Goldman Sachs posted a rough first quarter of 2020, results released April 15, just like its large bank peers. Regarding its on-balance sheet debt and equity investments, we remain very skeptical both about the marks on private equity and amortized cost debt, as well as the appropriateness of holding this size of assets on a leveraged bank balance sheet. In our view, it simply exposes the shareholders to too much risk, and we think these investments should be sold down to reduce risk.

By Matthew Warren

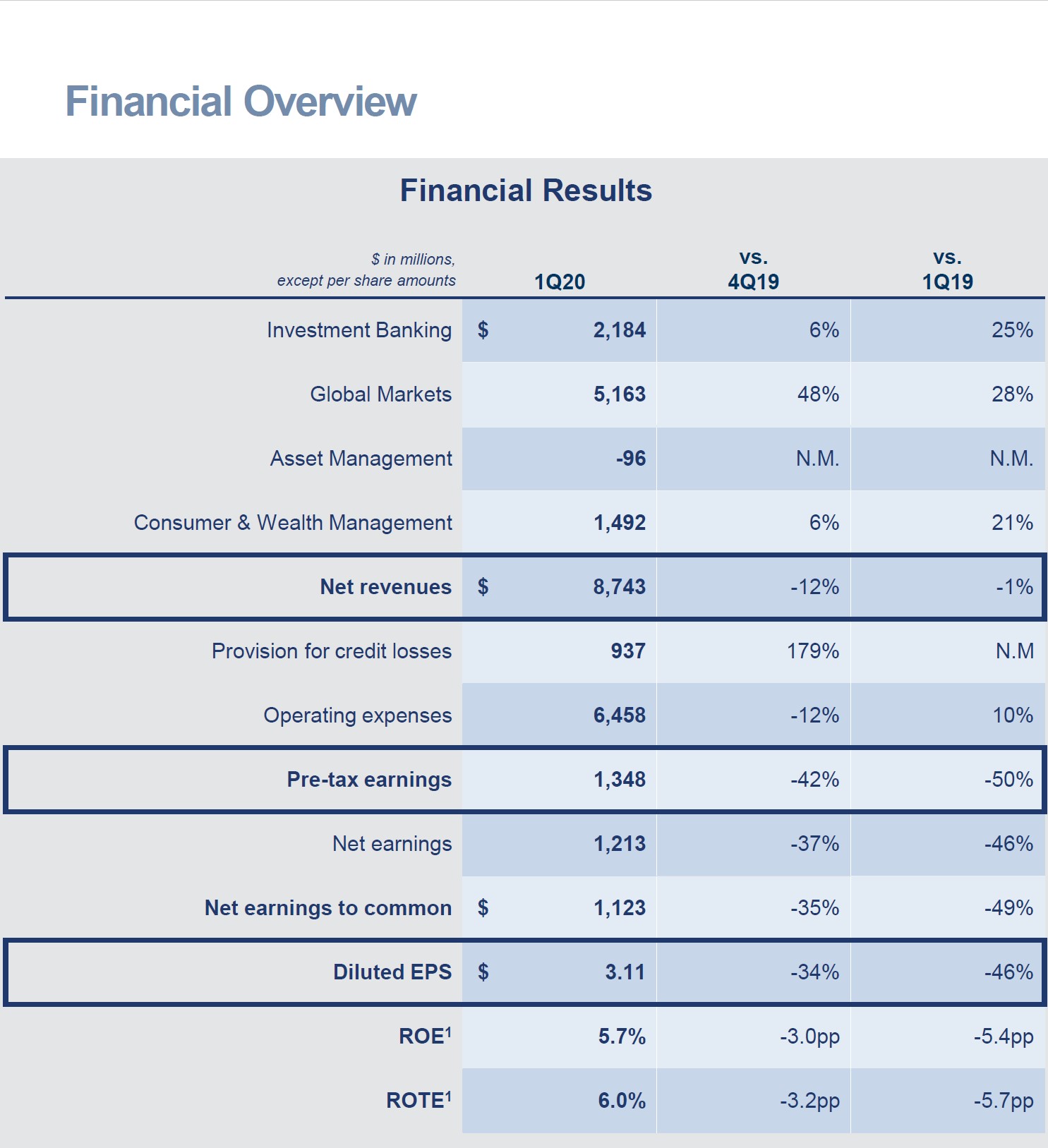

Goldman Sachs (GS) posted a rough first quarter of 2020, results released April 15, just like its large bank peers. While the firm exceeded the consensus estimate on the top line with revenue of $8.74 billion, or $820 million more than expected, the bank’s $3.11 of GAAP EPS missed consensus by $0.18. Annualized return on equity dropped to 6% in the quarter, suggesting the bank is likely to trade at a discount to its $214.69 tangible book value until the market gains confidence it will come out the other side posting stronger results.

As one can see in the graphic down below, the bank posted strong revenue growth in three of its four segments, but markdowns on on-balance sheet debt and equity positions meant that the Asset Management segment’s revenue was actually negative in the quarter, to the tune of $96 million. The provision for credit losses also jumped substantially to $937 million. Expenses grew 10% while revenue went 1% backward, meaning efficiency ratios also moved in reverse, and net earnings were crushed, falling 46%.

