Celgene Implodes

The pharma/biotech industry operates in a boom-bust environment where the market cap of a company can post a meteoric rise or suffer a precipitous fall based on the data published from recently completed clinical trials. The industry remains one of the most innovative fields, but the quest for new products leads to constant disruption and a subsequent spike in volatility. Of late, the volatility pendulum for Celgene has swung in favor of the bears with the company posting a costly phase 3 failure.

By Alexander J. Poulos

Mongersen

The vitality of the clinical pipeline, in our view, is the critical differentiator in the biotech space (XBI, IBB) due to the loss of revenue once patent protection lapses on existing products. We tend to favor companies that have a broad pipeline of unique products in areas of critical need. Celgene (CELG) neatly falls into this category as the clinical profile of Mongersen seemed poised to disrupt the industry, but the molecule failed to live up to the initial promise.

We were mildly surprised by the report as our initial read-through of phase 2 data was not inspiring, but defered to the expert opinion of the management team of Celgene as it saw fit to advance the molecule to phase 3. As a molecule progresses through the various stages of clinical trials, the costs associated with the molecule rise. Thus, a phase 3 trial is very costly as significant time and resources have been devoted with little to show for the effort.

Mongersen was being developed for the treatment of Crohn’s Disease and Ulcerative Colitis—the inflammatory disease category is the most significant portion of specialty drug spend in the country. If Mongersen had been successful, it would have provided additional relief for those afflicted with the disease. It would also have expanded the pool of treatments utilized by the PBM’s to negotiate for lower overall rates per treatment, thus in some respects aiding the total healthcare budget. The discontinuation of Mongersen is a disappointment, which led to a steep sell-off in shares, but the bulk of the damage may really be in the view that the reimbursement landscape has changed within Celgene’s existing product line-up.

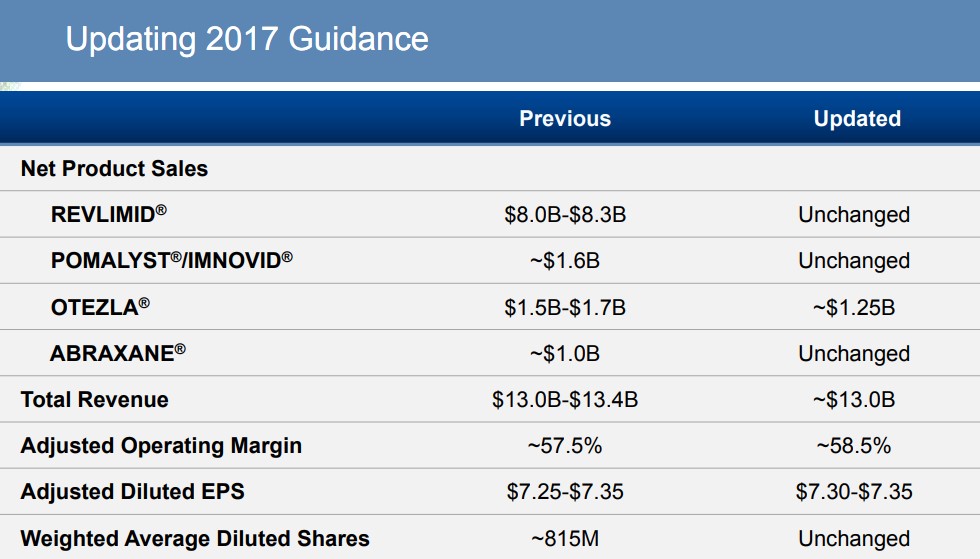

Image Source: Celgene Q3 2017 Earnings Presentation

Otezla

The competitive environment for 'inflammatory diseases' has evolved in a manner that has caught Celgene’s management by surprise as the initial sales projections for Otezla have turned out to be wildly optimistic (as shown in revision table above). Celgene reduced its Otezla projections by over $250 million, thus fracturing the confidence many investors have placed in the management team of Celgene.

