Image: Ferrari’s fundamental momentum has been strong of late. Image Source: Ferrari N.V. 2022 Globe Newswire

By Brian Nelson, CFA

The auto industry perhaps has changed more than any other industry the past five years. First, it was Ford (F) that said it wouldn’t make passenger cars anymore, except for its iconic Mustang. Then, the European Union said that it would eventually end the internal combustion engine (ICE) by 2035. Then, Tesla (TSLA) reached over $1,200 per share and over a $1 trillion market capitalization. Can you imagine a world where Ford is not making sedans, the once modern-marvel of the internal combustion engine is dying, and where one car maker is worth as much as the next nine car makers combined?

Certainly, a lot has changed in the auto industry during the past decade, and we haven’t dabbled much in the auto sector as it relates to idea generation due in part to the industry’s fast-changing backdrop. That doesn’t mean that we’re not fans of the auto space and its promising long-term opportunities, particularly with electric vehicles (EVs). It just means that we think there are better stories elsewhere, as in ideas in the simulated newsletter portfolios. However, if we had to pick two of our favorite auto names to consider, they would be Tesla and Ferrari (RACE), even as we note General Motors (GM) and Ford (F) both trade at mid-single-digit earnings multiples.

That said, investors don’t necessarily have to take on the risks of automakers, especially as the group deals with chip shortages, supply chain issues, and margin pressures from higher input costs. The cyclicality of many of the operators and the reality that operating leverage cuts both ways (and is quite painful during difficult economic times) are risks that perhaps won’t ever go away. That said, exposure to the auto space via Tesla or Ferrari could work nicely in a broadly diversified equity portfolio should risk-seeking investors be so inclined. These two names remain on our radar.

Tesla’s Cash-Based Fundamentals Support Its Stock

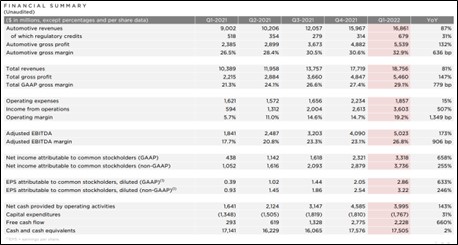

Though it remains a cult stock, Tesla fundamentals are on the up and up. The company has become a free-cash-flow generating powerhouse, and its balance sheet is rock-solid. For starters, Tesla has generated free cash flow north of at least $1 billion in each of the past three sequential quarters, and it hauled in $2.775 billion and $2.228 billion in the fourth quarter of 2021 and the first quarter of 2022, respectively (see image that immediately follows). Tesla ended the first quarter of 2021 with $18 billion in cash and short-term marketable securities, while total debt, excluding vehicle and energy product financing stood at less than $100 million at the end of the quarter.

Image: Tesla has been growing like a weed as free cash flow trends have markedly improved. Image Source: Q1 2022 Update.

We love companies that are tied to secular growth trends, have strong free cash flow generating capabilities, and sport net cash rich balance sheets. Tesla’s outlook is quite strong, too, with ample room for strong revenue growth and meaningful margin expansion over the long haul. That said, CEO Elon Musk and Tesla have a lot on their plate as the company scales its business and expands its manufacturing capabilities into new geographical markets, all while rolling out new products, such as its Cybertruck (an EV pickup truck). As with its industry rivals, Tesla is not immune to broader industry challenges, however, which it summed up in its latest quarterly report:

Challenges around supply chain have remained persistent, and our team has been navigating through them for over a year. In addition to chip shortages, recent COVID-19 outbreaks have been weighing on our supply chain and factory operations. Furthermore, prices of some raw materials have increased multiple-fold in recent months. The inflationary impact on our cost structure has contributed to adjustments in our product pricing, despite a continued focus on reducing our manufacturing costs where possible.

