Image: Page 49, June edition of American Library Association Booklist.

By Brian Nelson, CFA

—

Welcome new members!

Roughly 90% of active management is underperforming their benchmarks, after fees, over the trailing 15-year period ending 2018. It’s a sad story out there. Most active investors are performing backward-looking analysis, others are using short-cut multiple analysis to make decisions; still, others may be continuing down the path of thinking that may have gotten active management in trouble in the first place: theoretical quantitative finance.

The bedrock of finance, for example, the Capital Asset Pricing Model (CAPM) and its beta have been shown to explain little about stock market returns, yet it is still in finance textbooks and still on key financial exams. The remaining two factors in the widely-known three-factor pricing model aren’t performing at all how one might have expected. The traditional quant value factor has now been underperforming growth for a long time, and many say there’s really not a size factor.

Finance knows there are not really growth and value stocks, and there’s no reason to suggest that just because a company is small it will even survive, let alone thrive. The challenge for the past couple decades has been similar to the challenges that permeated the 1970s and 1980s with the efficient markets hypothesis. Many just accepted the markets as being proven efficient then, and new ideas that disagreed with this view or the CAPM weren’t being published in academic journals during that time. Finance failed itself because it shut out new thinking.

The seeds were planted years ago for the ongoing bloodbath of underperformance we are witnessing today. In the 1990s, finance fell in love with data. It set off a wave of “empirical” research that may have created unfounded interest in spurious correlations. Certain books sold millions of copies; the work was all over the academic journals. It seemed data mining was everywhere! Research that tortured data until it said something, anything, laid the foundation for backward-looking, ambiguous factor research that has been proliferating during the past decade or so.

Today, I’m not even sure the most talented in finance are even asking the right questions. For example, when was the last time you heard someone ask: What is the stock of this company worth? It’s just not happening out there. Most are looking at P/E ratios, and believe it or not, most are purposely looking backwards and ignoring the future. It’s almost hard to fathom. The current generation has a chance to set finance up for a great future, but not if we extend the existing thinking into artificial intelligence and machine learning.

The industry needs to lay the “right” foundation for finance. For too long, investors have been sold on “buying anything at any price.” You should read the story about how index funds bought Longfin (and it has since folded) and cost investors millions. At what point does finance say that index funds have to do due diligence on their underlying holdings? If active fund managers don’t perform due diligence on a holding and it “blows up,” it is negligence. Why the free pass for index funds? There’s something wrong when asset managers know more about ambiguously-derived factors than how a deferred tax asset is created or how free cash flow is calculated.

I hope that my book Value Trap: Theory of Universal Valuation marks a turning point in the financial research industry. To you and me, 1) looking forward, 2) understanding that stock values are based on future expectations, and 3) calculating intrinsic value is simply par for the course. If other investors are not doing this, it should be no surprise that they are failing miserably. 90% underperformance! I hope my book serves as a wake up call for readers to demand forward-looking analysis and research that calculates a best fair value estimate.

There is more at stake than what we think. Here’s what keeps me up at night: If regulators can pass new legislation called Regulation Best Interest, as they have, and still allow advisors to charge 1%-2% to hold index funds, certain “influences” may be seeping into the laws of country. I can’t be convinced that charging 1-2% to hold an index fund is in anyone’s best interest. Index funds are free. We must preserve choice for customers. Active management is being attacked from everywhere, and index providers and passive asset managers are all to happy to market aggressively against them.

In my book Value Trap, I have debunked the conclusion of Sharpe’s “Arithmetic of Active Management” and have shown that the corporate equity market consists of just 17% active/ETF management, not sufficient enough for “skill” to equal out, in my view. I’m now looking hard at the data that compares active funds to benchmarking, and I believe that there may be a degree of over-benchmarking in there, but this is going to take some more work. I have some serious questions about what’s going on out there, and I don’t like it at all!

On this holiday weekend, I wanted to thank you so very much for being there. I believe our boutique firm Valuentum is making a huge difference, and frankly, we couldn’t have done it without you. Value Trap will be honored at the prestigious Next Generation Indie Book Awards in Washington DC in the coming week, so I may be delayed in responding to your emails. The book is a Blue Ink Review Notable Book and a Readers’ Favorite 5 Stars. We are working hard for the investor. Every. Single. Day. You deserve the truth so you can make the best decision, and I hope that you will take time to read my book.

