Image Source: Walmart

By Brian Nelson, CFA

On February 20, Walmart (WMT) reported better than expected fiscal fourth quarter results, but issued guidance lower than what the Street was looking for. Revenue increased 4.1%, or 5.3% in constant currency in the quarter, while its gross margin rate advanced 53 basis points. Operating income increased $0.6 billion, or 8.3% (adjusted up 9.4% constant currency) thanks to higher gross margins, growth in membership income and improved economics in eCommerce, which grew revenue 16% led by store-fulfilled pickup and delivery. Global advertising revenue advanced 29%, including 24% for Walmart Connect in the U.S. Adjusted earnings per share came in at $0.66 in the quarter, up from $0.60 in the same period a year ago.

Management had the following to say about the quarter:

Our team finished the year with another quarter of strong results. We have momentum driven by our low prices, a growing assortment, and an eCommerce business driven by faster delivery times. We’re gaining market share, our top line is healthy, and we’re in great shape with inventory. We’ll stay focused on growth, improving operating margins, and strengthening ROI as we invest to serve our customers and members even better.

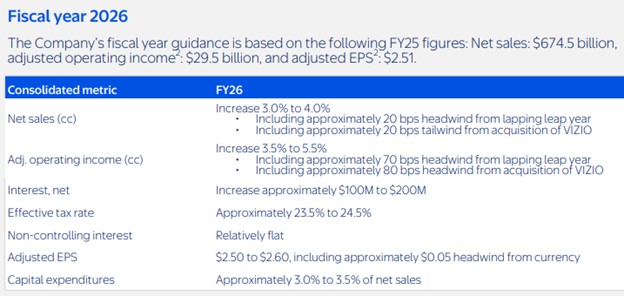

Walmart ended its fiscal year with cash and cash equivalents of $9.0 billion and total debt of $45.8 billion. Operating cash flow for fiscal 2025 was $36.4 billion, an increase of $0.7 billion from last year, while free cash flow remained robust at $12.7 billion. Looking to the first quarter of fiscal 2026, net sales are expected to increase 3%-4%, while adjusted operating income is expected to advance 0.5%-2%, with adjusted earnings per share targeted in the range of $0.57-$0.58, below the $0.65 consensus estimate. For all of fiscal 2026, net sales are anticipated to increase 3%-4%, with adjusted operating income expected to increase 3.5%-5.5%. Adjusted earnings per share is targeted in the range of $2.50-$2.60 for the full year (consensus was at $2.76), inclusive of a $0.05 headwind from currency. Shares yield 0.9%.

—–

Brian Nelson owns shares in SPY, SCHG, QQQ, QQQM, DIA, VOT, RSP, and IWM. Valuentum owns SPY, SCHG, QQQ, QQQM, VOO, and DIA. Brian Nelson’s household owns shares in HON, DIS, HAS, NKE, DIA, RSP, SCHG, QQQ, QQQM, and VOO. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.