Walking Through the Calculation of the Dividend Cushion Ratio

A cow for her milk, A hen for her eggs, And a stock, by heck, For her dividends. An orchard for fruit, Bees for their honey, And stocks, besides, For their dividends. - John Burr Williams, “The Theory of Investment Value” (1938)

Executive Summary: We believe the Dividend Cushion ratio is one of the most helpful tools an income or dividend growth investor can use in conjunction with qualitative dividend analysis. The ratio is one-of-a-kind in that it is both free-cash-flow based, considers balance sheet health, and is forward looking. Since its development in 2012, we estimate its efficacy at ~90% in helping to forewarn readers of impending dividend cuts. For companies where Valuentum reports are available, the Dividend Cushion ratio can be found in a stock's Dividend Report or in the table on the company's stock landing page. We use Kimberly-Clark as an example of how we calculate the Dividend Cushion ratio and how useful it is for investors of all types.

Note: This article is for educational purposes only to explain the nuts-and-bolts behind the calculation of the Dividend Cushion ratio. To access our updated opinion on Kimberly-Clark, please view its 16-page stock report and Dividend Report on its stock landing page here. A version of this article appeared on our website July 3, 2013. Updated December 1, 2020. To read our academic white paper on the Dividend Cushion ratio, "The Dividend Cushion Beats the Aristocrats," please download Valuentum's latest write up at the following link: http://www.valuentum.com/articles/20150506.

By Brian Nelson, CFA

We've received a significant amount of interest in the Dividend Cushion ratio, and we wanted to walk through the Dividend Cushion ratio calculation for an example company, Kimberly Clark (KMB), in this article. The Dividend Cushion ratio is derived from the forecasts within our discounted cash-flow models (enterprise valuation, as explained in the book, Value Trap), and the ratio measures the financial capacity of a company to pay and grow its dividend in the future--not necessarily the willingness of the company to pay and grow its dividend. Both capacity and willingness are necessary to achieve sustainable growth in a company's payout, so paying attention to a company's historical dividend growth track record (also available in a company's Dividend Report) to assess willingness is also very important.

Kimberly-Clark is generally what is described as a Dividend Aristocrat, meaning it has raised its dividend in each of the past 25+ years (40+ years in Kimberly Clark's case). The company's dividend yield is above the ~2% average for S&P 500 companies, offering a ~3% annual dividend payout at recent price levels (as of December 1, 2020). We generally prefer annualized dividend yields above 3% and generally don't include stocks with yields below 2% in the Dividend Growth Newsletter portfolio (unless under rare occassions where we expect dividend growth to be explosive in coming years, as in the case of Microsoft of Apple, as examples). We update the simulated Dividend Growth Newsletter portfolio monthly as a key component of the Dividend Growth Newsletter, which is released on the first of each month to members via email.

We measure the future safety or durability of a company's dividend in a unique but very straightforward and logical fashion. As many know, accounting earnings (earnings per share, or EPS) can fluctuate significantly through the course of the economic/business cycle, so using the traditional dividend payout ratio (dividends per share divided by earnings per share) in any given year has substantial limitations. For one, companies can often encounter non-recurring charges/expenses (e.g. extraordinary or one-time items), which makes single-year accounting (reported) earnings (or the single-year payout ratio) a less-than-predictable measure of the safety of the dividend. We know companies won't simply cut the dividend just because earnings have temporarily declined, or eliminate the payout in cases, for example, where a firm had a restructuring charge that put it in the red for a quarter (or year or two).

We therefore believe that assessing the forward-looking traditional free-cash-flow (cash flow from operations less all capital spending) and balance-sheet dynamics (total cash less total long-term debt) of a business, in conjunction with the firm's dividend payout ratio and other items, is a more reasonable approach in determining whether a company has the capacity to continue paying and growing dividends than the dividend payout ratio alone. This line of thinking has led us to develop the forward-looking Dividend Cushion ratio.

The Dividend Cushion measure is a ratio that sums the existing net cash (total cash less total long-term debt) a company has on hand (on its balance sheet) plus its expected future free cash flows (cash from operations less all capital expenditures) over the next five years and divides that sum by future expected cash dividends (including expected growth in them, where applicable) over the same time period. If the ratio is significantly above 1, the company generally has sufficient financial capacity to pay out its expected future dividends, by our estimates.