According to Reuters, Tesla has reportedly delayed production of the Cybertruck until 2023, but such growing pains should be expected, especially as the coronavirus (‘COVID-19’) pandemic threw a wrench into the development timetables of most companies. Tesla’s EVs remain in very high demand, and it is likely its customers will be able to wait until then for their futuristic looking Cybertruck. Even though Tesla’s market cap has fallen quite a bit from the $1 trillion price tag, the company still has proven the critics wrong, in our view, and it’s hard not to like fundamental trends at the controversial name.

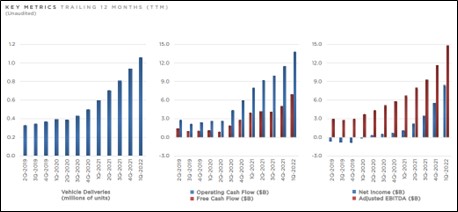

Image: Tesla key metrics have been moving in the right direction. Image Source: Q1 2022 Update.

General Motors to Launch More than 30 EVs Globally by 2025

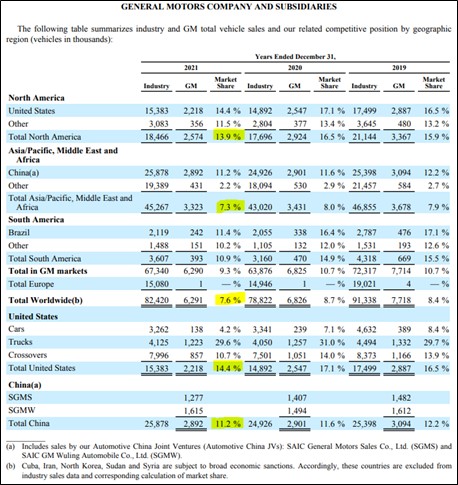

Image: General Motor’s has faced dwindling market share in the U.S. and China the past few years. Image Source: GM’s latest 10-K.

In April 2020, General Motors suspended its dividend and share buyback programs to conserve cash in the wake of the COVID-19 pandemic. Though the firm is contemplating reinstating its dividend, that may not occur for some time. During the past several years, General Motors had significantly improved its break-even point (before the pandemic hit), which helped drive margin improvements. General Motors is working very hard to stay relevant into today’s fast-changing auto market, too, particularly with EVs. Here’s more from its General Motors’ latest 10-K:

Our vision for the future is a world with zero crashes, zero emissions and zero congestion, which guides our growth-focused strategy to invest in electric vehicles (EVs) and autonomous vehicles (AVs), software-enabled services and subscriptions and new business opportunities, while strengthening our market position in profitable internal combustion engine (ICE) vehicles, such as trucks and sport utility vehicles (SUVs). We have committed to an all-electric future with a core focus on zero emission battery EVs as part of our long-term strategy to reduce petroleum consumption and greenhouse gas (GHG) emissions. As a result, we have committed to making total EV and AV investments of more than $35.0 billion from 2020 through 2025…

…We plan to launch more than 30 EVs globally by 2025. A key element in our EV strategy is Ultium, our all-new dedicated battery electric platform. Our first Ultium-based products launched with the GMC HUMMER EV and BrightDrop EV600 in 2021, to be followed by the Cadillac LYRIQ in 2022. This all-new platform is flexible and will be leveraged across multiple brands and vehicle sizes, styles and drive configurations, allowing for quick response to customer preferences and a shorter design and development lead time compared to our ICE vehicles…

Our end-to-end software platform Ultifi will provide our customers with software-defined features, apps and services over-the-air starting in 2023. Ultifi and the apps it enables will empower customers to update their ownership experiences continuously with desirable features such as vehicle performance, ADAS, safety and security features, climate and comfort options, personal themes and EV ownership experience elements, including battery and charging details…

…Cruise is driving leadership in the development and commercialization of AV technology. We believe that building all-electric vehicles with autonomous capabilities integrated from the beginning, rather than through retrofits, is the most efficient way to unlock the tremendous potential societal benefits of self-driving cars. The Cruise Origin, a purpose-built, all-electric, self-driving vehicle that is being co-developed by GM, Cruise and Honda Motor Company, Ltd. (Honda), will be built on General Motors’ all-new modular architecture, powered by the Ultium platform, at Factory ZERO starting in early 2023, pending government approvals.