We have built an entire company on providing investors the best research and valuation work out there (have you had a chance to check out our mobile site?). Our newsletters are fantastic pieces of work, and ideas in the Exclusive publication continue to deliver in a big way. Many are pitching P/E ratios and ambiguous data, but we’re taking a deep dive on each company, and there’s a ton of work that goes behind our idea generation. New members, please have a read of the article that follows below for more information.

Enjoy, and thank you again!

Brian Nelson, CFA

President, Investment Research

Valuentum Securities, Inc.

|

|

Let’s talk about our hierarchy of idea generation in this note.

—

A version of this article was sent to members previously.

—

Hierarchy of Idea Generation

A) Ideas in the newsletter portfolios (Best Ideas Newsletter portfolio, Dividend Growth Newsletter portfolio, High Yield Dividend Newsletter portfolio) or the Exclusive publication

B) Ideas that are rated 9s and 10s on the Valuentum Buying Index as potential long ideas

C) Ideas that are undervalued on a discounted cash-flow (enterprise valuation) basis and relative valuation basis

D) Ideas then are ranked below 9 on the Valuentum Buying Index as potential long ideas

—

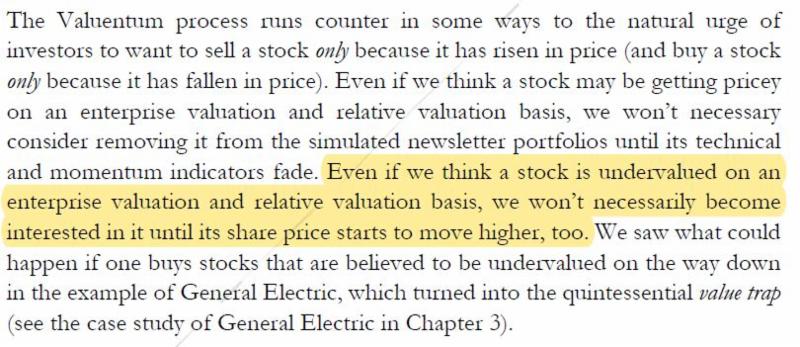

If you are only considering the estimated fair value of stocks, you could fall into value traps! Use momentum as another check and balance to assess what the market thinks is the true intrinsic value of the company. Using enterprise valuation (free cash flow to the firm) and momentum together could shield your portfolio from painful value traps. Simply put, there may be no logical basis for buying stocks immediately as they fall and on the way down. Here’s an excerpt from Value Trap: Theory of Universal Valuation.

Image: Excerpt from Value Trap: Theory of Universal Valuation, page 241

—

————————-

—

Image: Chipotle (CMG) was one of our best calls in 2019.

—

Image: Verint (VRNT) was a controversial idea in the Best Ideas Newsletter portfolio that worked out great for members this year.

—

Image: Visa (V) has been the top-weighted idea in the Best Ideas Newsletter for as long as we can remember. In December 2017, when we migrated to weighting ranges for ideas in the newsletter portfolio, the company’s “weight” was 8.6%. The image above shows its performance relative to the S&P 500 (SPY) since then. Source (pdf).

—

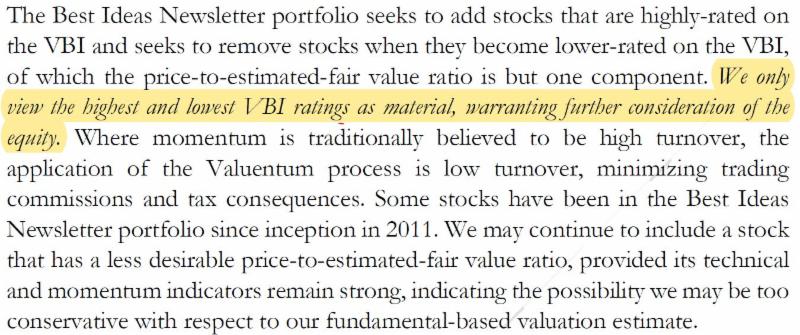

What Valuentum Buying Index (VBI) Ratings Are Material?

