Image Source: Honeywell – J.P. Morgan Industrials Conference Presentation

By Brian Nelson, CFA

On Monday, March 15, Honeywell International (HON) reminded us why it is one of our favorite industrial ideas. The firm presented at J.P. Morgan’s Industrial Conference, and we liked what management had to say. Honeywell was a recent addition to the Dividend Growth Newsletter portfolio, and here’s our thoughts on the industrials giant November 27 and the view we still hold today:

With GE’s (GE) fall from grace years ago, Honeywell has taken the reigns as one of Valuentum’s top industrial ideas. Though Honeywell’s valuation is not attractive as we’d like it to be at the moment, we recently raised our fair value significantly to north of $200 per share. With respect to this idea, we’d like to add some more industrials exposure to the Dividend Growth Newsletter portfolio to take advantage of what could become a very strong global economic rebound in 2021 (source).

Industrials equities, as measured by the Industrials Select Sector SPDR ETF (XLI) have outpaced the broader market year-to-date in 2021. Energy equities, as measured by the Energy Select Sector SPDR ETF (XLE), have also soared thus far this year, along with financials, as measured by the Financials Select Sector SPDR ETF (XLF). Our move to rotate into the areas of energy and financials in early January in the Best Ideas Newsletter portfolio has served members well.

That said, we could have been more aggressive knowing that we would see some strength in the most beaten-down areas of financials and industrial/energy, but it’s very hard to pass up (or trade in and out of) some of the strongest entities on the marketplace that we already include in the newsletter portfolios, namely many of the net-cash-rich, competitively advantaged and free-cash-flow powerhouses found within big cap tech. For example, we think companies such as Apple (AAPL) and Microsoft (MSFT) will be the dividend growth companies of this decade, and we can’t take our eye off the bigger picture.

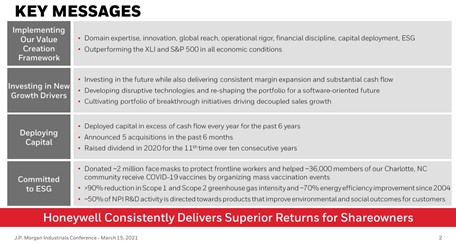

In the longer run, we still think big cap tech is the place to be in light of secular growth trends and higher-return business (asset light) models, but there are opportunities within other sectors as well. Specifically, for dividend growth investors that are seeking long-term exposure to the industrials sector, it’s hard to find a better idea than Honeywell, in our view. The company’s ‘Key Messages’ at the J.P Morgan Conference are provided in the image below, including its emphasis on capital deployment toward dividends and growth in them (Honeywell has raised the payout eleven times in the past ten years).

Image Source: Honeywell – J.P. Morgan Industrials Conference Presentation

Looking ahead to full-year 2021, Honeywell’s management reaffirmed its previously issued guidance, calling for sales to be in the range of $33.4-$34.4 billion with organic growth of 1%-4%. Segment margins for the year are targeted at 20.7%-21.1%, up 30-70 basis points on a year-over-year basis, and earnings per share is anticipated to be between $7.60-$8.00, up 7%-13% on an adjusted basis.

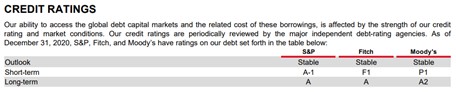

When it reported fourth-quarter results January 29, the company released a target range of $5.1-$5.5 billion in free cash flow for 2021. To put that range in perspective, it paid out just $2.6 billion in cash dividends during 2020, revealing very nice coverage of the dividend with expected free cash flow. The company’s Dividend Cushion ratio of 2.3 is robust, and while we’d prefer the company to have a net cash position, long-term investment-grade credit ratings of A, A, and A2 at S&P, Fitch, and Moody’s, respectively, speak to tremendous financial health.

Image Source: Honeywell’s 2020 10-K.

Concluding Thoughts

2021 will be a solid year for Honeywell, but we expect 2022 and 2023 to be even brighter, as some of the company’s revenue initiatives bear fruit in a much healthier industrial marketplace buoyed by greater infrastructure spending. The cost cuts put in place during COVID-19 should help with margin improvement as economic conditions pick up, putting the firm in a position to surprise to the upside. We expect continued dividend growth. Honeywell yields 1.7% at the time of this writing.

Downloads

Honeywell’s 16-page Stock Report (pdf) >>

Honeywell’s Dividend Report (pdf) >>

—–

Tickerized for HON, GE, XLI, XLE, RCKY, CW, TATT

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Brian Nelson owns shares in SPY, SCHG, QQQ, and IWM. Brian Nelson’s household owns shares in HON. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.