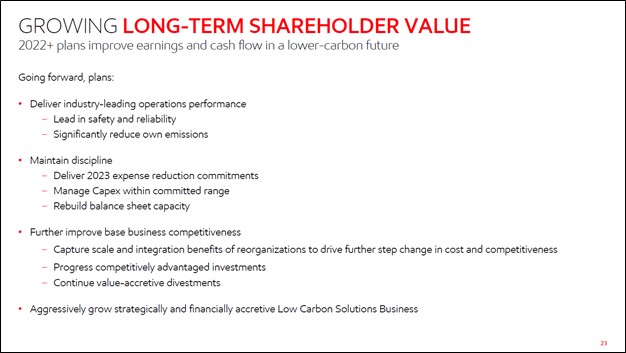

Image Shown: An overview of ExxonMobil Corporation’s strategy to generate shareholder value going forward. Image Source: ExxonMobil Corporation – Second Quarter of 2021 Earnings IR Presentation

By Callum Turcan

We added shares of ExxonMobil Corporation (XOM) as an idea to both the Best Ideas Newsletter and Dividend Growth Newsletter portfolios back on June 27 (link here) to gain greater exposure to the ongoing recovery in the global energy complex. On a day-to-day, month-to-month basis, raw energy resources pricing (crude oil, natural gas, and natural gas liquids) will bounce around (commodity prices are inherently volatile). However, what we have been interested in the most is the sharp recovery seen in raw energy resources pricing since the start of 2021. That includes liquified natural gas (‘LNG’) prices as well, which generally speaking are tied to Brent, the premier international oil pricing benchmark, though the emergence of the US as an LNG exporting powerhouse is slowly changing that.

Background

Crude oil pricing is on the rise in part due to efforts by the OPEC+ oil cartel to limit supplies (an agreement that will phase out through September 2022 under the current structure) and in part due to the resumption of “normal” daily activities around the world, including the return of the daily commute and a rebound in domestic air travel. The easing of lockdown restrictions to contain the coronavirus (‘COVID-19’) pandemic combined with households feeling at ease to resume “normal” daily activities, aided by widespread COVID-19 vaccine distribution efforts, supports the outlook for refined petroleum product (gasoline, diesel, kerosene) demand and ultimately crude oil demand. Due to the integrated nature of ExxonMobil’s business model, the firm is incredibly well-positioned to benefit from this upside.

The company’s vast upstream operations (involved with extracting raw energy resources from the ground) enable ExxonMobil to directly capitalize on higher raw energy resources pricing. ExxonMobil’s downstream operations (namely refineries and petrochemical plants) benefit primarily from higher utilization rates in the current environment as demand recovers, enabling its downstream assets to run at more “normalized” levels (utilization rates at these assets plummeted during the worst of the COVID-19 pandemic). Subdued utilization rates ruin the economics of refineries and petrochemical plants, though elevated utilization rates provide a powerful tailwind to the economics of these facilities.

Please note that ExxonMobil’s downstream operations are contending with higher input costs (i.e., rising raw materials pricing), which are counterbalanced by pricing increases at the pump and elsewhere (such as pricing increases for its plastics and other petrochemical products) and the ability for many of its facilities to source cost-advantaged feedstocks. ExxonMobil’s enormous downstream presence along the US Gulf Coast region represents a prime example of assets that can source cost-advantaged feedstocks that still have ample access to overseas markets via immense export capabilities.

Earnings Update

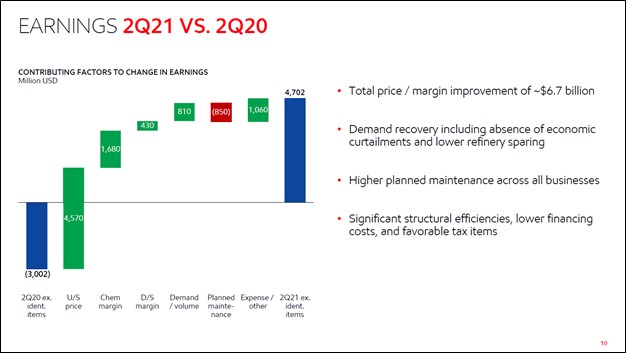

On July 30, ExxonMobil reported second-quarter 2021 earnings that beat both consensus top- and bottom-line estimates. Please note we will have more to say about the firm once it publishes its 10-Q SEC filing covering the second quarter of 2021, as ExxonMobil provided only a snapshot of its financial performance last quarter. The company’s ‘total revenues and other income’ more than doubled year-over-year in the second quarter of 2021 and were up 15% sequentially. The firm’s GAAP net income flipped from a $1.1 billion loss in the second quarter of 2020 to a $4.7 billion gain in the second quarter of 2021 (up 72% sequentially).