—  Image — Excerpt Value Trap: Theory of Universal Valuation, page 244. — By Brian Nelson, CFA —

I love it when I get questions because it shows the engagement of our members. I appreciate that very much. Though there are other considerations, of course, the Valuentum methodology is really quite simple: dividend growth considerations aside, we like undervalued ideas that are going up, and we generally won’t remove ideas that are overvalued until their technical/momentum indicators turn over. At times, however, I receive questions that worry me a bit that I may not be doing a good job communicating how we think about our service.

—

I’ve written consistently about how our favorite ideas are included in the Best Ideas Newsletter portfolio and Dividend Growth Newsletter portfolio, or for those seeking high yield, the High Yield Dividend Newsletter portfolio. The Exclusive publication is what I describe to be a “back-against-the-wall” publication where we “force” ourselves to highlight three new ideas each month: an income idea, a capital appreciation idea, and a short-idea consideration. The ideas in the three newsletter portfolios, per each strategy, or highlighted in the Exclusive publication are our favorites for consideration.

—

Though the ideas in the newsletter portfolios have done well, the Exclusive ideas have done extremely well, in my opinion. Through March 2019, for capital appreciation ideas highlighted in the Exclusive publication, the success rate is nearly 82% (81.8%). For short-idea considerations highlighted in the Exclusive publication, the success rate is nearly 79% (78.8%). Adjusted for currency, not one income idea has cut its payout either. That’s after 33 monthly editions!!! The Exclusive is purely incremental and highlights ideas that fall outside our vast coverage universe (and that may not fit as well into the existing newsletter portfolios). It is a great add-on publication if you may be interested.

—

For new members, Valuentum is a financial information publisher, so we don’t provide personal advice or personal recommendations. That’s not the area that we operate in. Only your personal financial advisor knows what is right for you. That means we can’t tell you to buy or sell anything or what you should do if you own a stock. Financial advisors build you a personal financial plan and select the stocks that may fit best to achieve your personal goals in the context of your personal risk tolerances. Be sure to ask your financial advisor if any move is right for you. We don’t operate in this area. We provide financial information and data. With that said, as we publish studies on the market, here is how we think about our Valuentum Buying Index ratings.

—

Image: The guidelines for how we think about the Valuentum Buying Index rating. This table is provided on our website and in each 16-page company report. Valuentum is not a broker, financial advisor or money manager. Valuentum is a financial information provider.

—

In this context and in light of what an 8 indicates on the Valuentum Buying Index (as shown in the table above), it would be puzzling for me to think that a company such as Tivity (TVTY), which had been rated 8 at the moment (it is now a 3), is the highest on one’s list of considerations. It may be a consideration, of course, but only after many, many others. For starters, we view only the 9s and 10s as material considerations on the long side, but even then, we still prefer ideas in the newsletter portfolios, first. Said another way, after scouring the ideas in our newsletter portfolios, then the 9s and 10s on the Valuentum Buying Index, then those that are undervalued on a discounted cash-flow basis (“DCF Undervalued”), one might then start to look at ideas that are lower on the Valuentum Buying Index.

—

Hierarchy of Idea Generation

A) Ideas in the newsletter portfolios (Best Ideas Newsletter portfolio, Dividend Growth Newsletter portfolio, High Yield Dividend Newsletter portfolio) or the Exclusive publication

B) Ideas that are rated 9s and 10s on the Valuentum Buying Index as potential long ideas

C) Ideas that are undervalued on a discounted cash-flow (enterprise valuation) basis and relative valuation basis

D) Ideas then are ranked below 9 on the Valuentum Buying Index as potential long ideas

—

So as we think about things that Valuentum didn’t quite get “right,” Tivity (once an 8 on the Valuentum Buying Index) is not such an example. It really wasn’t ever a consideration in the newsletter portfolios, nor was it a 9 or 10 on the Valuentum Buying Index. It was a stock that we had thought was undervalued, but valuation is one part of our process. The same is true for other stocks that appear undervalued on a discounted cash-flow basis that are not part of the newsletter portfolios or rated highly on the Valuentum Buying Index-

|