Image Shown: Netflix Inc’s paid subscriber base is expected to grow at a slower pace in the near term compared to the performance seen in recent years. Image Source: Netflix Inc – Shareholder letter covering the fourth quarter of 2021

By Callum Turcan

On January 20, Netflix Inc (NFLX) reported fourth-quarter 2021 earnings after the bell. The video streaming giant met consensus top-line estimates and beat consensus bottom-line estimates last quarter as original content such as the South Korean TV show Squid Game (released September 2021) proved to be quite popular in markets around the globe and helped Netflix retain interest in its service. During Netflix’s latest earnings call, management noted that the violent Squid Game TV show had been renewed for a second season when asked by an analyst about the issue.

However, the near-term guidance Netflix provided in conjunction with its latest earnings update signaled that growth in its paid subscriber base was expected to slow down in the first quarter of 2022 on both a year-over-year and sequential basis. During regular trading hours on January 21, shares of NFLX were pummeled.

Financial Update

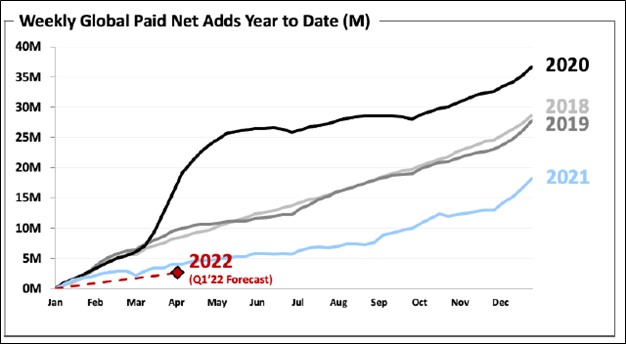

In the fourth quarter of 2021, Netflix added 8.3 million net paid memberships to its subscriber base, which was short of its internal forecasts calling for growth of 8.5 million (issued during the third quarter). Netflix forecasts that it will grow its net subscriber base by 2.5 million memberships on a sequential basis during the current quarter, a figure that underwhelmed investors. Here, we will caution that Netflix’s subscriber growth has historically been volatile as one can see in the upcoming graphic down below. For all of 2021, Netflix added ~18.2 million net paid memberships to its subscriber base.

Image Shown: Netflix’s near term guidance indicates its paid subscriber growth rate is expected to slow down in the first quarter of 2022 on both a sequential and year-over-year basis. Image Source: Netflix – Shareholder letter covering the fourth quarter of 2021

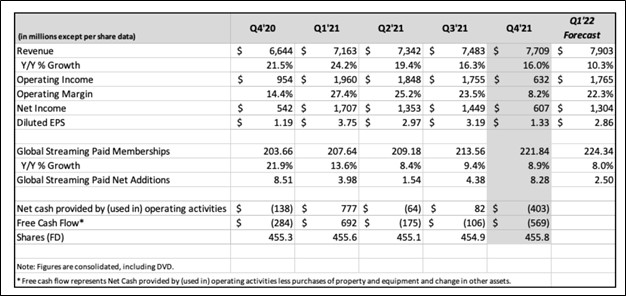

In 2021, Netflix grew its GAAP revenues 19% and its GAAP operating income 35% on an annual basis. We appreciate the operating leverage of Netflix’s business as revenue growth can lead to meaningful margin expansion, which ultimately supports its future cash flow performance (which hasn’t been great, as the image above shows). Beyond paid subscriber growth, Netflix’s pricing power was also at play as it concerns growing both its revenues and operating income.

For instance, Netflix increased the price of its subscriptions in the US and Canada in late 2020. Defined as Netflix’s ‘UCAN’ geographical reporting segment, this region represents the company’s largest single source of revenue and is its most lucrative market. Netflix has a history of steady price increases in the US and Canada, and we appreciate its pricing power. The firm announced in January 2022 that it was once again increasing its monthly subscription fees in the US and Canada.

Some of its competitors have also recently pushed through domestic price increases. Hulu, owned by both The Walt Disney Company (DIS) and Comcast Corporation (CMCSA), increased the price on some of its US subscriptions in October 2021. Additionally, the cost of Disney+ went up in the US back in March 2021.

Pivoting to Netflix’s cash flow performance last year, it generated $0.4 billion in net operating cash flow and spent $0.5 billion on capital expenditures, resulting in -$0.1 billion (negative $0.1 billion) in free cash flow in 2021. Please note that some of its original content spend that was slated for 2020 got pushed into 2021 due to the coronavirus (‘COVID-19’) pandemic forcing production activities to get delayed. The company also repurchased $0.6 billion of its shares in 2021, primarily to offset dilution from stock-based compensation as its weighted-average diluted share count still rose last year versus 2020 levels.

