By Brian Nelson, CFA

On December 9, luxury homebuilder Toll Brothers (TOL) reported better-than-expected fourth-quarter fiscal 2024 results with revenue and non-GAAP earnings per share coming in higher than the consensus forecasts. Home sales revenues increased 10% in the quarter, while delivered homes were 3,431, up 25%. Net signed contract value was up 32% compared to the same quarter a year ago, with contracted homes of 2,658, up 30%. Backlog value, however, fell 7% on a year-over-year basis, with homes in backlog of 5,996, down 9%.

Toll Brothers’ adjusted home sales growth margin, which excludes interest and inventory write-downs, came in at 27.9% in the quarter, below the adjusted home sales gross margin of 29.1% in the fiscal fourth quarter of last year. Pre-tax income expanded to $621.1 million compared to $605 million in last year’s quarter. Net income and earnings per share came in at $475.4 million and $4.63, up from $445.5 million and $4.11 in the same quarter a year ago. Management had a lot to say about the quarter:

I am very pleased with our fourth quarter results, which cap the strongest year ever for Toll Brothers. For the full year, we generated a record $10.6 billion of home sales revenue, earned $15.01 per diluted share and grew contracts by 27% in both units and dollars. In the fourth quarter, we delivered 3,431 homes and generated $3.3 billion in home sales revenues, up 25% in units and 10% in dollars compared to last year’s fourth quarter. Our fourth quarter adjusted gross margin was 27.9%, beating guidance by 40 basis points, and our SG&A expense was 8.3% of home sales revenues, or 30 basis points better than guidance. Our strong margin performance and better than projected home sales revenues drove earnings of $4.63 per diluted share in the quarter, up 13% compared to last year. We also signed 2,658 net contracts at an average price of $1,000,000, up 30% in units and 32% in dollars compared to last year’s fourth quarter. Our performance this year and in the fourth quarter demonstrates the power of our luxury brand, the financial strength of our buyers, and the success of our strategies of increasing our spec home production and widening our geographies, price points and product lines.

Since the start of our fiscal 2025 six weeks ago we have seen strong demand, which is encouraging as we approach the beginning of the spring selling season in mid-January. We are well positioned with communities in over 60 markets across 24 states featuring the widest offering of luxury homes and serving the most affluent customers in our industry. Last year, we increased community count by 10% and are targeting a similar increase in fiscal 2025. We also owned or controlled approximately 74,700 lots at year end, providing sufficient land for further growth in fiscal 2026 and beyond.

In fiscal 2024, we generated a return on beginning equity of 23.1%, driven by our record earnings and strong cash flows that allowed us to return approximately $720 million of capital to shareholders. Our healthy balance sheet, low leverage, and ample liquidity, including significant projected cash flows from operations in fiscal 2025, should allow us to continue investing in our business while returning cash to shareholders well into the future.

Image Source: Toll Brothers

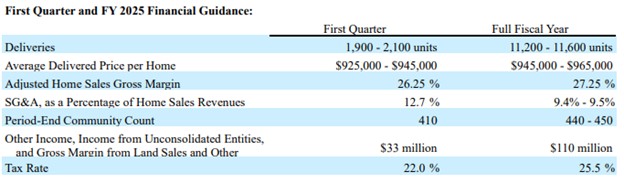

Looking to fiscal 2025, Toll Brothers’ deliveries are expected in the range of 11,200-11,600 units with an average delivered price per home of $945,000-$965,000 and adjusted home sales gross margin expected at 27.25%. The company’s pace of deliveries is expected to be strong, but the company’s gross margin isn’t as strong as we would like, facing pressure from last year’s adjusted mark. SG&A, as a percentage of home sales revenue is expected in the range of 9.4%-9.5%, up from last year’s measure of 9.3%.

Toll Brothers ended its fiscal fourth quarter with $1.3 billion in cash and cash equivalents and $2.7 billion in loans payable and senior notes. The company continues to return cash to shareholders in the form of buybacks and dividends. Though we don’t include Toll Brothers in any newsletter portfolio, the bellwether’s fiscal fourth quarter report indicates the housing market remains healthy.

—–

Tickerized for holdings in the ITB.

Brian Nelson owns shares in SPY, SCHG, QQQ, DIA, VOT, RSP, and IWM. Valuentum owns SPY, SCHG, QQQ, VOO, and DIA. Brian Nelson’s household owns shares in HON, DIS, HAS, NKE, DIA, RSP, SCHG, QQQ, and VOO. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.