That said, we are taking a far more sanguine view of the chain of events as we feel Celgene was hit with a perfect storm. We do not believe the innovation engine is broken as we think the company will recover as new molecules are brought to market. The drop in Otezla is not a surprise to us as the remarkable growth posted by Dividend Growth Newsletter portfolio idea Novartis (NVS) Cosentyx accounts for a significant portion of the loss of volume witnessed by Otezla and Amgen’s (AMGN) Enbrel. Cosentyx possesses a favorable safety profile, which Novartis is utilizing to drive widespread formulary coverage. In exchange for broad formulary inclusion, Novartis is willing to sacrifice price to gain volume.

The initial 50%+ year-over-year growth in Otezla, in our view, is emblematic of over-aggressive assumptions that have “blown up” in the face of management. The takeaway that investors will carry with them is growth is declining for Otezla, whereas year-over-year growth (assuming the $1.25 billion number is achieved) will come in at 23% (2016 sales of Otezla were $1.017 billion). The management team bungled the news, in our view. It should have pre-announced the shortfall along with the Mongersen news. The sell-off after the earnings release only shook investor confidence even more.

Pipeline

The costly phase 3 failure of Mongeresen forced Celgene to revise its 2020 outlook, but we are not too concerned with the targets laid out by the team, as a host of unknown variables (positive and negative) will manifest themselves long before 2020. We feel it is far more instructive to focus on the near-term clinical pipeline, in this case, along with the health of the overall balance sheet to garner a feel for the potential going forward.

Celgene sports an impressive cash and marketable securities balance of $11.76 billion as of the latest quarterly report. The growth of Revlimid continues to generate an abundance of cash for Celgene, the cash of which is critical once the need arises to diversify away from the product (when the patent lapses). Celgene has demonstrated a willingness to strike strategic partnerships in addition to outright acquisitions of promising molecules. We are reasonably confident the team will continue to broaden the pipeline.

Celgene wisely hedged its bets with the acquisition of Mongersen by acquiring the rights to Ozanimod, too, an innovative oral treatment that is being studied for a host of specialty diseases ranging from multiple sclerosis to Ulcerative colitis. We have recently reviewed the data posted by Ozanimod versus beta-interferon (Avonex) and came away impressed with the efficacy coupled with a side-effect profile on par with Avonex. We feel the oral dosage form is a crucial differentiator on par with Roche’s (RHHBY) recently-approved MS treatment Ocrevus. Ozanimod is currently in phase 3 trials for Multiple Sclerosis and Ulcerative Colitis along with phase 2 for Crohn’s Disease. Assuming the molecule is a success, it will in our opinion more than offset the expected loss of revenue from Mongersen.

Celgene is actively seeking to broaden the prescribing label for Otezla in an effort to expand the overall market for the treatment. The molecule has entered into phase 3 trials for scalp psoriasis and as a potential therapy for Behcet’s Disease. We view additional indications as a necessary step to expand the product label, thus garnering incremental sales for the product. The main focus of Celgene’s product pipeline remains concentrated in the field of oncology with multiple molecules in various stages of clinical development. We continue to view Celgene as one of the preferred partners in the area, especially with its well-documented history of a willingness to engage in developmental partnerships. The innovative partnerships struck by Celegene allow the company a proverbial “multiple shots on goal” approach which may increase the likelihood of a string of clinical successes.

Conclusion

We continue to admire the innovative success posted by Celgene, but we cannot get excited over its prospects at this juncture. The company posts a rather unimpressive Valuentum Buying Index rating of 4 at the time of this writing, and the lack of a dividend further diminishes the appeal. Valuentum tends to like Johnson & Johnson (JNJ), an idea in both newsletter portfolios, Novartis and Gilead Sciences (GILD) in the healthcare/biotech space at this juncture. There is also a rather sizable position in the Healthcare Sector SPDR ETF (XLV) in the Best Ideas Newsletter portfolio. Celgene’s aggressive fallout should be on your radar, in any case.

Independent Healthcare and Biotech Contributor Alexander J. Poulos is long Gilead Sciences and Celgene.