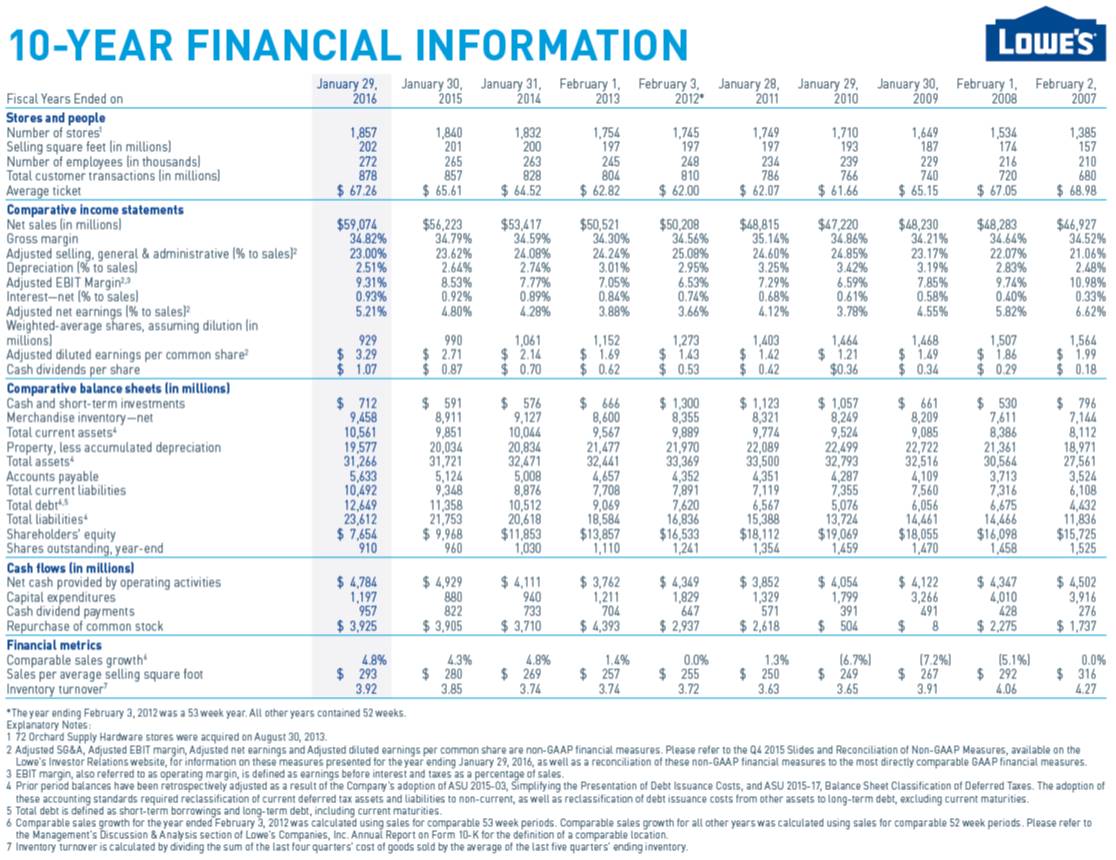

Lowe’s – The 10-Year History

Image Source: Lowe's, 10-year Financial Summary

Request a 10-year financial review like this one of another company. Only $129/each. Or request your entire portfolio up to 20 companies for just $1,999. Select payment button to book a request, and then contact us at info@valuentum.com.

What a treasure trove of financial information--Lowe’s (LOW) 10-year financial history, that is. Let’s walk through a few observations that we think are important for holders of its equity to be aware of.

Resilient Top-line Growth and Gross Margins

In looking at Lowe’s unit store growth, selling square feet and average ticket during the past 10 years, we bear witness to consistent growth, and that’s a good thing. Net sales, despite falling during the Financial Crisis in 2010, have also advanced in each of the past 10 years, on resilient gross margins that have amazingly hovered in a very tight range of ~34%-35%. Even some of the most seasoned companies will have some degree of variability in the gross margin over as long a period as a decade, and in this light, the consistency of its gross margin is certainly worth noting, if not highlighting. This speaks of a rational pricing marketplace as Lowe’s continues to bump heads with Home Depot (HD), mom-and-pop hardware stores and lumber yards including Lumber Liquidators (LL). We love this consistency about Lowe’s business, and it speaks more of a duopolistic environment than one of fragmentation.

Cyclical Operating Margins and Same-Store Sales

Interestingly, the consistency on the gross margin line may be a necessity, as Lowe’s adjusted operating (EBIT) margins have been volatile. It may not look like a large swing from 10.98% in 2007 to 6.53% in 2012 back to 9.31% in 2016, but it’s important to think in terms of percentage change, not in percentage-point change for this one. Given Lowe’s sizable revenue line, small changes in the adjusted operating (EBIT) margin line translate into rather large changes in operating earnings. So while a drop of 4.55 percentage points to 2012 from 2007 in the gross margin may not sound too severe, it is a drop of ~40% in terms of overall operating profitability. In this light, profit trends at Lowe’s are very cyclical, and interestingly, it took Lowe’s to 2014 to finally surpass adjusted diluted earnings per share marks achieved in 2007--and a significant reduction in diluted shares outstanding to do so.