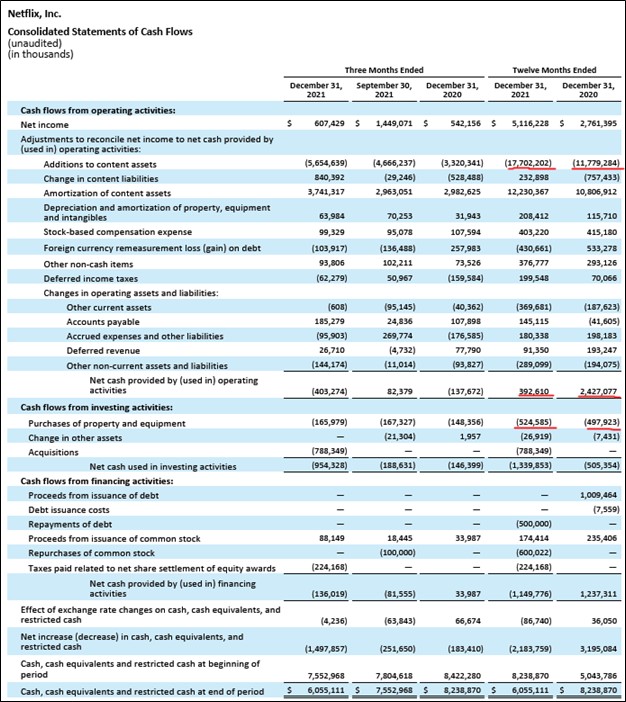

Netflix’s net operating cash flows were negative in both 2018 and 2019 due primarily to its large ‘additions to content assets’ line-item in its cash flow from operating activities section. In 2020, that figure declined by 15% versus 2019 levels after years of steady growth due to the pandemic which temporarily supported Netflix’s net operating cash flow performance. Netflix generated $2.5 billion in net operating cash flow while spending $0.5 billion on capital expenditures in 2020, allowing for $2.0 billion in free cash flow. We’ve highlighted the relevant line items in the upcoming graphic down below.

Image Shown: Netflix does not generate consistent cash flows due primarily to its enormous original content investments. Image Source: Netflix – Shareholder letter covering the fourth quarter of 2021 with additions from the author

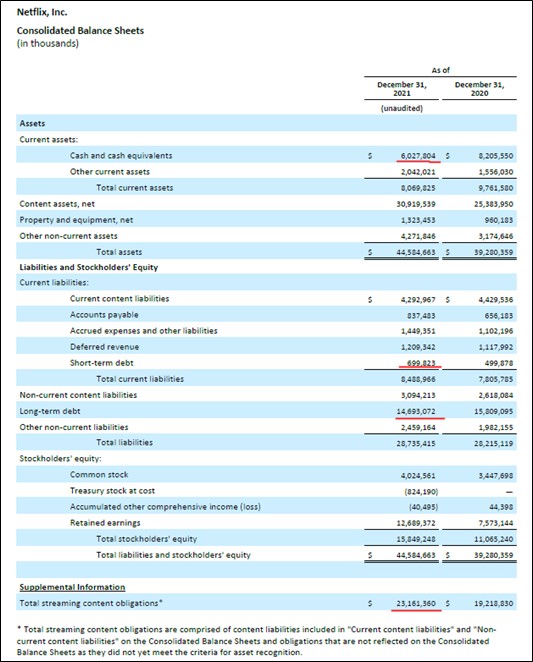

Large original content investments weigh negatively on Netflix’s ability to generate consistent cash flows, and the company has historically tapped debt markets to fund its growth ambitions. Netflix exited December 2021 with a net debt load of $9.4 billion (inclusive of short-term debt), though its $6.0 billion in cash and cash equivalents position at the end of this period should provide it with ample liquidity to meet its near term funding needs. We caution that Netflix also notes it had sizable ‘total streaming content obligations’ on the books at the end of 2021 as one can see in the upcoming graphic down below (see the asterisked line item at the bottom of the financial statements).

Image Shown: Netflix had a large net debt load at the end of 2021 along with sizable total streaming content obligations. Image Source: Netflix – Shareholder letter covering the fourth quarter of 2021 with additions from the author

Industry Getting Crowded

Investing enormous sums towards growing their original content portfolio is how video streaming services are differentiating their offerings in an increasingly-crowded market. The following few paragraphs provide a snapshot of some of the activity the video streaming industry has witnessed in recent years.

AT&T Inc’s (T) WarnerMedia unit launched the streaming service HBO Max in May 2020, adding another well-funded competitor to the arena. Now, WarnerMedia is merging with Discovery Inc (DISCA), which launched its own streaming service Discovery+ in January 2021, and the deal will create a behemoth in the media and entertainment space. That comes as Amazon Inc (AMZN) continues to pour billions towards original content investments for its Prime service.