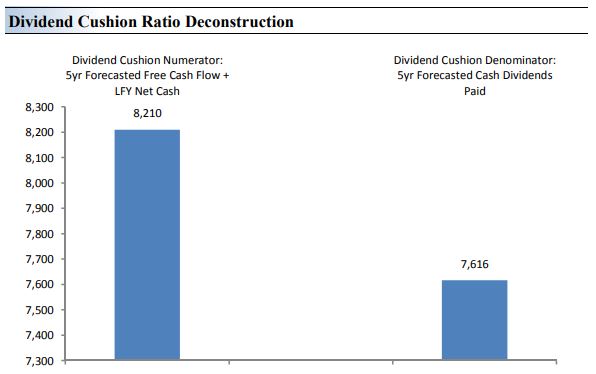

The higher the ratio, the better, all else equal. An elevated ratio doesn't always ensure the company will keep paying dividends, however, as management's willingness to do so is another key consideration (as we've noted above), but the ratio acts as a logical, cash-flow based ranking of dividend health (dividend cut risk), much like a corporate credit rating, for example, ranks a company's ability to pay back debt (default risk). A low Dividend Cushion ratio (e.g. 0.5) doesn't mean a company will cut its dividend in the near term, no more than a junk-rated credit rating (e.g. BB+) means a company will default on its debt tomorrow. Both the Dividend Cushion ratio and corporate credit ratings measure and rank risk. The image below showcases the mathematics behind the calculation of the Dividend Cushion ratio.

Image: We assess the safety of a firm's dividend by adding the company's net cash to our forecast of its free cash flows over the next five years. We then divide that sum by the total expected dividends over the next five years. This process results in the Dividend Cushion ratio. A Dividend Cushion ratio significantly above 1 indicates a company can cover its future dividends with net cash on hand and future free cash flow (by our estimates), while a score below 1 signals trouble may be on the horizon. By extension, the greater the ratio, the stronger the dividend, as excess cash can be used to offset any unexpected earnings shortfall.

Dividend growth and income investors may like to see a Dividend Cushion ratio much larger than 1 for a couple of reasons: 1) the higher the ratio, the more "cushion" the company has against unexpected earnings and cash shortfalls, and 2) the higher the ratio, the greater capacity a dividend-payer has in boosting the dividend in the future. At the time of the publishing of this article, Kimberly-Clark's Dividend Cushion ratio is 1.1, revealing that on its current path the company should be able to cover its future dividends (and the expected growth in them) with net cash on hand and future free cash flow over the measurement period. Note that the higher the future expected dividend obligations (the denominator), the more difficult it is for companies to register high Dividend Cushion ratios. By definition, most high dividend payers will generally have lower Dividend Cushion ratios, which makes sense--they have greater dividend obligations and greater risk.

Derivation of Kimberly-Clark's Dividend Cushion

Let's now dig into the math.

To arrive at the Dividend Cushion ratio for Kimberly-Clark, we divide the numerator ($8,210 million) by the denominator ($7,616 million), as shown in the image immediately below. The numerator represents the sum of a company's net cash position and its cumulative analyst-driven 5-year expected free cash flows, as measured by cash flow from operations less all capital spending. The denominator represents the sum of a company's cumulative 5-year expected cash dividends paid (note that the denominator includes our growth expectations, too).

The calculation for Kimberly-Clark results in a ratio of 1.1. A ratio of 1.1, as it is for Kimberly-Clark at the time of this writing, can be considered GOOD, absent any extraordinary considerations that pose exogenous threats to the payout (e.g. extreme cyclicality, competitive pressures, secular declines in a company's core product, an outsize net debt position despite strong free cash flows, and some others). In most cases, however, the higher the Dividend Cushion ratio above 1, the better.

To reiterate, as in the case of Kimberly-Clark, we estimate the sum of Kimberly-Clark's net balance sheet position at the end of last fiscal year and its future expected free cash flows to be generated over the next five years to be ~$8.2 billion. We estimate that the company will pay out ~$7.6 billion in cash as dividends over the same time period, and we divide the numerator by the denominator to arrive at a Dividend Cushion ratio of 1.1 for Kimberly-Clark.

