Image Shown: Shares of Meta Platforms Inc (blue line) and PayPal Holdings Inc (orange line) have staged a nice comeback during the past month, as of the start of April 2022.

By Callum Turcan

Rising interest rates and the impact that has had on the market’s discount rate implictly used within the enterprise cash flow pricing process has pressured the value of equities with long free-cash-flow growth tails–stocks that are expected to grow at a meaningful premium over global economic growth over the coming decades. The rapid increase in the 10-year Treasury rate, no doubt, has had a profound impact on the equity values of long-duration cash-flow companies such as those held in the ultra-speculative ARK Innovation ETF (ARKK), for example.

However, established big cap tech firms and many fintech entities shouldn’t necessarily be as impacted by rising interest rates as those of many currently money-losing speculative innovation names that won’t generate meaningful levels of free cash flow for 5 to 10 years, maybe longer. For example, shares of companies such as Apple Inc. (AAPL) or Microsoft Corp. (MSFT) should only have but a muted impact from rising rates; these companies have huge net cash positions and are already generating strong free cash flow. It can even be argued that higher inflation/rates will afford Apple and Microsoft pricing power to raise product and software prices.

While we might expect the ARK Innovation ETF to be down nearly 40% year-to-date and more than half during the past 52 weeks, we don’t think it makes a lot of sense for some of the strongest, large cap growth names to be off ~12%, on average, year-to-date. We think the market, in many instances and especially within the area of technology, is throwing the baby out with the bathwater. Shares of Meta Platforms Inc (FB), formerly Facebook, and PayPal Holdings Inc (PYPL) are two such names that the market has been beating down too much, in our view. Though some weakness in Meta Platform’s and PayPal’s shares can be expected in the current market environment, year-to-date declines of 30%+ and 40%+, respectively, are a bit much.

That said, during the past few months, we have reduced our fair value estimates for both Meta Platforms and PayPal for good reasons. For starters, Meta Platforms is investing heavily in the metaverse, a digital universe, and is scaling up its data center capacity to support its efforts on this front (which is driving its capital expenditure and operating cost expectations up sharply in the medium-term). Meta Platforms is not expected to make a meaningful amount or any money on these investments for some time.

PayPal is facing headwinds from hefty customer acquisition costs to grow its active user base amid rising competitive threats. We also think that we may have been too aggressive within our valuation model when we built in too much earnings leverage during the next five years at PayPal. Said another way, the fintech company’s mid-cycle operating margin is not what we once though it was–as PayPal will find it difficult to meaningfully expand its margins in the current environment.

However, putting it all together, these pressures and others have all been reflected in our current fair value estimates (and fair value estimate ranges) for Meta Platforms, which sits at $367 per share, and PayPal, which sits at $152 per share. Both companies are included as ideas in the Best Ideas Newsletter portfolio, and we are beginning to see signs of a rebound underway. For long-term investors, we think Meta Platforms is a no-brainer at current prices, though we may be a bit more cautious on PayPal, which is now more of a “show-me” story, given recent hiccups.

All this having been said, let’s dig in to why we still like Meta Platforms and PayPal.

Meta Platforms

We continue to be enormous fans of Meta Platforms as its cash-based sources of intrinsic value are rock-solid and supported by its nice net cash position on hand, which stood at $48.0 billion at the end of December 2021 with no debt on the books (not including $6.8 billion in non-current equity investments at the end of this period). Meta Platforms generated $39.1 billion in free cash flow in 2021 and repurchased $44.5 billion of its Class A common stock.

Going forward, we expect Meta Platforms will repurchase “gobs” of its Class A common stock after its recent share price decline, made possible by its strong financial position. The firm announced a $50.0 billion increase in its share repurchase authority when reporting its third quarter of 2021 earnings update in October 2021. We are very supportive of Meta Platforms buying back its stock given that shares of FB are trading at an enormous discount to their intrinsic value based on what we believe to be reasonable assumptions, indicating such a move would generate substantial shareholder value.