Though General Motors is facing sizable market share headwinds as global rivals take share against the storied auto maker, fundamentals still remain resilient. When the company reported its first-quarter 2022 results April 26, it called for “full-year 2022 net income in a range of $9.6 billion-$11.2 billion and reaffirmed its earnings guidance of EBIT-adjusted in a range of $13.0 billion-$15.0 billion.” GM also expects to double revenue, to the range of $275-$315 billion, by 2030, while expanding margins along the way as it reaps new higher-margin business and as it scales its EV operations.

Image: GM is expecting big things to happen by 2030. Image Source: Q1 2022 Results.

These are some lofty goals, and while GM is not immune to the industry’s supply chain issues and stiff cost headwinds, we’re not ruling the automaker out, by any stretch. The company ended the first quarter of 2022 with $32.9 billion in automotive liquidity and $16.9 billion in total automotive debt. Adjusted diluted earnings per share for 2022 is targeted at $6.25-$7.25, implying that shares of GM are trading at just 4.5x this year’s earnings at the high end of the range, though we note that the large automakers have always traded at a low multiple due to the operating leverage of their business model that cuts deep during challenging economic times.

Ford’s New Product Line-Up Holds Tremendous Promise

Image: We’re excited by Ford’s new product line-up including the F-150 Lightning, but we like a few other companies in the auto space more than Ford. Image Source: Ford’s Q1 2022 Earnings Slide Deck.

Ford has sizable industrial and financing businesses built around its Ford and Lincoln brands. After suspending its dividend in 2020, the company resumed its quarterly dividend in October 2021. Ford has big plans for its electric vehicle (EV) business. The auto giant forecasts it will spend ~$40-$45 billion towards its total capital expenditures from 2020- 2025, with ~$30 billion of that allocated to its EV operations. That strategy involves Ford building new EV and battery manufacturing facilities in Tennessee and Kentucky, with support from its strategic partner, SK Innovation. Ford’s all-electric F-150 Lighting pickup truck has drummed up a lot of excitement in its growth outlook.

Ford has a history of suspending its dividend as it halted payments during both the Great Financial Crisis and the COVID-19 pandemic. Most recently, Ford needs to retain ample liquidity on hand to meet the funding needs of its industrial and financing operations. Cutting its dividend has historically been one of the main ways Ford has conserved capital in the wake of exogenous shocks to its business. Ford’s electric vehicle (EV) growth ambitions will require enormous levels of capital investments for years to come, and its net debt load is another concern, but recent quarterly results, while weak, haven’t been that poor, and excitement around its new product line-up remains.

Image: Ford’s first-quarter results weren’t that great. Image Source: Ford’s Q1 2022 Earnings Slide Deck.

During Ford’s first-quarter 2022, revenue, adjusted EBIT, adjusted EBIT margin, adjusted free cash flow and adjusted earnings per share all fell in the quarter on a year-over-year basis due in part to supply chain constraints, unfavorable mix and inflationary increases in commodity prices. Though we’re huge fans of what the F-150 Lightning may bring to Ford’s bottom line, at the moment, we think there are better ideas in the auto space out there at the moment. Ford ended the first quarter with strong cash and liquidity, to the tune of $44.6 billion and cash-net-of-debt stood at $8.7 billion. Consensus earnings estimates put Ford’s latest share price at just 5.8x this year’s earnings, but as with GM, the cyclicality of its operations means results could face huge pressure during painful downswings.

Ferrari May Be a Hidden Investment Gem in the Auto Sector

Image: Ferrari’s fundamentals keep moving in the right direction. Image Source: Q1 2022 Press Release.

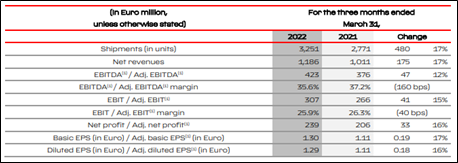

Though we like Tesla’s fundamental momentum, free cash flow generation, and net-cash-balance sheet relative to General Motors and Ford, we also think investors should be aware of the fundamental strength at Ferrari N.V. The company’s performance for the first quarter ended March 2022 was fantastic, with total shipments up 17.3%, net revenues up by the same pace, EBITDA up 12.5% versus the prior year, and industrial free cash flow generation that came in at Euro 299 million. We loved the quarterly performance, and here’s what management had to add in the press release:

In the start of the year we recorded excellent results, with a double-digit growth on the main financial indicators. The first quarter was characterized by a record level of revenues, EBITDA and industrial free cash flow, which almost doubled to approximately Euro 300 million thanks in particular to the collection of advances on the Daytona SP3. Margins in the quarter were in line with our guidance”, stated the CEO of Ferrari, Benedetto Vigna. “These results were sustained by a strong net order intake, which continued firmly over the first three months of the year: today the order book already covers well into 2023 and most of our models are sold out.

Ferrari’s strategic plan for 2022-2026 also looks solid. The luxury car maker expects 15 new launches, as it plans for the first full electric Ferrari to be unveiled by 2025. Ferrari also plans to migrate to roughly a 60% hybrid and full electric line-up by the end of 2026, and it still expects the internal combustion engine to be a part of its line-up for some time to come. Here are some other key bullet points from Ferrari’s Capital Markets Day:

– The plan privileges revenue over volume and entails strong mix/price contribution, reaching in 2026 an EBITDA of Euro 2.5-2.7 billion with an EBITDA margin of 38%-40%.

– Cumulated capital expenditures of Euro ~4.4 billion to fuel product development, of which ~75% focused on products and ~25% on infrastructures.

– Consistently generating strong cumulated industrial free cash flow of Euro 4.6-4.9 billion over the 2022-2026 plan period.

– Shareholders will be rewarded through a dividend pay-out increased from 30% to 35% of adjusted net income from 2022 onward and a share-repurchase program of Euro ~2 billion from now to 2026.

It’s hard not to like Ferrari’s iconic brand and how it continues to focus on preserving its status by not sacrificing price for volume. A brand new all-electric Ferrari by 2025 sounds exciting, and a shareholder-friendly management team that is committed to a dividend and buybacks as the firm throws off tremendous industrial free cash flow is certainly a plus. Shares of Ferrari have fallen more than 30% year-to-date, to ~$180 at the time of this writing, but we like the long-term picture at the company, and as with Tesla, Ferrari represents one of our favorite names for consideration in the auto space.

———-

Tickerized for LI, BYDDY, NIO, XPEV, GM, TM, HMC, RACE, AUDVF, STLA, NSANY, TSLA, RIVN, CVNA, FREY, ELMS, CENN, ARVL, SEV, ALLG, BLBD, WKHS, LIDR, NKLA, TTM, DDAIF, BMWYY, POAHY, POAHF, VWAGY, VLKAF, VLKPF, F, EVGO, LCID, RIDE, GOEV, FSR, MULN, LEA, MGA, VC, BWA, FFIE, GWLLF, WLMTF, GELYF, GNZUF, BCCMY, DNFGY, KMX, LAD, VRM, SFT, AN, GPI, SAH, ABG, MMTOF, AXL, APTV, LOTZ, CARS

Brian Nelson owns shares in SPY, SCHG, QQQ, DIA, VOT, BITO, and IWM. Valuentum owns SPY, SCHG, QQQ, VOO, and DIA. Brian Nelson’s household owns shares in HON, DIS, HAS, NKE. Some of the other securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.

Valuentum members have access to our 16-page stock reports, Valuentum Buying Index ratings, Dividend Cushion ratios, fair value estimates and ranges, dividend reports and more. Not a member? Subscribe today. The first 14 days are free.