Image Source: Valuentum

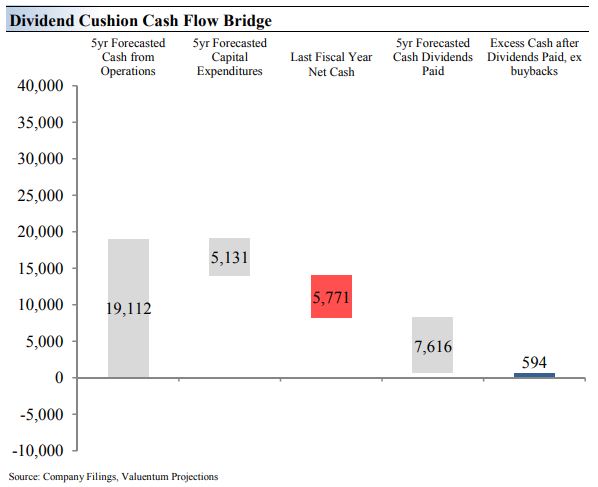

The difference between the numerator and denominator of the Dividend Cushion ratio is the firm's 'total cumulative 5-year forecasted distributable excess cash after dividends paid, excluding buybacks.' The difference represents the excess cash that can be applied to more dividend increases (above that which are forecast in the analysis) during the 5-year measurement period. The following build in the image below is a mapping of Kimberly-Clark's residual free cash flow after deducting both capital spending and cash dividends (and after considering net debt obligations).

The build up below illustrates why Kimberly-Clark has a Dividend Cushion ratio above 1. The residual blue bar at the right of the chart (in the image below), or the difference between the numerator and the denominator, as shown in the above image, is positive, even if it may be modest in the context of the firm's robust cash-flow-from-operating dynamics. All else equal, when it comes to dividend growth, we tend to like equities that have relatively large/healthy Dividend Cushion ratios (coupled with acceptable dividend yields), though management's willingness to sustain and raise the dividend, business model risk and valuation should never be ignored.

It's worth noting that companies that have high Dividend Cushion ratios may have a significantly larger 'blue bar' than Kimberly-Clark's (image below), relatively speaking and in the context of their respective financial statements. We posit that such companies have significantly more excess cash that can be applied to future dividend increases, all else equal, for one reason or another (e.g. lower expected dividend obligations, stronger net cash position). Note that the greater the future expected dividend obligations, the greater tendency for the Dividend Cushion ratio to approach 1 (given the outsize denominator).

Derivation of Kimberly-Clark's Total Cumulative 5-year Forecasted Distributable Excess Cash after Dividends Paid, excluding buybacks

Image Source: Valuentum

The chart immediately above shows that Kimberly-Clark has a significant amount of dividend obligations to pay out in the coming years relative to its future expected free-cash-flow generation over this time frame (the dividends expected to be paid is the fourth bar from the left, and just like capital expenditures, absorbs cash generated from operations, the first bar on the left). The above analysis at the time of publishing considers a ~3% annual future growth rate in dividends per share (from 2021-2024), as shown on the front page of Kimberly-Clark's Dividend Report (view the front page of the Dividend Report at the bottom of this article)--meaning the Dividend Cushion ratio analysis is forward-looking and considers growth expectations in the dividend, too. This is an important consideration--the Dividend Cushion ratio measures the durability and dividend growth potential of the dividend payout above and beyond our expected dividend growth rates.

Within the simulated Dividend Growth Newsletter portfolio, we generally prefer firms that have a very large estimated residual cash position over the next five years, or a very large measure of 'total cumulative 5-year forecasted distributable excess cash after dividends paid, excluding buybacks' -- the blue bar in the graph immediately above. The companies with the largest 'blue bars' are the ones with the strongest future dividend-growth prospects as measured by financial capacity, in our view. Dividend growth and income investors may consider equities that have a good balance of a strong dividend yield that meets certain personal criteria, a strong/healthy Dividend Cushion ratio, and is headed by a management team dedicated to sustaining and growing the payout. Some firms have nice income streams, but if they also have a high Dividend Cushion ratio, they may be poised for material dividend-payout expansion, too.

