about in this article may be included in Valuentum's simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

0 Comments Posted Leave a comment