ExxonMobil’s ‘Upstream,’ ‘Chemical,’ and ‘Downstream’ divisions all benefited from significant margin expansion and/or pricing increases last quarter on a year-over-year basisas one can see in the upcoming graphic down below. Rising demand and volume increases (on a net basis across all of ExxonMobil’s divisions) along with cost structure improvements further supported ExxonMobil’s financial performance on a year-over-year basis last quarter. The firm’s upstream production base slipped modestly lower year-over-year last quarter, though this was offset by sharp increases in its crude throughput volumes at its refineries (which was accompanied by a sharp increase in its refined petroleum product sales by volume) and rising petrochemical product sales by volume.

Image Shown: An overview of the dynamics that saw ExxonMobil’s earnings performance stage an impressive recovery last quarter versus year-ago levels. Image Source: ExxonMobil – Second Quarter of 2021 Earnings IR Presentation

Beyond margin expansion, ExxonMobil has been aggressively focused on improving its cost structure. During ExxonMobil’s second quarter 2021 earnings call, management noted that “in addition to reducing structural costs by $3 billion in 2020, the company has captured over $1 billion in further structural savings in the first half of 2021” which will go a long way in improving ExxonMobil’s free cash flow generating abilities over the long haul. Furthermore, ExxonMobil’s management team noted that “the company remains on pace to achieve through 2023 total structural cost reductions of $6 billion relative to 2019” which is great news.

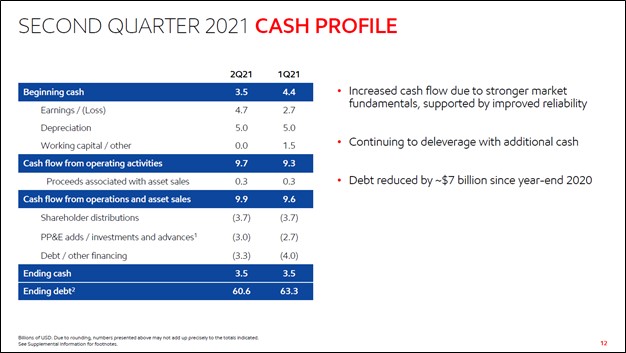

The upcoming graphic down below provides a snapshot of ExxonMobil’s cash flow performance during the first and second quarters of this year. Again, we will have more to say when ExxonMobil publishes its 10-Q SEC filing covering last quarter, though we like the company’s recent update. ExxonMobil generated ample free cash flows during the first half of 2021 (~$13.3 billion as defined as net operating cash flows less ‘PP&E adds/investments and advances’) which fully covered its shareholder distributions (totaled ~$7.4 billion in the first half of 2021) and then some during this period. Management noted that ExxonMobil allocated a large chunk of its “excess” free cash flows (free cash flows less dividend obligations) to debt reduction activities, which we really appreciate.

Image Shown: A snapshot of ExxonMobil’s cash flow performance during the first and second quarters of 2021. Image Source: ExxonMobil – Second Quarter of 2021 Earnings IR Presentation

Upstream Update

ExxonMobil has several promising upstream opportunities that can help the firm reverse a roughly decade-long (I, II) slide in its upstream production base. Its upstream production fell on both a year-over-year and sequential basis in the second quarter of 2021 for a variety of reasons (maintenance, natural declines at mature fields, etc.), though looking ahead, things are significantly brighter.

The company’s two core growth engines on the upstream front are represented by its assets in the prolific Permian Basin in West Texas and the southeastern corner of New Mexico, and the Stabroek exploration block (which has existing production facilities with many more to come) off the coast of Guyana along the northern coast of South America. Here is what management had to say regarding ExxonMobil’s upstream operations in Guyana during the firm’s second quarter earnings call (lightly edited, emphasis added):

“In Guyana[‘s] Stabroek block, we’ve added three new discoveries since the first quarter, including the Whiptail discovery announced this week. The Uaru-2 well encountered 220 feet of high quality oil bearing reservoirs. The Longtail-3 well encountered 230 feet of net pay, and both of these results included newly identified intervals below the zones originally discovered.

Resource quantification is ongoing. The Whiptail-1 well encountered 246 feet of net pay and drilling is ongoing at the Whiptail-2 well, which has encountered 167 feet of net pay, both in high quality oil bearing sandstone reservoirs.

This additional resource will add to the 9 billion oil-equivalent barrels we discussed at Investor Day [held in March 2021], further increasing our confidence in the resource size and quality in the area east of Liza and supporting our view of an ultimate block-wide footprint of seven to 10 [upstream] developments. The projects in progress remain on schedule, with the expected arrival of the Liza Phase 2 Unity FPSO in Guyanese waters early in the fourth quarter.

Payara, the third major development on the block is on track for a 2024 start-up, with topsides construction ongoing. And pending government approval, we’re targeting a final investment decision on Yellowtail, our fourth major development later this year, with start-up planned for 2025.” — Jack Williams, Senior Vice President of ExxonMobil

As we noted in our July 2021 article ExxonMobil’s Immense Upside in Guyana (link here), various planned and pending upstream developments off the coast of Guyana could have the ability to produce north of 1 million barrels of oil equivalent per day combined on a gross basis at their peak by the late 2020s. ExxonMobil owns 45% of this venture (specifically the Stabroek block), and this asset represents one of the best ways the energy giant can revive its upstream production trajectory going forward.