Image Source: Goldman Sachs 1Q2020 Earnings Presentation

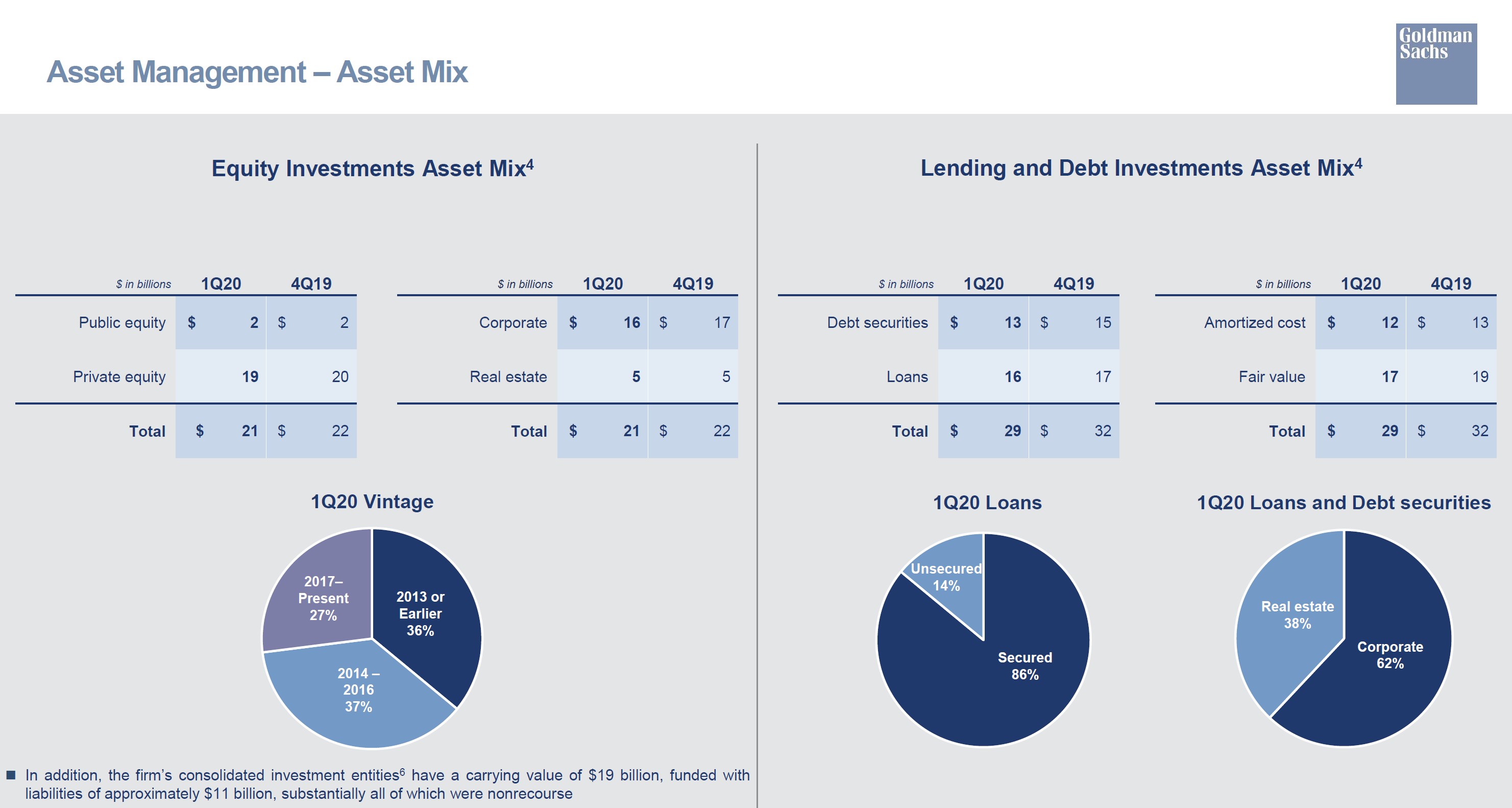

Regarding the on-balance sheet debt and equity investments, we remain very skeptical both about the marks on private equity and amortized cost debt, as well as the appropriateness of holding this size of assets on a leveraged bank balance sheet. In our view, it simply exposes the shareholders to too much risk, and we think these investments should be sold down to reduce risk. One can see the exposures detailed in the below graphic.

Image Source: Goldman Sachs 1Q2020 Earnings Presentation

These $50 billion of on-balance sheet investments can impact Goldman Sachs’ $74.6 billion of Common Equity Tier I capital, meaning large swings in valuations could easily affect the strength of the balance sheet. It was concerns like these that really drove fear among stakeholders during the Global Financial Crisis. While there are not large piles of collateralized debt obligations (CDOs) this time around, we still don’t like the exposure. We are maintaining our recently reduced $140 fair value estimate at this time.

—

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.

Matthew Warren does not own any of the securities mentioned. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.