The combination of revenue pressure from lower rates, a difficult operating environment, weakening efficiency metrics, one-off losses, and arguable low provisions for credit losses make for an ugly picture emerging at Unicredit at this time. We’re paying close attention to the key banking players in Europe to assess the likelihood of a global financial contagion that may accompany the global pandemic that has become COVID-19.

By Matthew Warren

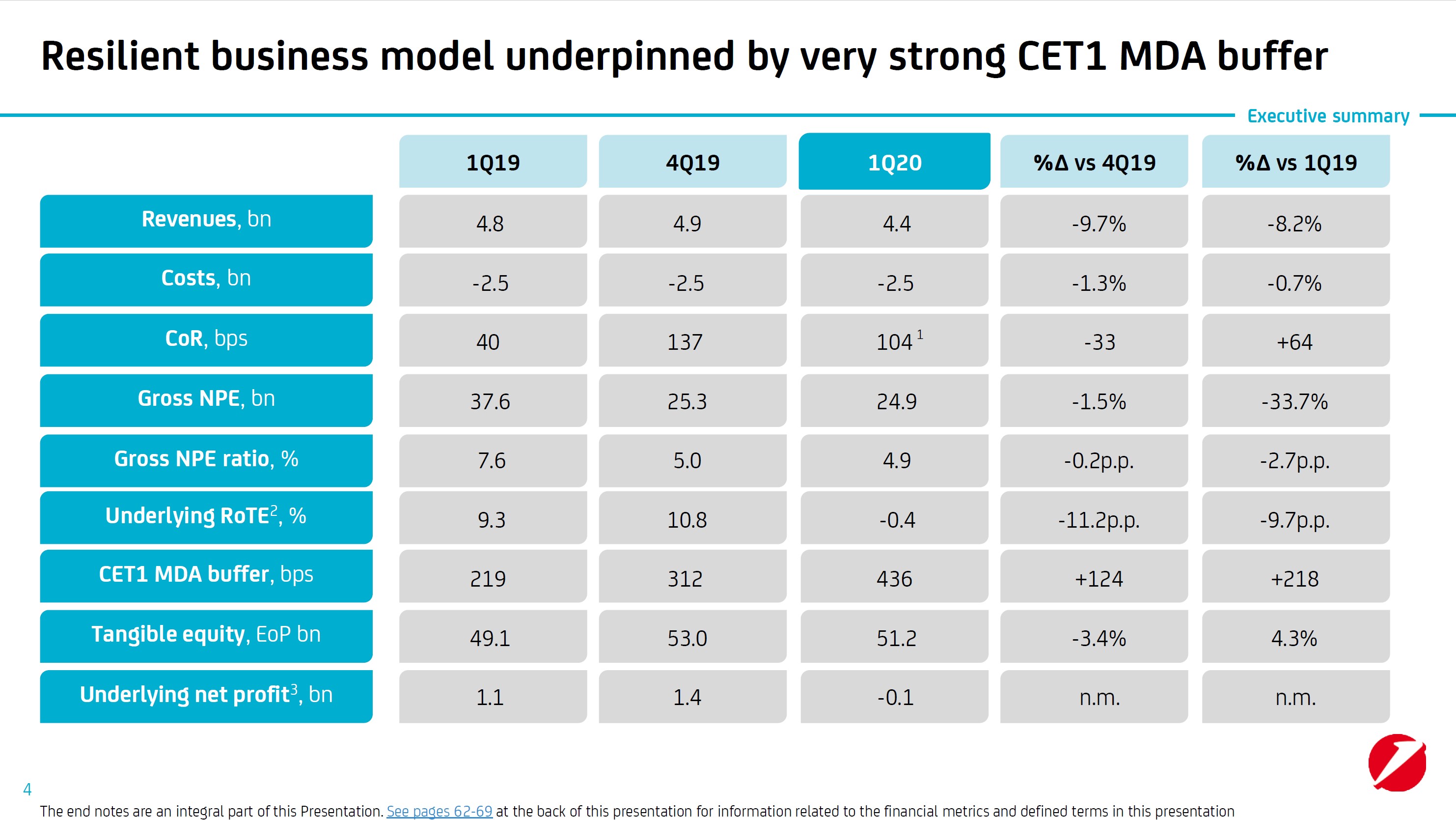

Unicredit (UNCFF) posted dismal first-quarter results May 6 that showed revenue falling 8.2% and negative “underlying net profit” of EUR 100 million from the same period last year. Stated net profit in the period was even worse at negative EUR 2.706 billion, including integration costs in Italy (EWI), a loss related to the Yapi transaction, and real estate disposal gains partially offsetting the former two negatives. As one can see in the graphic below, non-performing exposures remain uncomfortably high at 4.9% at quarter end, though down from extremely elevated levels just last year.

Image Source: Unicredit 1Q2020 Earnings Presentation

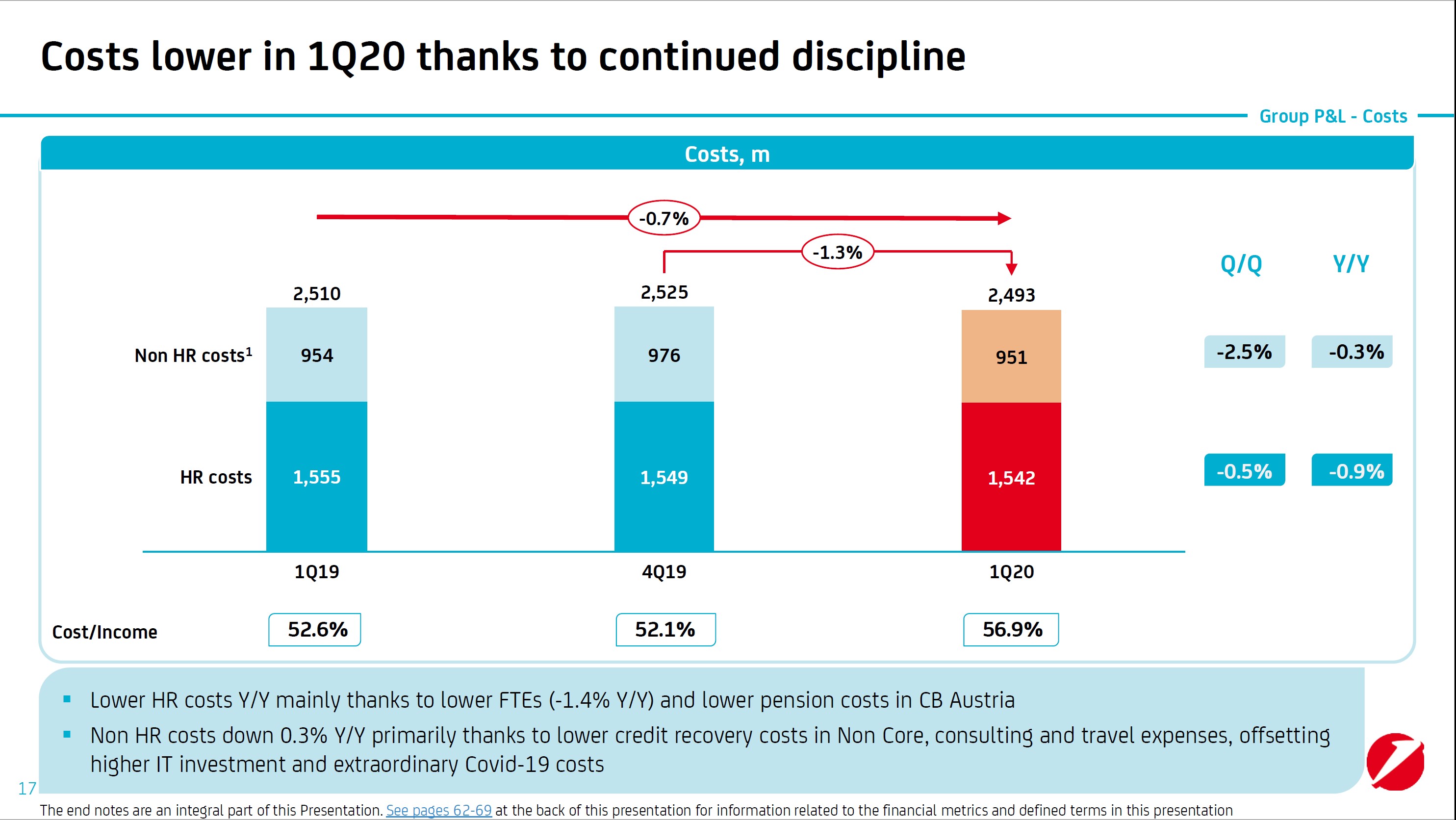

With a cost of risk of 104 basis points (bps), as compared to 137 bps in the fourth quarter of last year, we remain very skeptical that the bank is taking appropriate provisions for loan losses, which we expect to mount in the period(s) ahead. Unlike many of its peers, it doesn’t look like Unicredit is getting ahead of coming loan losses. Further, as one can see in the below graphic, despite reasonably good cost control efforts, the revenue pressure facing the bank has its cost/income ratio jumping substantially in the period, a clear worsening of efficiency.

Image Source: Unicredit 1Q2020 Earnings Presentation

The combination of revenue pressure from lower rates, a difficult operating environment, weakening efficiency metrics, one-off losses, and arguable low provisions for credit losses make for an ugly picture emerging at Unicredit at this time. We would also point out that Unicredit is exposed to a possible worsening of sovereign risk given Italy’s outlier high debt/GDP ratio and as well as the risk that spreads over comparable German (EWG) bonds may blow out again if periphery Euro countries and banks come under substantial question yet again. We would avoid this bank and are watching banks like this closely for potential mounting problems.

—

Related articles:

BNP Paribas’ Shares Could Have Upside Potential, May 7, 2020

Lloyds Banking Group Navigates Competitive Markets, May 4, 2020

Deutsche Bank Suffering From Lack of Earnings Power, April 30, 2020

Santander Remains Well-Capitalized, April 29, 2020

Related: UNCFY, UNCRY, CRZBY

—

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Matthew Warren does not own any of the securities mentioned. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.