Now on to a discussion of the potential growth of Kimberly-Clark's dividend. As mentioned above, the greater the "cushion," the greater financial capacity a firm has to raise the dividend in the future, in our view--but such dividend growth analysis is lacking if management's willingness to increase the dividend is ignored. As such, we evaluate the company's historical dividend track record. If a) there have been no dividend cuts during the past 10 years, b) the company has had a nice growth rate in recent years, and c) the firm boasts a strong Dividend Cushion ratio, we'd rate its future potential dividend growth as GOOD or EXCELLENT in the company's Dividend Report, which is the case for Kimberly-Clark. After all, in this case, Kimberly-Clark is a Dividend Aristocrat--meaning it has raised its dividend in at least each of the past 25 years.

The dividend is very important to dividend growth and income investors, but capital preservation is also an important consideration for all investors. We therefore assess the risk associated with the potential for capital loss. The in-depth valuation analysis is primarily included in each stock's 16-page report (a separate report than the Dividend Report also found on the company's stock landing page), but we also provide the valuation conclusions in a stock's Dividend Report for convenience. In Kimberly-Clark's case, at the time of the publishing of this article, we think its shares are OVERVALUED (the firm's share price falls above our estimated fair value estimate range), so the risk of capital loss is rated as HIGH. If we thought shares were undervalued, the risk of capital loss would be rated as LOW.

Wrapping Things Up

The Dividend Cushion ratio is a forward-looking ratio (with a simple but informative numerator and a denominator). It tells readers, on the basis of our estimates, how many times future expected free cash flow (cash from operations less capital spending) will cover future expected cash dividend payments after considering the net cash on the balance sheet--also a key source of dividend strength. It is purely fundamentally-based and driven from items taken directly from the financial statements and our analysts' forecasts.

For dividend growth and income investors, we think the Dividend Cushion ratio should be assessed at least quarterly/semi-annually, as it reflects an ongoing assessment of the health and durability of a company's dividend payout and its growth prospects. Enterprise valuation and share-price momentum aside, stocks with acceptable dividend yields, strong Dividend Cushion ratios, and a committed management team may be among the most attractive dividend paying stocks, in our view.

<< Download Kimberly-Clark's current Dividend Report

<< Access Kimberly-Clark's stock page

<< FAQ: Where Can I Find the Valuentum Dividend Cushion Ratio?

<< Explaining the Difference Between the Adjusted and Unadjusted Dividend Cushion Ratio and More

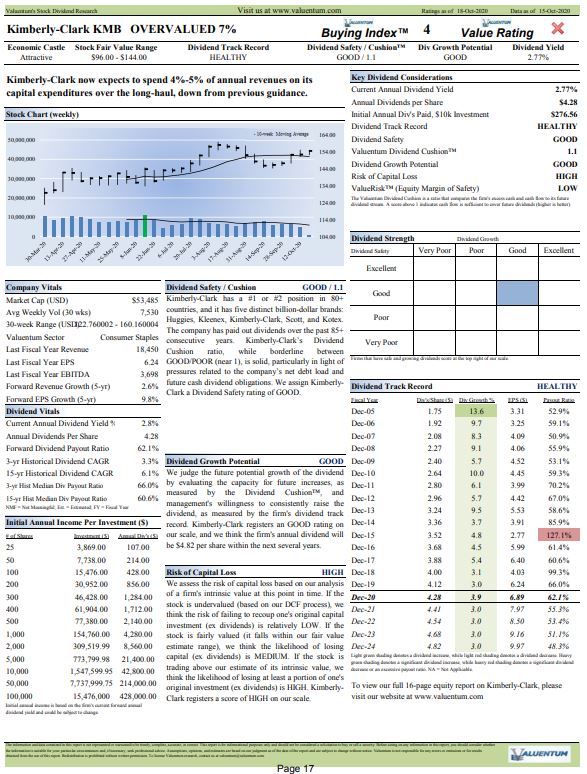

Image shown below: Page 1 of Valuentum's dividend report on Kimberly-Clark, as of October 2020.

Tickerized for holdings in the SDY. Also for ETFs: NOBL, TDV, WDIV, REGL.

-----

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Brian Nelson owns shares in SPY, SCHG, DIA, VOT, and QQQ. Some of the other securities written about in this article may be included in Valuentum's simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.