Lowe’s comparable store sales have also exhibited a hyper-cyclical trend, even if one might characterize the most recent Financial Crisis as a generational recession, one not likely to be repeated in severity anytime soon. After flat same-store sales performance in 2008, for example, comparable store sales dropped for three consecutive years in 2008 (-5.1%), 2009 (-7.2%), and 2010 (-6.7%), a rather interesting occurrence to witness as consecutive declines are compounding phenomena, and management would have had sufficient time to right the aggressive drops, even if such a period bounded the housing crisis. Only more recently has same-store sales performance returned to a more respectable mid-single-digit annual pace, but the timing of the next housing downturn (and declining same-store sales) is the only question. The question is not if same-store sales will decline again (they will), and our biggest worry is that the market may overly punish Lowe’s in light of what we’d describe as a natural part of its business.

Rising Debt But Flat Cash Flow from Operations?

I love looking at long-term financial information because it offers a great deal of information. Lowe’s total debt has expanded to $12.6 billion in 2016 from $4.4 billion in 2007, and while management has revealed a degree of discipline during the Financial Crisis with total debt dropping in 2010 and the company raising cash at that time, the loose credit market has become too easy to pass up for the executive team, it seems. There’s nothing “wrong” with taking on more and more debt or having a large and growing net debt load (total debt less cash and short-term investments), but it is evident that financial performance at Lowe’s has been augmented by adding more and more leverage to its business model--not only in more debt itself, but also in a substantial and significant reduction in diluted shares outstanding (shrinking the equity portion of its balance sheet).

Interestingly, while sales of Lowe’s have jumped to $59.1 billion in 2016 from $46.9 billion in 2007 and adjusted diluted earnings per share have surged as a result in part of a massive debt-financed reduction in shares outstanding to 929 million in 2016 from 1.56 billion in 2007, net cash provided by operating activities can best be described as “flattish,” even cyclical. Net cash provided by operating activities of $4.5 billion in 2007 dropped to $3.8 billion in 2013 (a few years after the Financial Crisis) and has only recently surpassed 2007 levels at $4.9 billion and $4.8 billion in 2015 and 2016, respectively. There hasn’t been much growth in operating cash flow generation during the past decade, and in this light, free cash flow has primarily been bolstered by a reduction in capital spending (~$1.2 billion in 2016 from ~$4 billion in 2007 and 2008). We would like to see free cash flow propelled by significant operating cash flow expansion, not a drawdown in investment, as in the case of Lowe’s.

The Financials Tell the Story

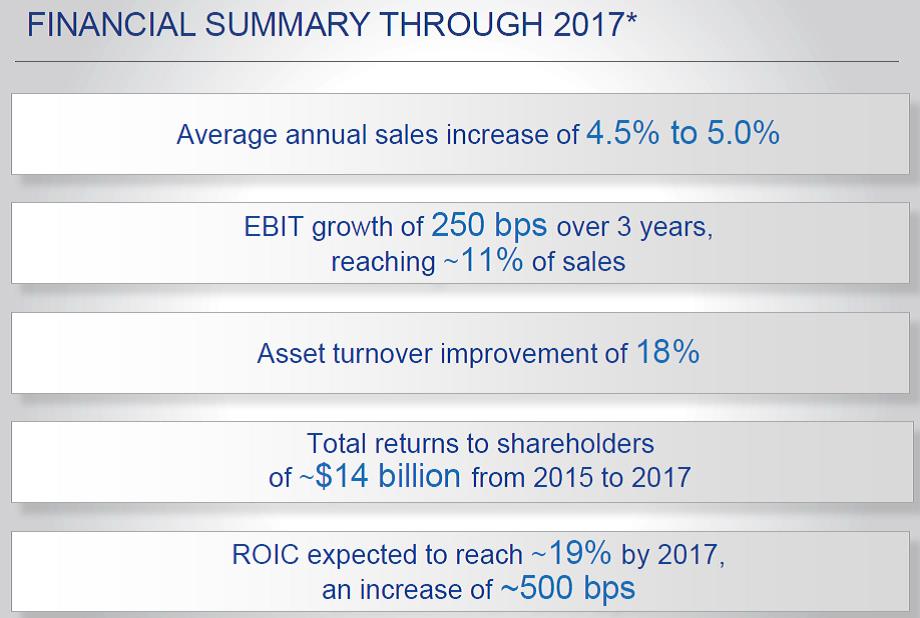

Lowe’s is a fantastic company with significant competitive advantages, and the home improvement retailing market may be as strong as ever, even if we are at or nearing peak demand for this cyclical recovery. Looking at its 10-year financials, however, is quite informative, even if it may not influence one’s conviction in the equity one way or the other (remember, this is a historical evaluation, and the future is what matters). But did you know that a large portion of Lowe’s diluted earnings per share expansion has been a direct result of financing initiatives (aggressive debt-funded stock buybacks), or that most of its surge in free cash flow has been a result of a massive reduction in capital spending during the past decade?

It should be no surprise that Lowe’s will continue to aggressively buy back stock as it targets materially lower annual capital spending levels of ~$1.2 billion through 2017. If management achieves its 11% target for EBIT in 2017, such a mark would only be modestly better than levels achieved a decade ago. We’re huge fans of Lowe’s but the financials tell a story of one that has benefited more from its financial initiatives than operating ones. Interesting to dig deep into the historical financials, no? You’ll never quite know all that you’ll find.

Request a 10-year financial review like this one of another company. Only $129/each. Or request your entire portfolio up to 20 companies for just $1,999. Select payment button to book a request, and then contact us at info@valuentum.com.

Image Source: Lowe’s Strategy Slides