Image Shown: An overview of ExxonMobil’s recent updates and longer term strategy in Guyana. Image Source: ExxonMobil – Second Quarter of 2021 IR Earnings Presentation

Pivoting here, ExxonMobil and its partners approved a final investment decision (‘FID’) regarding developing the Bacalhau field in offshore Brazil in the second quarter of this year. ExxonMobil owns 40% of the venture and Norway’s Equinor ASA (EQNR) acts as the operator of the endeavor and owns 40% of the project. The other partners include Petrogal Brasil, a subsidiary of Portugal’s Galp Energia ADR (GLPEY), and an entity run by Brazil’s government known as Pré-sal Petróleo SA. By 2024, the Bacalhau field is expected to achieve first-oil and at its peak, the production facilities will have the capacity to produce 220,000 barrels of crude oil per day on a gross basis.

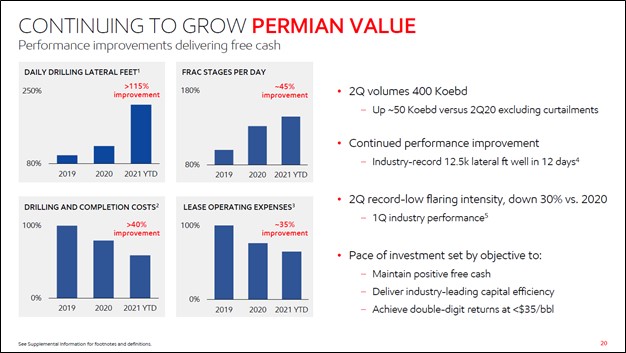

ExxonMobil’s upstream Permian Basin operations continue to progress nicely. Development and operating costs, on a relative basis, are shifting lower aided by efficiency gains. When excluding the impact of curtailments in response to the worst of the COVID-19 pandemic, and the related plummet in production levels last year, ExxonMobil’s Permian Basin operation grew its output by ~50,000 barrels of oil equivalent per day on a year-over-year basis last quarter. As of the second quarter of this year, ExxonMobil’s Permian Basin division pumped out ~400,000 barrels of oil equivalent per day with room for additional upside.

Image Shown: An overview of ExxonMobil’s progress in the Permian Basin, particularly as it concerns its upstream operations in the region. Image Source: ExxonMobil – Second Quarter of 2021 IR Earnings Presentation

Here is what ExxonMobil’s management team had to say regarding ExxonMobil’s upstream Permian Basin operations during the firm’s second quarter earnings call (lightly edited, emphasis added):

“We’re… benefiting from ongoing attractive upstream investments as well, especially in the Permian as development performance continues to improve, resulting in rapidly growing value. We produced [400,000] oil-equivalent barrels a day this quarter, which was up approximately 50,000 oil-equivalent barrels a day versus the second quarter of last year, excluding the impact of the economic curtailments. We expect to grow production a further 40,000 oil-equivalent barrels per day in the third quarter…

…[T]he [advantageous] short cycle development profile of the Permian gives us flexibility within the portfolio. The parameters setting our pace of development have not changed. First, delivering positive free cash flow across a broad range of price scenarios; second, demonstrating we are achieving industry leading capital efficiency; and third, ensuring double-digit returns at $35 a barrel or less.” — Senior Vice President of ExxonMobil

We appreciate ExxonMobil’s momentum on the upstream front across its positions in Guyana, Brazil, and the Permian Basin.

Midstream, Downstream, and Petrochemicals Update

As it concerns ExxonMobil’s downstream and petrochemical operations, the company continues to make sizable investments on these fronts and towards midstream infrastructure (such as pipelines) that support these operations. Please note that ExxonMobil took a leading role on the massive Wink-to-Webster crude oil pipeline development, which aims to transport 1+ million barrels of oil per day from origin points in the heart of the Permian Basin in West Texas (including at Midland, Texas, and Wink, Texas) which will run across the state to the US Gulf Coast region (carrying crude to major downstream hubs in Beaumont, Texas, and Texas City, Texas, and other locations by linking together with different pipeline networks).

This asset is largely operational, with ExxonMobil’s management team noting during the firm’s latest earnings call that the pipeline would begin handling third-party volumes by the fourth quarter of 2021. Please note there are a lot of partners participating in this project including ExxonMobil, Plains All American Pipeline LP (PAA), MPLX LP (MPLX), Delek US Holdings Inc (DK), privately-held Lotus Midstream, and Rattler Midstream LP (RTLR) which are all partners of the Wink to Webster Pipeline LLC joint-venture. Additionally, this joint-venture’s pipeline will link together with a pipeline network operated by Enterprise Products Partners L.P. (EPD) in the region. As an aside, we continue to like Enterprise Products as an idea in the High Yield Dividend Newsletter portfolio (more on that here).

Beyond this midstream development, ExxonMobil has numerous downstream and petrochemical projects in the works as one can see in the upcoming graphic down below. In our view, ExxonMobil’s growth outlook is quite promising. The company is currently upgrading its massive refining complex in Beaumont, Texas, to handle the light sweet crude oil