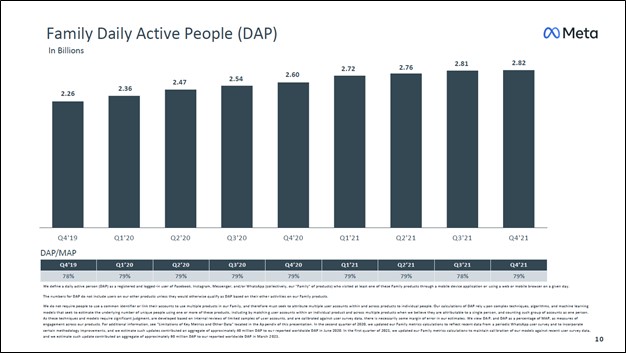

Though Meta Platforms’ various social media operations (Facebook, Instagram, WhatsApp) are facing competition from relative newcomers like TikTok, the firm’s underlying offerings remain in high demand. For instance, across all of its social media operations, Meta Platforms saw its family daily active people (‘DAP’) come in north of 2.8 billion during the fourth quarter of 2021, up on both a year-over-year and sequential basis. This is the kind of strength that enabled Meta Platforms to grow its GAAP revenues by 37% year-over-year in 2021, almost entirely due to strong sales of its digital advertising products and services. Meta Platforms’ core business remains sound, and calls to the contrary are overblown, in our view.

Image Shown: Meta Platforms’ social media operations remain incredibly popular and are regularly used by over 2.8 billion people each day. Image Source: Meta Platforms – Fourth Quarter of 2021 IR Earnings Presentation

When looking at Meta Platforms’ family monthly active users (‘MAP’), that figure came in just below 3.6 billion during the final quarter of 2021, up on both a sequential and year-over-year basis. Considering Meta Platforms caters to the lion’s share of the entire population connected to the Internet, estimated at just below 4.7 billion as of January 2021 according to Statista, it of course will be difficult to grow its active user base by a robust clip on an annual basis, though simply maintaining its current active user base is a big win for the firm. As additional households across the globe get connected to affordable internet for the first time, Meta Platforms’ growth runway should continue to grow.

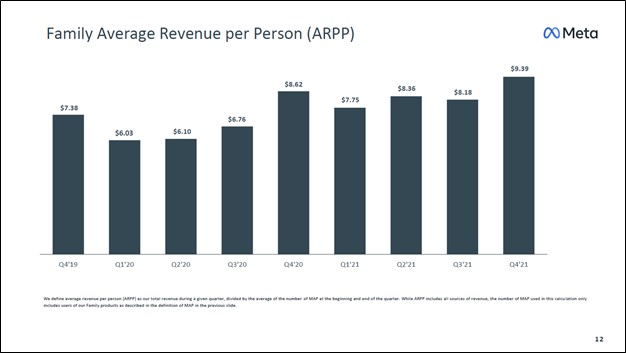

Another way Meta Platforms can improve its business is by capitalizing on growth in the global middle class and related increases in discretionary income. The firm’s family average revenue per person (‘ARPP’), based on its MAP, has been steadily climbing higher due in part to Meta Platforms’ pricing power and in part to its active user base in some economies becoming better off economically, which makes it easier to justify pricing increases for digital advertising services. Its ARPP stood at $9.39 in the final quarter of 2021, up from $8.62 in the same period in 2020.

Image Shown: Meta Platforms is steadily improving its ability to monetize its active user base with room for upside. Image Source: Meta Platforms – Fourth Quarter of 2021 IR Earnings Presentation

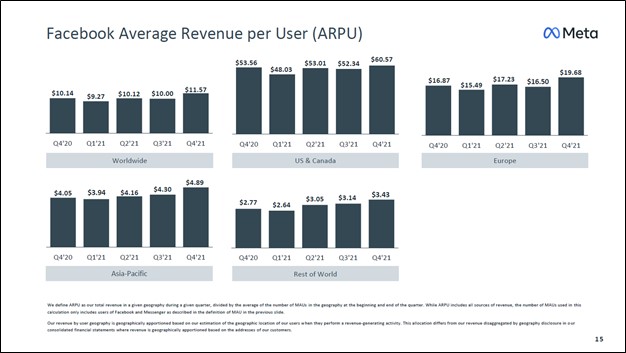

Meta Platforms has ample room to further improve its monetization efforts. The firm breaks down the average revenue per user (‘ARPU’) at Facebook, which as of the final quarter of last year ranges from $60.57 in the US and Canada to $4.89 in the Asia-Pacific region and stood at $11.57 on a worldwide basis. Over time, as the digital advertising markets outside of the US and Canada continue to develop in tandem with the broader economy in those regions, Facebook’s ARPU should improve on a worldwide basis which in turn should significantly support Meta Platforms’ company-wide financial performance.