Furthermore, Comcast’s NBCUniversal unit launched its Peacock streaming service in July 2020, fuboTV Inc (FUBO) launched its namesake sports-oriented streaming service back in January 2015 and later completed its IPO in October 2020, and ViacomCBS Inc (VIAC) launched its streaming service Paramount+ in March 2021 to capitalize on the merger of Viacom and CBS in December 2019. Disney launched Disney+ in November 2019, which quickly turned into a massive hit in households across the world as we have covered often in the past (link to our November 2021 article covering Disney here).

As of early October 2021, Disney+ had over 118 million paid subscribers, EPSN+ had over 17 million paid subscribers, and Hulu had almost 44 million paid subscribers. Since late-December 2019, Disney+, ESPN+, and Hulu have collectively added almost 116 million net paid memberships to their subscriber bases. The goal laid out during Disney’s big investor day event in December 2020 was to grow the collective paid subscriber base of these three services to 300-350 million by fiscal 2024 versus 179 million at the end of fiscal 2021. Launching its internationally-focused Star service in February 2021 offers room for further upside going forward. For reference, Disney’s fiscal year ends in early October.

Some of these new video streaming services represent rebranding efforts and initiatives to consolidate multiple existing streaming services into one. AT&T shut down HBO GO and rebranded HBO Now when launching HBO MAX, while CBS All Access was rebranded as Paramount+. To capitalize on their respective rebranding efforts, AT&T and ViacomCBS launched a ton of original content on HBO Max and Paramount+ to drum up excitement in their new streaming services.

Taking a step back, we would like to highlight the tremendous subscriber growth Netflix has put up over the past two years. At the end of 2019, Netflix had about 167 million paid memberships across the global. By the end of 2021, that figure had grown to roughly 222 million as demand for video streaming services surged in the wake of the pandemic. Maintaining the growth rates Netflix has put up over the past two years, especially in 2020 when Netflix added almost 37 million net paid memberships to its business, was always going to be a stretch and unlikely to occur in 2022.

Considering Netflix continued to grow its paid subscriber base throughout 2021 after putting up banner performance in 2020 and in light of rising competitive headwinds, the company’s fourth quarter performance and its near term outlook are more impressive than immediately meets the eye. However, investors were pricing in loftier expectations.

Netflix did provide some commentary on its gaming aspirations during its latest earnings update. Management noted that the firm would first focus on mobile gaming opportunities and was also “open to licensing, accessing large game IP that people will recognize” to support its efforts developing games. The company has already released some mobile video games that are accessible for subscribers to Netflix. We are intrigued by Netflix’s mobile gaming strategy as a way to further differentiate its services from its many competitors, though these are still early days. The company needs to prove that it can create popular games that generate some buzz around its service.

Fair Value Estimate Considerations

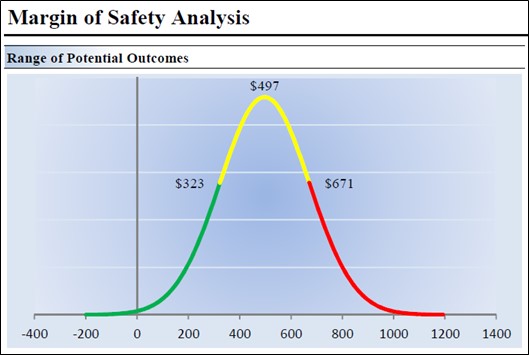

Our fair value estimate for Netflix sits at $497 per share under our “base” case scenario, though should the firm underperform our “base” case forecasts, the low end of its fair value estimate range sits at $323 per share under our “bear” case scenario. As of this writing, NFLX is trading at ~$398 per share and appear to be fairly valued (with modestly positive risk-reward potential) given they are trading in the lower bound of the fair value estimate range.

Image Shown: Shares of Netflix appear to be fairly valued as of this writing as they are trading in the lower bound of their fair value estimate range.

Concluding Thoughts

Netflix has a highly scalable business model with a ton of operating leverage. The company’s global growth runway is enormous and its pricing power in its key North American markets is impressive. However, rising competitive headwinds and new market entrants have made the video streaming space quite crowded. We are intrigued by Netflix’s push into mobile games but are concerned with its inconsistent cash flows and sizable financial liabilities and other obligations.

Our favorite play in the video streaming space is Disney and we include shares of DIS as an idea in the Best Ideas Newsletter portfolio. While Disney’s slate of video streaming services are also contending with rising competitive headwinds, similar to Netflix, we see Disney’s expansive and high-quality IP po