Image Shown: The difference in ARPU at Meta Platforms’ Facebook operation across geographical markets is stark. Image Source: Meta Platforms – Fourth Quarter of 2021 IR Earnings Presentation

Meta Platforms is also seeking upside in the realm of e-commerce, payment processing, and through its ambitious metaverse strategy. Please note that this upside is entirely incremental to our fair value estimate. It’s not included in our valuation model!

Based on Meta Platforms’ core social media and digital advertising business, which has been doing just fine of late (despite headwinds from Apple’s iOS changes), we view shares of FB as incredibly undervalued. For that reason, we include shares of FB as a top-weighted idea in the Best Ideas Newsletter portfolio, and we may even consider increasing the weighting in the event of broader market weakness.

We continue to be excited about Meta Platforms’ future free cash flow generating potential. Our thesis is supported by its strong performance in the recent past and secular tailwinds supporting the digital advertising industry, along with the “moaty” characteristics of its business model (namely the network effect), which underpins our expectations that Meta Platforms will continue to grow at a robust pace over the coming years and decades.

Meta Platforms is getting ready to report its first quarter earnings for 2022 on April 27. During its fourth quarter of 2021 earnings update, management guided that the firm would spend ~$29-$34 billion on its capital expenditures this year, a steep climb from the $18.6 billion it spent in 2021, though Meta Platforms’ net operating cash flows should be able to fully cover those cash layouts with relative ease. The company’s operating expenses are also set to shift higher. For the first quarter of 2022, the company guided that its revenues would grow by 3%-11% on a year-over-year basis, though we think this is conservative. We are intrigued by what updates management might offer up during Meta Platforms’ upcoming earnings report.

On a final note, Meta Platforms is still working on changing its ticker from FB to META, which is expected to be completed during the first half of 2022.

PayPal

While we are less optimistic on PayPal as compared to Meta Platforms given the competitive threats the fintech firm is facing and how that may impact its future growth opportunities and pricing power, the company’s cash-based sources of intrinsic value are also rock-solid.

As with Meta Platforms, PayPal has a nice net cash position. At the end of December 2021, PayPal had $1.5 billion in net cash on hand with no short-term debt on the books, and that figure does not include its $6.8 billion long-term investments which includes $3.6 billion in cash-like holdings (time deposits and available-for-sale debt securities) along with $3.2 billion in ‘strategic investments’ according to the firm. PayPal’s pristine balance sheet provides it with options as it seeks to revive its fortunes, including share repurchases.

PayPal generated $5.4 billion in free cash flow in 2021, aided by its relatively modest capital expenditure requirements to maintain a certain level of revenues (a product of its asset-light business model). The firm spent $3.4 billion buying back its stock last year, and we expect that PayPal will take advantage of the downturn in its share price to repurchase “gobs” of its stock this year. We are very supportive of this strategy.

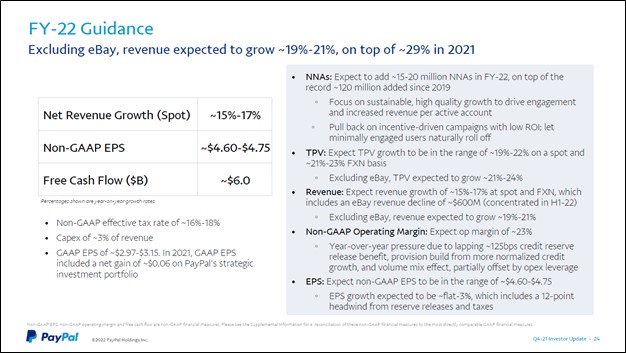

During PayPal’s fourth quarter of 2021 earnings report, the company issued guidance for 2022 that was a mixed bag. On the one hand, PayPal expects to generate ~$6.0 billion in free cash flow and ~15%-17% revenue growth on a spot basis (as it concerns foreign currency) in 2022. On the other hand, PayPal expects its non-GAAP operating margin will face pressures and its non-GAAP EPS is expected to either come in flat or grow by up to 3% this year. PayPal sees its total payments volume (‘TPV’) growing at 19%-22% on a spot basis and 21%-23% on a foreign currency neutral basis this year.

Image Shown: PayPal’s guidance for 2022 is a mixed bag. Image Source: PayPal – Fourth Quarter of 2021 IR Earnings Presentation

PayPal’s expects it will continue adding net new active accounts (‘NNAs’) to its business at a decent clip this year with the aim to add 15-20 million, though management has recently admitted that the goal is no longer to grow PayPal’s active user base at any cost. The firm announced it had dropped its goal to achieve 750 million active accounts in a few years’ time during PayPal’s fourth quarter of 2021 earnings call.

Trouble growing its NNAs in an economical manner has been a key hurdle for PayPal as it seeks to invest in growth opportunities while maintaining its margins. New market entrants from fintech firms have significantly increased PayPal’s competitive threats. Its operating margins on both a GAAP and non-GAAP basis have trended lower in recent years, and placing limits on its customer acquisition spending activities is part of how PayPal intends to reverse that trajectory. PayPal had 426 million active accounts during the fourth quarter of 2021, though its year-over-year growth rate on this front has been steadily slowing after a banner 2020 performance (its year-over-year NNA growth rate stood at 13% in the final quarter of 2021 versus 24% in the final quarter of 2020).

Image Shown: PayPal is slowing down its efforts to grow its NNA at any cost by limiting its customer acquisition spending levels in certain situations. Image Source: PayPal – Fourth Quarter of 2021 IR Earnings Presentation

PayPal runs an attractive business that is catering to various secular tailwinds such as the proliferation of e-commerce, the shift from cash to card and digital payments, and has exposure to global economic growth. The firm is working on monetizing its popular peer-to-peer payment transfer app Venmo and secured a partnership with Amazon Inc (AMZN) that was announced in November 2021. This deal involves giving Venmo users the option to pay with the app when ordering from Amazon.

Here is what PayPal had to say regarding monetizing Venmo during its fourth quarter of 2021 earnings call:

“Venmo had a solid finish to the year and closed out 2021, with more than $0.25 billion of revenue in the fourth quarter, up 80% year-over-year. We are still at the beginning of our monetization journey, with Amazon implementing the option to pay with Venmo later this year. And Venmo is turning an important corner and in Q4 helped to drive the sequential increase in our overall take rate.” — Dan Schulman, President and CEO of PayPal

There is a lot to like about PayPal. It has a strong balance sheet, great free cash flow generating abilities, and its longer term growth outlook is quite promising, aided by efforts to monetize Venmo. We include shares of PYPL as an idea in the Best Ideas Newsletter portfolio at a moderate weighting, and we see room for PayPal to recover some of its lost ground after shares boomed from 2020 through most of 2021, before pulling back sharply in recent months.

Concluding Thoughts

We view the ideas included in the newsletter portfolios as well-positioned to navigate inflationary pressures due to their pricing power and supply chain hurdles due to their scale and focus on innovation. Fears over rising interest rates has seen the name of companies with long growth tails sell off, though we continue to be bullish on large cap tech stocks over the long run as their cash-based sources of intrinsic value are simply stunning. Meta Platforms and PayPal remain two of our favorite ideas for long-term investors.

—–

Technology Giants Industry – FB, AAPL, GOOG, AMZN, MSFT, CSCO, V, MA, PYPL, INTC, ORCL, QCOM, TWTR, IBM, ADBE, NVDA, CRM, AMD, AVGO, BABA, BKNG, BIDU, TSM, FFIV, TXN, EBAY, ADP, PAYX, MU, KFY, MAN, KLAC, LRCX, AMAT, ADI, SIMO

Tickerized for FB, PYPL, PINS, AFRM, SQ, SNAP, TWTR, SOCL, TSLA, RBLX, DWAC, DWACW, NYT, BIDU, BABA, CRTO, KIND, ZNGA

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges,